Content

Crypto regulation moved decisively from political positioning toward implementation this week.

The U.S. Securities and Exchange Commission placed three major digital-asset initiatives on its 2026 regulatory agenda. Congress converted the federal prohibition on a retail central bank digital currency into statutory law. Stablecoin regulators entered the final days before a key GENIUS Act implementation deadline. In Europe, MiCA’s transitional phase was over, leaving unauthorized platforms with instructions to stop onboarding clients and begin an orderly exit.

The common thread is execution. Legislators and regulators are no longer debating whether crypto should sit inside the financial rulebook. They are deciding which firms may operate, which assets may be distributed, how trading venues must register and what forms of digital money governments will permit.

| Jurisdiction | Development | Current Status | Market Significance |

|---|---|---|---|

| United States | SEC adds crypto assets, broker-dealer requirements and market-structure amendments to its 2026 agenda | Rulemaking Planned | Could reshape token issuance, exchange registration and broker capital treatment |

| United States | Federal Reserve prohibited from issuing a retail CBDC without congressional authorization | Enacted | Reinforces the U.S. preference for private, regulated digital dollars |

| United States | GENIUS Act implementation deadline approaches | Rules Still Being Finalized | Stablecoin issuers face near-term licensing, reserve and compliance decisions |

| United States | CLARITY Act negotiations continue in the Senate | Legislation Pending | Market-structure reform remains possible, but timing and final language are unresolved |

| European Union | MiCA transitional period has ended | Enforcement Phase | Unauthorized providers must stop expanding EU business and wind down operations |

| Bolivia | Government evaluating formal use of USDT as a payment method | Technical Review | Shows how currency pressure can push stablecoins into national payment policy |

The SEC Builds A Crypto Rulemaking Pipeline

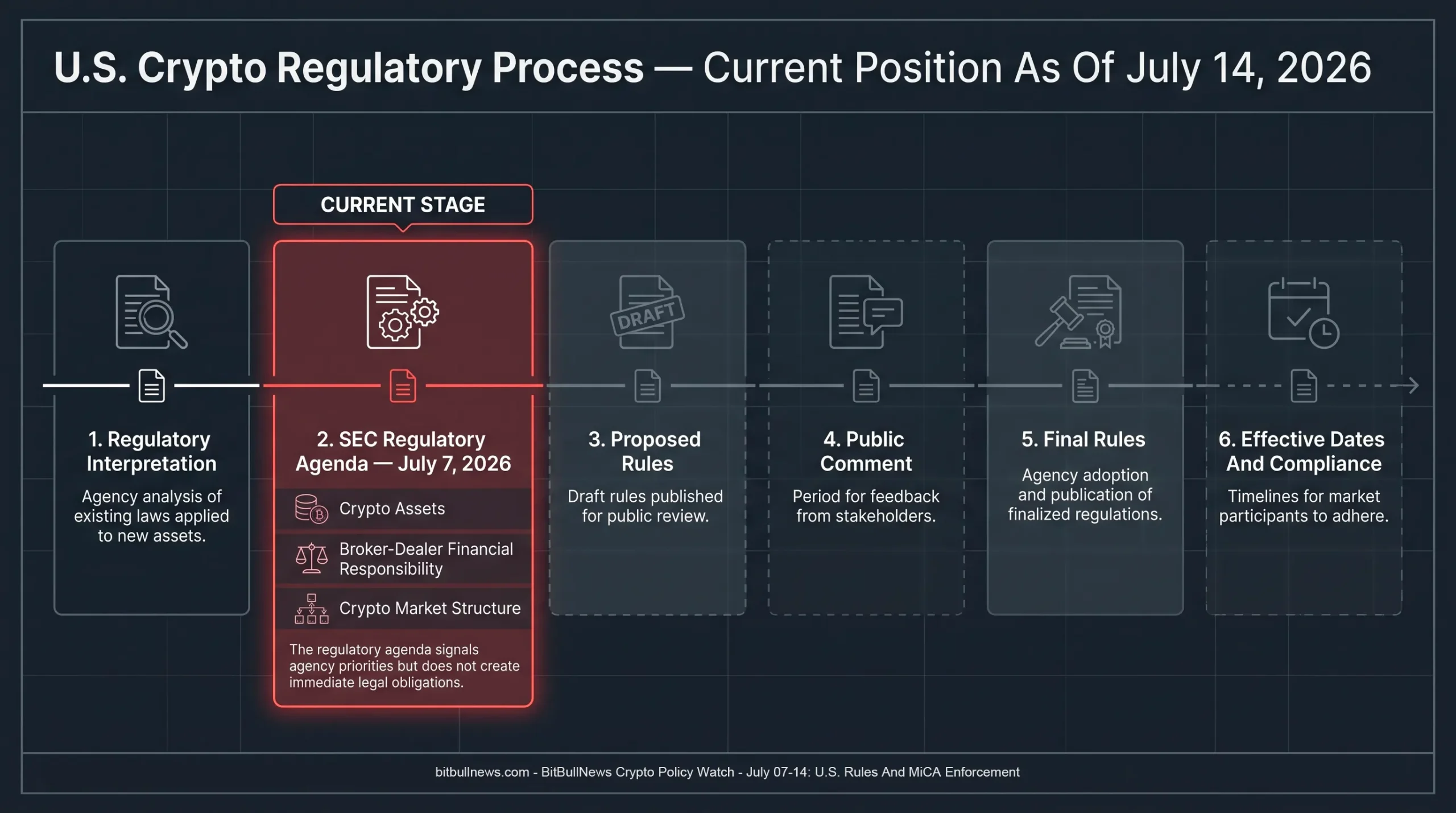

The SEC’s July 7 regulatory agenda identified three separate digital-asset workstreams: a broad crypto-assets proposal, amendments to broker-dealer financial-responsibility and reporting rules, and crypto market-structure amendments. The agency’s planning documents indicate that the crypto-assets initiative may include exemptions or safe harbors for token offers and sales, while the market-structure project may address trading through alternative trading systems and national securities exchanges.

That separation matters. The SEC is not treating crypto as one regulatory problem.

Token issuance raises disclosure, classification and registration questions. Broker-dealer custody creates capital, recordkeeping and customer-protection issues. Secondary trading requires rules covering venue registration, surveillance, execution and clearing. Addressing these areas through separate proposals gives the SEC more flexibility, but it also means the industry could face several overlapping compliance projects.

| SEC Initiative | Likely Regulatory Focus | Main Market Participants Affected |

|---|---|---|

| Crypto Assets | Token offers, sales, exemptions and possible safe harbors | Issuers, foundations, venture investors and token distributors |

| Broker-Dealer Crypto Rules | Capital, custody, recordkeeping and financial reporting | Broker-dealers, custodians and institutional trading firms |

| Crypto Market Structure | ATS and exchange treatment for digital-asset trading | Exchanges, ATS operators, market makers and infrastructure providers |

The agenda is not a final rule and does not create an immediate legal obligation. It is a planning document that signals the Commission’s priorities. Actual requirements would still need to pass through proposal, public comment, Commission approval and publication.

Even so, the direction is clear. Earlier SEC work focused heavily on interpreting how existing securities laws apply to activities such as staking, mining, airdrops and token wrapping. The new agenda points toward operational rules that could allow regulated crypto businesses to build around a defined registration framework rather than a collection of enforcement precedents.

The Market Read-Through: Regulatory clarity will depend less on whether the SEC calls an asset a security and more on whether it provides a workable route for issuing, custodying and trading that asset. A legal classification without functioning market infrastructure would solve only part of the problem.

Timeline Showing The U.S. Crypto Regulatory Process From SEC Interpretation To Proposed Rules, Public Comment, Final Rules And Effective Dates. Mark The July 7, 2026 Regulatory Agenda As The Current Stage.

The U.S. CBDC Ban Becomes Law

A federal prohibition on a retail central bank digital currency became law during the reporting period as part of H.R. 6644, the 21st Century ROAD to Housing Act. The measure became law without the president’s signature after the constitutional review period expired.

The legislation prevents the Federal Reserve Board and Federal Reserve banks from issuing or creating a CBDC, or a substantially similar digital asset, either directly or through a financial institution or other intermediary. It includes an exception for dollar-denominated currency that is open, permissionless, private and preserves the privacy characteristics of physical cash. The prohibition remains effective through December 31, 2030. The law also states that the Federal Reserve would still require explicit congressional authorization to issue a CBDC after that provision expires.

This is more consequential than the earlier executive-order prohibition. An executive order can be reversed by a subsequent administration. Statutory language requires Congress to act.

The policy signal is equally important. Washington is creating a federal framework for privately issued payment stablecoins while restricting the Federal Reserve from offering a competing retail digital currency. That leaves regulated banks, trust companies and approved non-bank issuers as the primary candidates for distributing blockchain-based dollars to the public.

The ban does not end every form of central-bank experimentation. Wholesale settlement systems, tokenized reserves and infrastructure used between regulated financial institutions remain separate policy questions. The law is aimed primarily at a broadly available Federal Reserve liability that could function as a public retail digital dollar.

The GENIUS Act Reaches Its Implementation Test

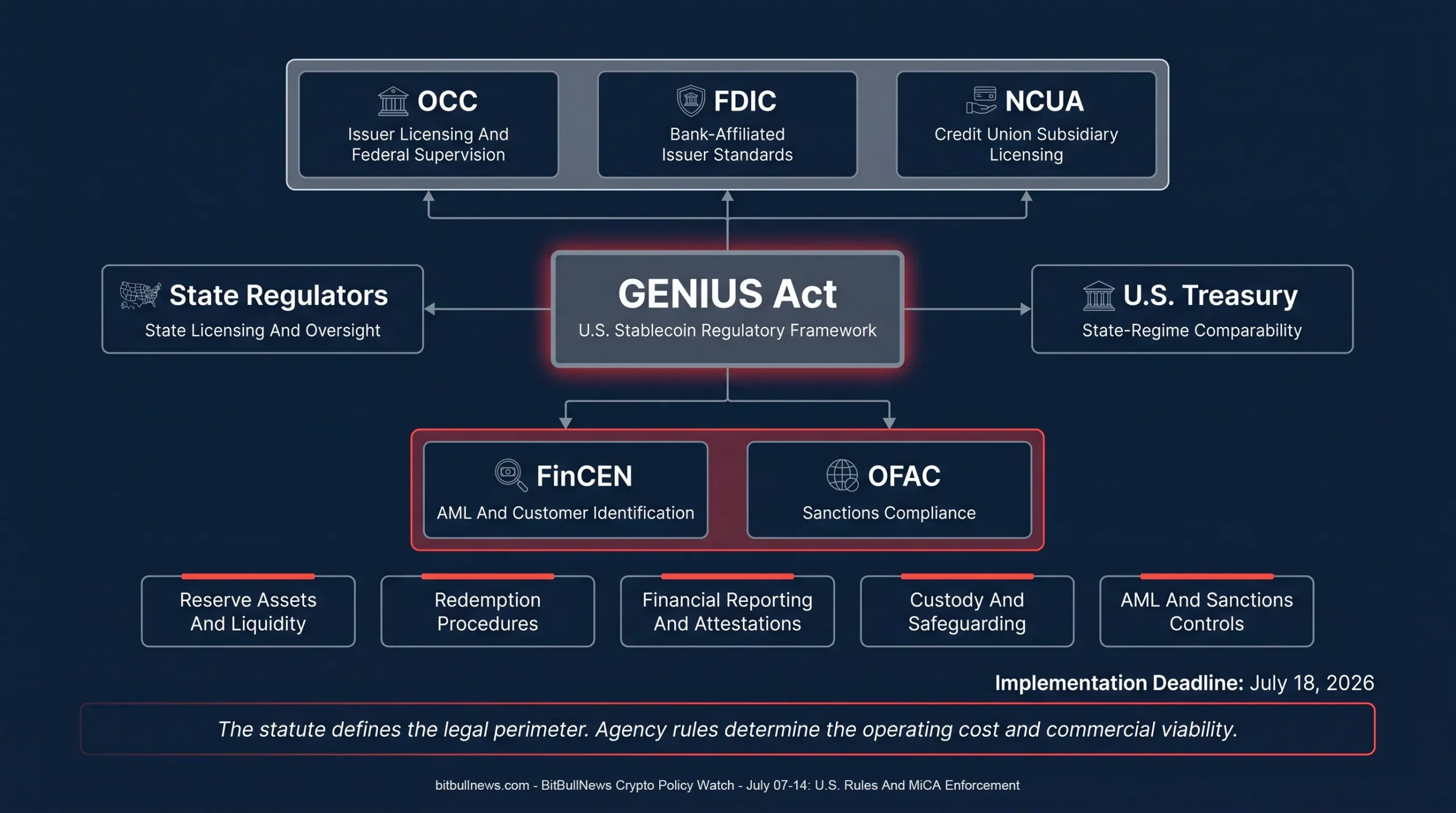

The GENIUS Act requires key federal regulators to issue implementing regulations by July 18, 2026. As of July 14, several major components were still represented by proposed rather than final rules.

The Office of the Comptroller of the Currency has proposed a licensing and supervisory framework for issuers under its jurisdiction. The Federal Deposit Insurance Corporation has proposed standards for permitted payment-stablecoin issuers connected to FDIC-supervised institutions. The National Credit Union Administration has published its own licensing proposal for credit-union subsidiaries. Treasury, FinCEN and OFAC are developing rules covering state-regime comparability, customer identification, anti-money-laundering controls and sanctions compliance.

| GENIUS Act Area | Responsible Authorities | Key Issue |

|---|---|---|

| Issuer Licensing | OCC, FDIC, NCUA And State Regulators | Which entities may issue payment stablecoins |

| Reserve Standards | Primary Federal Stablecoin Regulators | Eligible reserve assets, custody and liquidity |

| Financial Reporting | OCC, FDIC, NCUA And Treasury | Attestations, disclosures and supervisory filings |

| AML And Customer Identification | FinCEN | Customer due diligence and illicit-finance controls |

| Sanctions Compliance | OFAC And Treasury | Screening, freezing and transaction restrictions |

| State-Regime Comparability | Treasury | Whether state frameworks meet federal standards |

The immediate risk is sequencing.

An issuer may know the broad statutory requirements but still lack final forms, detailed supervisory procedures or settled interpretations across every relevant agency. That complicates product launches, bank partnerships and licensing decisions. It also raises the possibility that different categories of issuer will become operational at different speeds.

The deadline should therefore be treated as the beginning of the federal stablecoin regime, not the end of implementation. Firms will still need final agency rules, licensing manuals, examination procedures and guidance on how federal and state oversight interact.

For investors, the distinction between a statutory framework and an operating framework matters. The GENIUS Act created the legal perimeter. The agencies now determine how expensive, restrictive and commercially viable that perimeter will be.

U.S. Stablecoin Regulatory Map Showing The GENIUS Act At The Center, Connected To The OCC, FDIC, NCUA, Treasury, FinCEN, OFAC And State Regulators. Label Each Authority’s Main Responsibility.

The CLARITY Act Remains The Largest Unfinished U.S. File

The Senate Banking Committee advanced its version of the CLARITY Act in May by a 15–9 vote, but the bill had not reached final Senate passage by July 14. Fresh negotiations continued during the week, with updated language reportedly being prepared as lawmakers debated ethics restrictions, decentralized-finance provisions and stablecoin-related questions.

The legislation remains the central U.S. market-structure project because it would define the respective roles of the SEC and Commodity Futures Trading Commission, create registration paths for digital-asset intermediaries and establish rules for spot-market supervision.

Its political problem is no longer committee access. It is coalition durability.

A committee majority does not guarantee enough votes for the Senate floor, especially if the final text changes the treatment of DeFi developers, conflicts of interest or yield-bearing stablecoin products. Any Senate amendment would also have to be reconciled with the version previously approved by the House.

The absence of final legislation creates an unusual split in the U.S. regulatory timetable:

- Stablecoin regulation is entering implementation.

- The SEC is preparing agency-level market rules.

- The broader division of authority between the SEC and CFTC remains unsettled.

That raises the chance that agency rules arrive before Congress completes the statutory market-structure framework. Exchanges and broker-dealers should therefore prepare for both tracks rather than assume the CLARITY Act will replace the SEC’s rulemaking process.

MiCA Enters Its Enforcement Phase

The European Union’s MiCA transitional period ended on July 1. ESMA instructed crypto-asset service providers that had not obtained authorization to stop onboarding new EU clients, halt marketing and restrict their activities to the steps necessary to transfer assets, close positions or complete an orderly exit.

Unauthorized firms may continue custody only for the period strictly required to complete the wind-down. They must also maintain customer-due-diligence, transaction-monitoring, sanctions-screening and recordkeeping controls during the exit process. ESMA said national authorities could take coordinated action against significant unauthorized cross-border providers.

This changes MiCA from a licensing project into a distribution constraint.

Before July 1, a platform’s application status could be treated as an administrative issue. After July 1, authorization affects whether the platform can acquire customers, advertise services, hold assets and maintain commercial relationships in the EU.

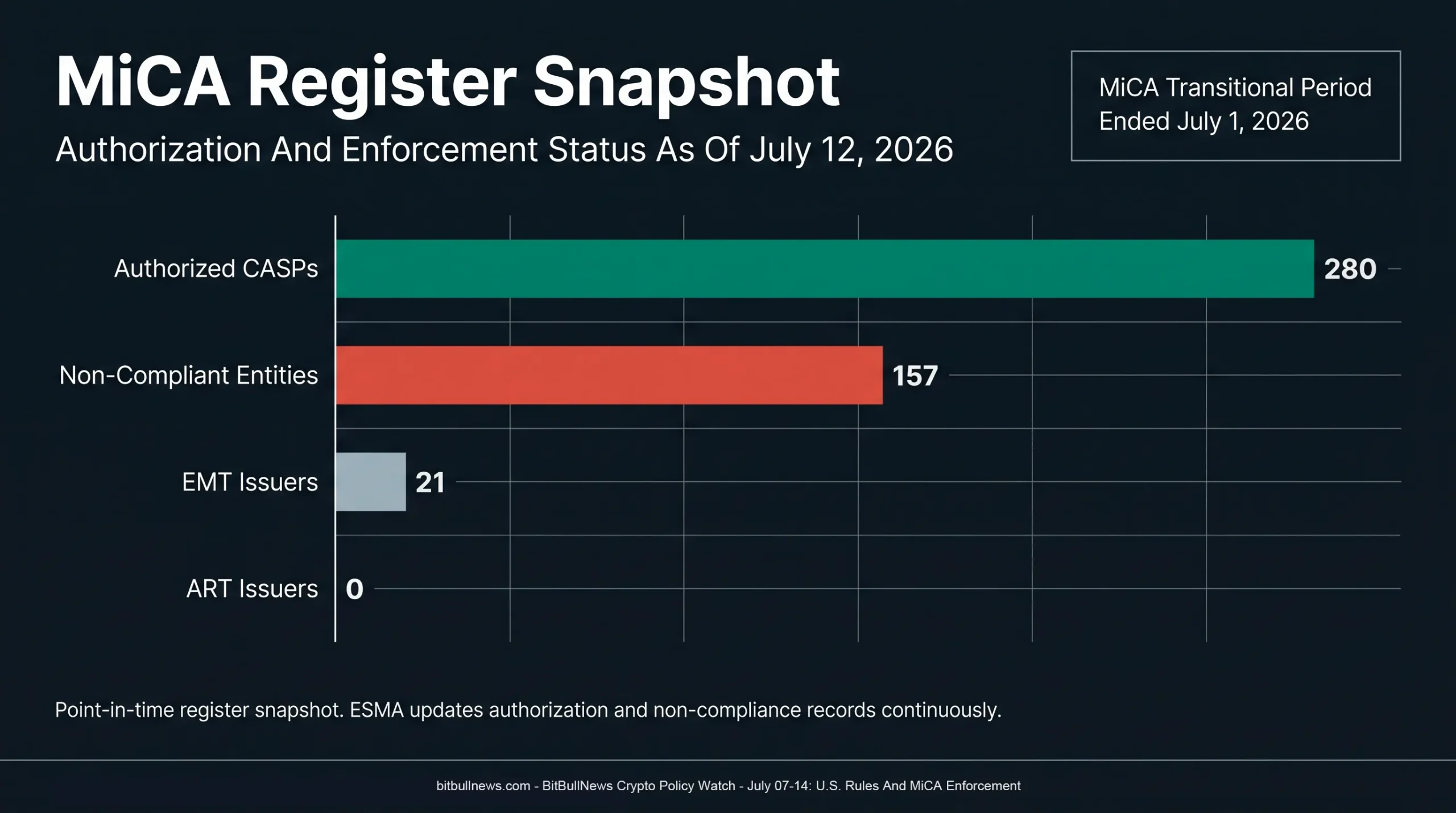

A July 12 snapshot compiled from ESMA’s downloadable register files showed the following market structure:

| MiCA Register Category | Recorded Entities |

|---|---|

| Authorized Crypto-Asset Service Providers | 280 |

| Electronic-Money Token Issuers | 21 |

| Asset-Referenced Token Issuers | 0 |

| Listed Non-Compliant Entities | 157 |

The figures are a point-in-time snapshot rather than a permanent total. ESMA updates the register as national authorities grant authorizations, record white papers and identify non-compliant entities. They should not be interpreted as 280 conventional exchanges: the CASP category also covers custody, execution, advice, transfer and other regulated services.

MiCA Register Snapshot As Of July 12, 2026, Showing 280 Authorized CASPs, 21 EMT Issuers, Zero ART Issuers And 157 Non-Compliant Entities. Add A Note That The Register Is Continuously Updated.

MiCA Is Changing Access Before Aggregate Demand

A working paper published on July 10 offers an early view of how MiCA-related restrictions are affecting stablecoin trading.

The study reports that aggregate stablecoin market shares and trading volumes changed relatively little across the broader market. The composition of activity on regulated-facing exchanges changed more noticeably. USDC’s share increased by approximately 0.82 pre-event standard deviations, while its relative trading volume rose by roughly 0.54 standard deviations, largely where USDT activity contracted following restrictions or delistings.

The result is consistent with a gateway effect.

Regulation does not have to reduce total stablecoin demand to change the market. It can redirect that demand toward approved assets, licensed venues and compliant custody channels. Global supply may remain stable while liquidity fragments across jurisdictions.

That distinction matters for traders. A stablecoin can retain a large global market capitalization while losing depth on the specific venues used by European institutions. Global circulating supply is therefore an incomplete measure of regulatory impact.

The metrics worth monitoring include:

- Stablecoin trading depth by jurisdiction.

- USDC and USDT spreads on EU-facing venues.

- Changes in quote-asset composition.

- Withdrawal routes from unauthorized platforms.

- Concentration of liquidity among authorized CASPs.

The paper is an early academic working paper rather than a final regulatory assessment. Its standardized estimates should be read as evidence of market reallocation, not as a complete measure of MiCA’s long-term effect.

Regulated Gateways Are Becoming Data Gateways

A separate July research paper examining Austrian crypto service providers shows why authorization registers matter beyond licensing.

By linking regulatory records with on-chain addresses, the researchers reconstructed Bitcoin, Ether, USDC and USDT activity associated with Austrian providers. They estimated that those firms intermediated about $30 billion with external counterparties through May 2025. Institutional counterparties accounted for a large share of value, while retail-like counterparties dominated transaction counts. The study also found that different stablecoins behaved differently during the Terra, FTX and Silicon Valley Bank disruptions.

The policy value is straightforward. Once regulated providers can be associated with verified blockchain addresses, supervisors gain a more detailed view of:

- Cross-border exposure.

- Counterparty concentration.

- Stablecoin dependence.

- Institutional and retail transaction patterns.

- Liquidity behavior during stress.

MiCA’s long-term influence may therefore come as much from better supervisory data as from licensing itself. A regulator that can connect legal entities, service permissions and blockchain activity has a stronger basis for detecting concentration and tracing risk through the market.

Bolivia Tests A Different Stablecoin Model

Bolivia’s government is technically evaluating whether USDT could operate as a recognized payment method alongside the boliviano and U.S. dollar, according to remarks reported from Economy Minister José Gabriel Espinoza on July 10. The government had not adopted a final payment framework by the end of the reporting period.

The distinction is important. Bolivia has not declared USDT legal tender. It is studying whether the stablecoin can be integrated into the country’s payment system under formal rules.

The review comes against a backdrop of currency pressure. The Central Bank of Bolivia continued adjusting its reference exchange rate during the week, while official data showed 12-month inflation of 9.23% in June.

| Policy Model | Main Objective | Regulatory Approach |

|---|---|---|

| United States | Support Private Digital Dollars While Blocking A Retail CBDC | Federal Issuer Licensing And Reserve Regulation |

| European Union | Control Access Through Authorized Providers And Approved Tokens | Comprehensive Licensing, Conduct And Distribution Rules |

| Bolivia | Explore Stablecoins As A Payment And Dollar-Access Tool | Technical Review Before Formal Payment Recognition |

For emerging markets, stablecoin policy is often driven by payment access and currency availability rather than securities regulation. That can accelerate adoption, but it also creates difficult questions around monetary sovereignty, consumer protection and dependence on a privately issued offshore asset.

What Traders And Institutions Should Watch

Venue Authorization Is Now A Market-Risk Variable

EU users should verify whether a provider appears in the ESMA register and which services that authorization covers. Brand recognition or a pending application does not replace legal authorization after the transitional deadline. ESMA explicitly advises clients of unauthorized firms to consider transferring assets to an authorized provider or self-hosted wallet.

Stablecoin Liquidity Must Be Measured Locally

MiCA’s initial effects suggest that regulation may shift trading between stablecoins without materially reducing total demand. Institutions should track depth, spreads and settlement availability on the venues they can legally use rather than relying only on global market capitalization.

U.S. Regulatory Milestones Must Be Separated By Legal Weight

The market should distinguish between:

- A regulatory agenda.

- A proposed rule.

- A final rule.

- Agency guidance.

- Committee-approved legislation.

- Enacted law.

The SEC agenda signals direction but creates no immediate obligation. The CBDC prohibition is already law. The CLARITY Act is still pending. The GENIUS Act is enacted, but much of its operational framework depends on implementing rules.

Treating those events as equivalent produces poor regulatory analysis and poor trading decisions.

Stablecoin Issuers Need A Multi-Agency Compliance Stack

A U.S. issuer preparing for the GENIUS regime will need more than reserve assets. Licensing, financial reporting, redemption procedures, AML controls, sanctions screening, custody arrangements and state-federal coordination all sit inside the emerging framework.

The strongest applicants will be those that can present a complete operating model rather than a token product waiting for regulatory approval.

| Date Or Period | Event To Monitor | Why It Matters |

|---|---|---|

| July 18, 2026 | GENIUS Act Implementation Deadline | Tests whether federal agencies can move from proposals to an operational issuer regime |

| Late July 2026 | Possible Senate Action On Market-Structure Legislation | Could clarify whether the CLARITY Act has a viable floor coalition |

| Coming Months | SEC Crypto Rule Proposals | Will reveal the practical registration path for tokens, brokers and trading venues |

| Ongoing | ESMA And National MiCA Enforcement | Unauthorized providers may face coordinated restrictions or exit requirements |

| Ongoing | Updates To The ESMA MiCA Register | Shows the pace of authorization and concentration among compliant providers |

| Unscheduled | Bolivia’s Formal USDT Decision | Would determine whether the technical review becomes payment-system policy |

The Structural Shift

The regulatory center of gravity shifted this week.

The United States is building a private-sector digital-dollar model: regulated stablecoin issuers are being brought inside a federal framework while the Federal Reserve is blocked from launching a retail CBDC without congressional approval.

Europe has moved further down the enforcement path. MiCA authorization now determines whether providers may continue acquiring clients and distributing services across the EU. Early market evidence suggests the rules are redirecting stablecoin liquidity toward compliant gateways rather than eliminating demand.

The remaining uncertainty sits mainly in market structure. The SEC is preparing its own rules while Congress continues negotiating the CLARITY Act. Until those tracks converge, firms must plan for agency-led regulation and legislative reform at the same time.

This is no longer a debate about whether crypto will be regulated. The decisive questions are who receives a license, which assets remain available through regulated channels and whether compliance costs concentrate activity among a smaller group of institutions.

Data Sources & References

- SEC Statement On The 2026 Regulatory Agenda

- Federal Unified Agenda — Securities And Exchange Commission

- H.R. 6644 Enrolled Bill Text

- Senate Banking Committee — CLARITY Act Advancement

- NCUA Proposed GENIUS Act Regulations

- OCC Proposed GENIUS Act Regulations

- FDIC Proposed GENIUS Act Regulations

- FinCEN GENIUS Act AML Proposal

- ESMA MiCA Register

- ESMA Crypto-Asset Service Provider Dataset

- ESMA Statement On The End Of The MiCA Transitional Period

- Does Regulation Bite At Gateways? Evidence From MiCA And Stablecoins

- Austrian Crypto-Asset Service Provider Transaction Study

- Central Bank Of Bolivia