Content

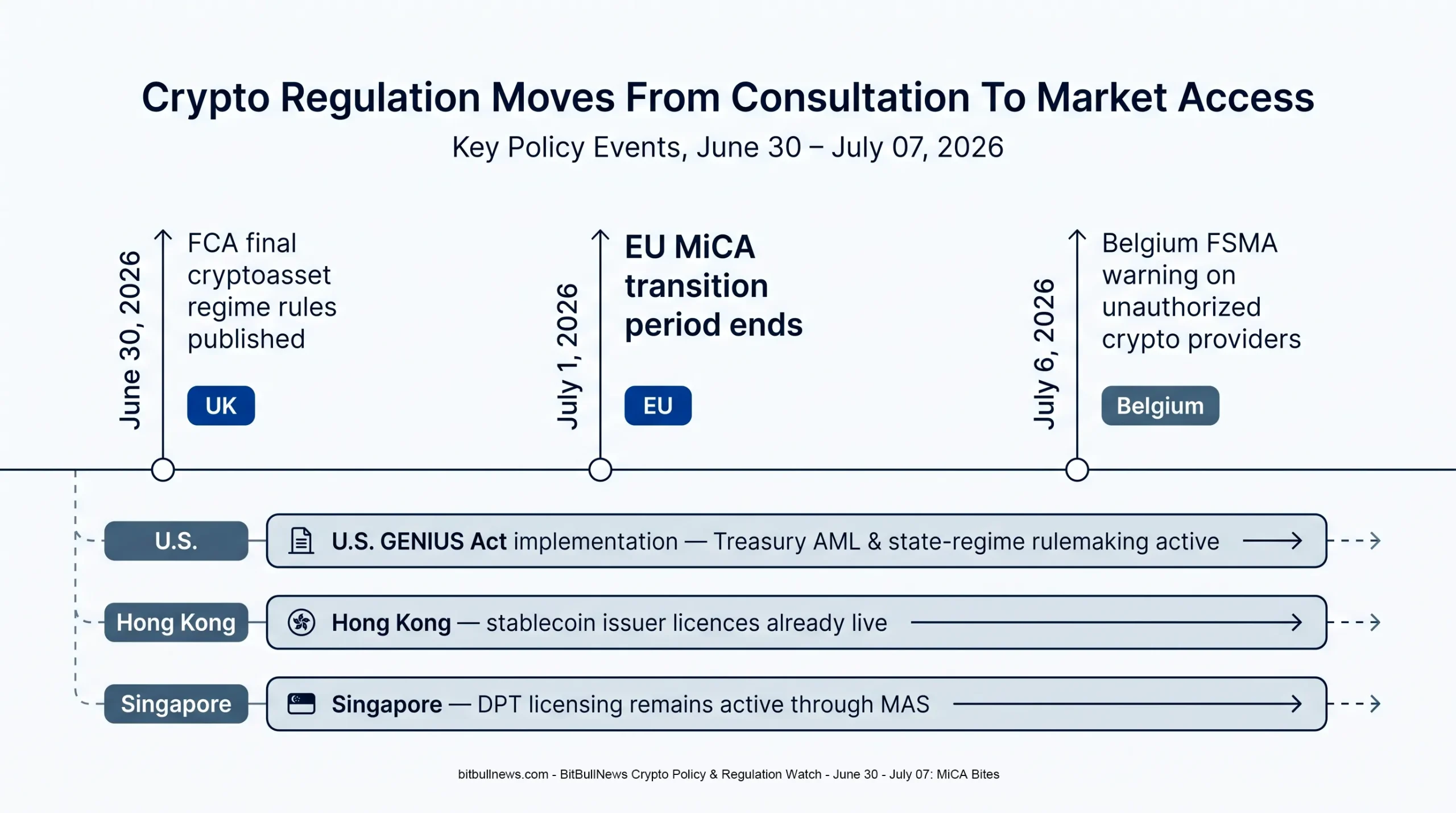

The week of June 30 – July 07, 2026 was the first real test of crypto regulation after years of consultation, political positioning, and phased implementation.

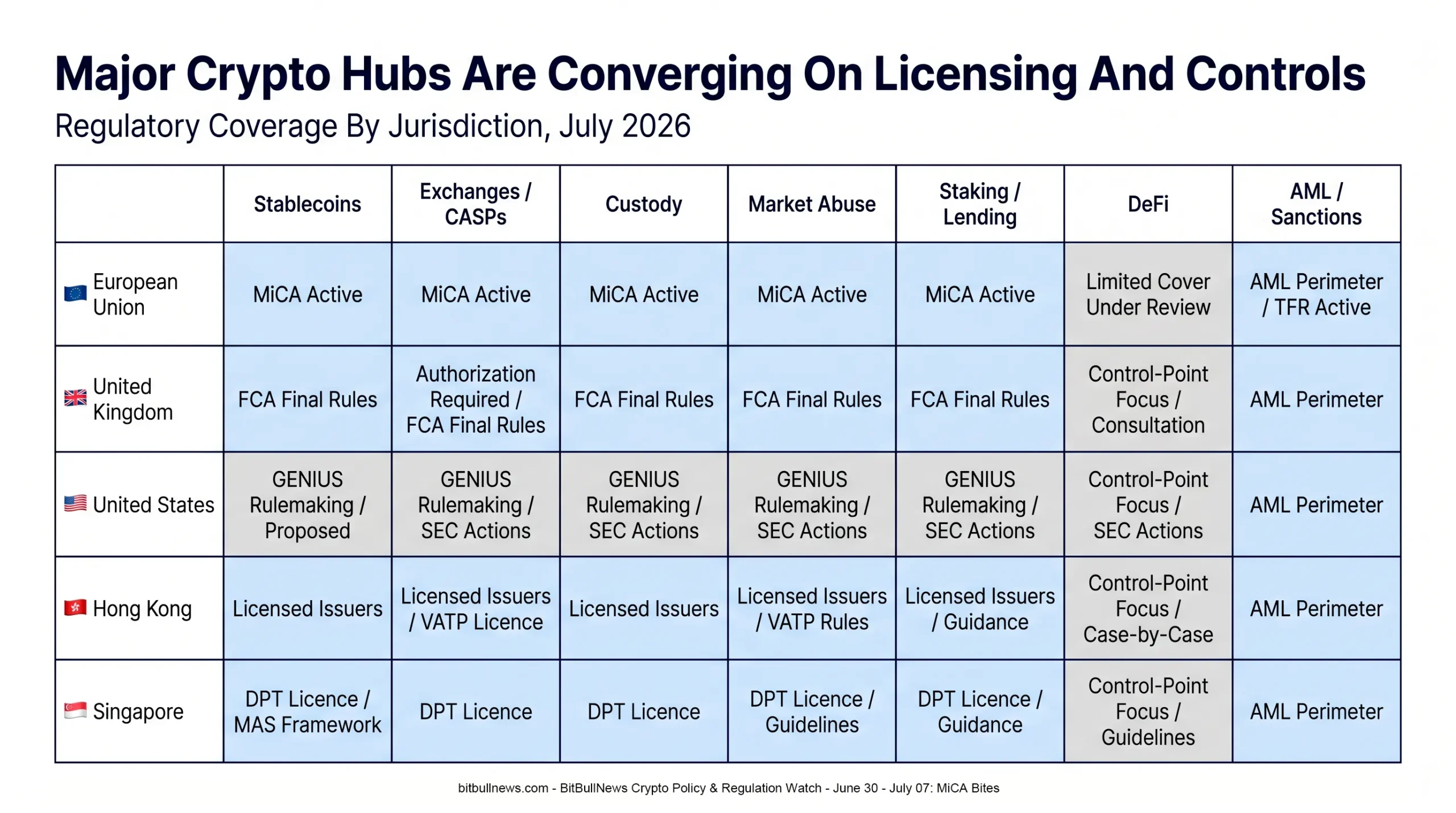

The European Union’s MiCA transition period ended on July 1, 2026, turning authorization from a future compliance project into the legal gate for serving EU clients. ESMA told unauthorized crypto-asset service providers to wind down activity in an orderly way, stop onboarding new EU clients, and protect client interests during the exit process. That is the clearest policy shift of the week: Europe moved from rule design to market access enforcement.

The United Kingdom moved in the opposite direction on timing but not on substance. On June 30, 2026, the FCA published final rules and guidance for its incoming cryptoasset regime. The full regime is expected to start on October 25, 2027, but the policy package is already detailed enough for firms to start mapping authorization, custody, stablecoin issuance, market abuse, prudential capital, staking, lending, and DeFi-control exposure.

The United States stayed focused on stablecoin implementation. Treasury continued rulemaking under the GENIUS Act, including AML and sanctions requirements for permitted payment stablecoin issuers, while the SEC’s 2026 interpretation and tokenized-securities materials continued to frame the boundary between crypto assets, payment stablecoins, commodities, and digital securities.

This is what a maturing regulatory cycle looks like. The industry is not waiting for one global rulebook. It is being split across licensing regimes.

Chart: Global Timeline Showing June 30 FCA Final Rules, July 1 MiCA Transition End, July 6 Belgium Unauthorized Provider Warning, U.S. GENIUS Act Rulemaking, And Hong Kong / Singapore Stablecoin And DPT Licensing Milestones

Global Policy Dashboard

| Jurisdiction | Weekly Signal | Key Date / Status | Market Impact |

|---|---|---|---|

| European Union | MiCA Transition Ended | July 1, 2026 | Unauthorized CASPs Must Wind Down Or Restrict EU Activity |

| United Kingdom | FCA Final Rules Published | June 30, 2026 | Firms Can Now Map The Full Authorization Burden |

| United States | GENIUS Act Implementation Continues | Treasury Rulemaking Active | Stablecoin Issuers Move Toward Financial-Institution-Style Compliance |

| Hong Kong | Stablecoin Licensing Already Live | HSBC And Anchorpoint Licensed April 10, 2026 | Selective, Institution-Led Stablecoin Market |

| Singapore | DPT Licensing Remains Active | MAS Directory Shows 38 Major Payment Institution Results For DPT Services | Crypto Access Runs Through Payments Licensing |

| FATF / Global AML | Stablecoins And Unhosted Wallets Stay In Focus | FATF Targeted Report Published March 2026 | AML Obligations Are Moving Closer To P2P And Wallet-Level Risk |

The common thread is access control. The EU is cutting off unauthorized service providers. The UK is preparing a comprehensive FSMA-based perimeter. The U.S. is building a stablecoin compliance stack. Hong Kong and Singapore are limiting access through issuer and payment-licensing channels. FATF is pushing AML pressure toward stablecoins, P2P transfers, and unhosted-wallet exposure.

Why This Week Matters

Crypto regulation usually moves slowly, then all at once. This week was one of those “all at once” moments.

The EU did not just publish another warning. It ended the transition period. ESMA’s statement says unauthorized CASPs must take immediate steps to wind down their EU activities, stop onboarding new EU clients, and only permit actions that protect client interests, such as withdrawals, transfers, or closing positions. That turns licensing status into a live market-structure factor.

The market impact is practical. Users may lose access to unlicensed venues. Exchanges may need to geofence or migrate customers. Token listings may become more conservative. Licensed providers gain a distribution advantage because authorization now carries commercial value, not just regulatory credibility.

At the same time, the UK’s new regime gives firms a long runway but less room to hide. The FCA’s package covers admissions and disclosures, market abuse, stablecoin issuance, regulated cryptoasset activities, prudential requirements, and application of the FCA Handbook. The regulator also confirmed that key obligations such as Consumer Duty, conduct rules, SM&CR, operational resilience, and financial crime frameworks will apply across regulated cryptoasset activities.

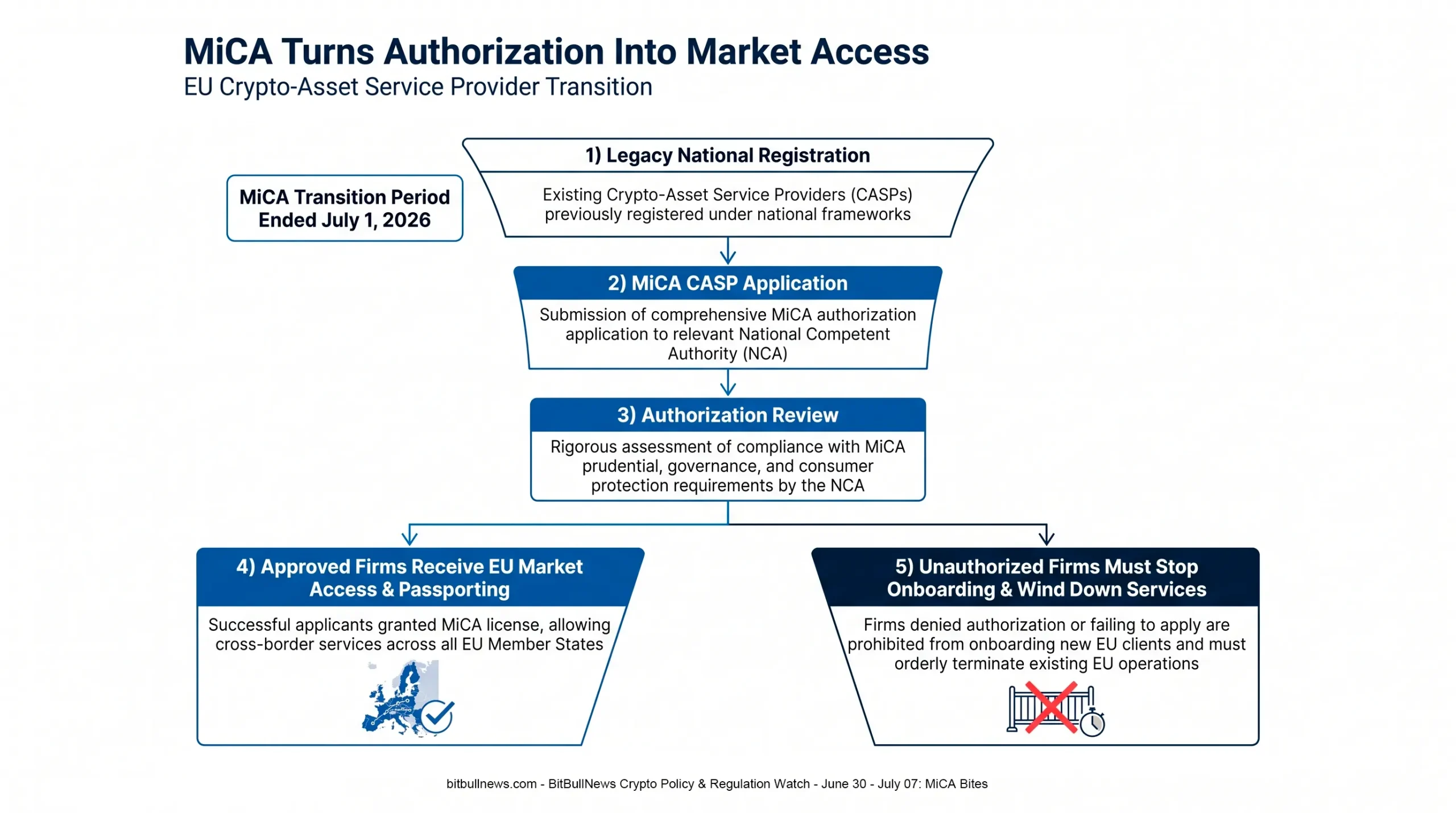

European Union: MiCA Becomes A Market Access Filter

MiCA’s transition period ended across the EU on July 1, 2026. ESMA warned that firms without MiCA authorization cannot treat legacy national registration as a continuing passport into the bloc. The regulator also told unauthorized providers to wind down in a way that protects clients, rather than forcing a disorderly break.

| MiCA Area | Post-July 1 Status | What It Means |

|---|---|---|

| CASP Authorization | Required For Serving EU Clients | Licensing Becomes The Legal Access Gate |

| Legacy National Regimes | Transitional Use Ended | Old Registration Paths No Longer Carry The Same Operating Value |

| Client Treatment | Orderly Wind-Down Expected | Users Should Be Able To Withdraw, Transfer, Or Close Positions |

| New EU Client Onboarding | Unauthorized Firms Expected To Stop | Growth In The EU Shifts Toward Licensed Firms |

| Supervisory Convergence | ESMA Remains Focused On Harmonized Application | National Arbitrage Becomes A Policy Risk |

The first enforcement signals arrived quickly. Belgium’s FSMA reminded the market that only CASPs may offer crypto-asset services and that certain non-CASP entities could operate only until June 30, 2026 under the transitional regime. Market reporting during the week also said the Belgian regulator flagged six unauthorized crypto providers after the MiCA deadline took effect.

The commercial read is simple: MiCA turns authorization into a customer-acquisition tool. A licensed exchange or custodian can now market regulatory continuity. An unlicensed provider must explain why EU users should stay through an exit process.

Chart: EU MiCA Enforcement Funnel Showing Legacy Registration, CASP Application, Authorization Review, Passporting For Approved Firms, And Wind-Down For Unauthorized Firms After July 1, 2026

United Kingdom: The FCA Publishes The Real Rulebook

The FCA’s June 30 package is the most detailed regulatory document set of the week.

The regulator published final policy statements for admissions and disclosures, market abuse, stablecoin issuance, regulated cryptoasset activities, prudential requirements, and application of the FCA Handbook. The full scope of the regime is expected to expand from October 25, 2027, giving firms time to prepare, but the direction is already fixed: crypto activity in the UK is moving from AML registration and financial-promotion controls into a full financial-services perimeter.

| FCA Rule Area | What Changed | Institutional Read |

|---|---|---|

| Admissions And Disclosures | Final A&D And MARC Framework Published | Token Listing Becomes A Controlled Disclosure Event |

| Stablecoin Issuance | Backing Assets, Safeguarding, Redemption, And Holder Disclosure Rules Finalized | Issuers Need Treasury-Grade Reserve Controls |

| Custody | CASS 17 Safeguarding Requirements For Cryptoasset Custodians | Custody Becomes A Formal Control Function |

| Staking / Lending | Activity-Specific Rules Included Under Regulated Cryptoasset Activities | Product Design Must Match Regulatory Classification |

| Prudential Rules | COREPRU And CRYPTOPRU Frameworks Introduced | Capital Planning Becomes Part Of Crypto Operations |

| DeFi | Rules Apply Where There Is An Identifiable Controlling Entity | “Decentralized” Label Alone Will Not Avoid The Perimeter |

Stablecoin rules are especially important. The FCA confirmed statutory trust arrangements for backing assets, adjusted redemption timelines, allowed limited intragroup custody subject to safeguards, and permitted up to a 5% excess in the backing asset pool. These are not cosmetic details. They define how an issuer must hold, protect, and redeem backing assets in a regulated market.

The DeFi language may become one of the most copied parts of the UK approach. The FCA says rules and guidance will apply to DeFi firms where there is an identifiable controlling entity. That puts attention on front ends, governance structures, administrators, upgrade keys, fee capture, and operational control rather than protocol branding.

United States: Stablecoins Stay At The Center

The U.S. policy cycle remains more stablecoin-first than Europe’s or the UK’s.

Treasury’s GENIUS Act rulemaking is focused on permitted payment stablecoin issuers, including AML and sanctions compliance program requirements. The proposed AML and sanctions rule treats stablecoin issuers as part of the financial-crime perimeter rather than as technology companies sitting outside it.

Treasury also proposed how state-level regulation can work under the GENIUS Act. Payment stablecoin issuers with consolidated outstanding issuance of not more than $10 billion may opt into a qualifying state-level regime if that regime is substantially similar to the federal framework. That threshold matters because it creates a two-tier path: smaller issuers may stay closer to state supervision, while larger issuers face the federal baseline more directly.

The SEC’s 2026 interpretation adds another boundary. It references payment stablecoins issued by permitted payment stablecoin issuers separately from other non-security crypto assets, and it clarifies how federal securities laws apply to certain crypto assets and transactions. The SEC’s public materials on digital securities also state that tokenized securities remain securities when ownership records are maintained through crypto networks.

For U.S. firms, the message is not “regulation is over.” It is more precise: stablecoins have a federal implementation path; securities classification still depends on structure; tokenization does not erase the legal nature of the underlying instrument.

Asia: Hong Kong And Singapore Keep Access Narrow

Hong Kong’s stablecoin regime is already live. The HKMA granted stablecoin issuer licences to Anchorpoint Financial Limited and The Hongkong And Shanghai Banking Corporation Limited on April 10, 2026, and the HKMA register is the public list of licensed issuers under the Stablecoins Ordinance.

The licensing outcome is notable because it was selective. HKMA said licences were granted to Anchorpoint and HSBC from a group of 36 applications, and both licensed issuers initially planned Hong Kong dollar-referenced stablecoins. That suggests Hong Kong is not chasing a broad issuer land rush. It is building a bank-grade, controlled stablecoin channel.

Singapore remains payments-led. MAS’s Financial Institutions Directory showed 38 results for Digital Payment Token Service under Major Payment Institution status during the period. That does not mean Singapore is open to every crypto firm; it means access is formalized through payments licensing rather than informal market entry.

| Market | Regulatory Channel | Current Public Signal | Strategic Meaning |

|---|---|---|---|

| Hong Kong | Stablecoin Issuer Licence | HSBC And Anchorpoint Licensed | Institution-Led Stablecoin Rollout |

| Hong Kong | HKMA Public Register | Register Maintained Under Stablecoins Ordinance | Users Can Verify Licensed Issuers |

| Singapore | Major Payment Institution Licence | 38 DPT-Service Results In MAS Directory | DPT Access Runs Through Payments Supervision |

| Singapore | Stablecoin Framework | Single-Currency Stablecoin Rules Remain Relevant | Issuers Must Fit A Formal Monetary Framework |

Asia’s pattern is controlled experimentation. Hong Kong is making stablecoin issuance institution-led. Singapore is keeping digital payment token activity inside a payments framework. Neither is a free-for-all.

AML And Wallet Risk: The Pressure Is Moving Down The Stack

The FATF’s 2026 targeted report on stablecoins and unhosted wallets remains highly relevant to this week’s policy moves. The report highlights illicit-finance risks linked to stablecoin misuse, especially peer-to-peer transactions through unhosted wallets, and recommends stronger controls for countries and the private sector.

This is where the next fight sits. MiCA can license CASPs. The FCA can authorize trading platforms and custodians. Treasury can supervise permitted stablecoin issuers. But value can still move through self-custody, P2P transfers, smart contracts, bridges, and DeFi interfaces.

That does not mean regulators will ban self-custody. It means they will look harder for control points:

- Issuer redemption and blacklisting policies.

- CASP wallet-screening obligations.

- Travel Rule implementation.

- Front-end control in DeFi.

- Stablecoin mint and burn counterparties.

- Smart-contract governance and upgrade authority.

The regulatory perimeter is moving from “who runs the exchange?” to “who controls the transaction pathway?”

Market Scale: Why Regulators Are Moving Now

This is no longer a small market. DefiLlama showed total stablecoin market capitalization around $311.95 billion, with USDT dominance near 59%, while CoinGecko tracked more than 12,800 coins and roughly 1,490 exchanges in its global market dataset.

| Market Signal | Public Reading | Policy Relevance |

|---|---|---|

| Stablecoin Market Cap | $311.95B | Dollar-Linked Crypto Liquidity Is Systemically Relevant To Digital Markets |

| USDT Dominance | 59.02% | Issuer Concentration Creates Market-Structure Risk |

| CoinGecko Tracked Coins | 12,841 | Token Classification Cannot Be Handled Asset By Asset Manually |

| CoinGecko Tracked Exchanges | 1,494 | Exchange Supervision Is A Cross-Border Problem |

| MAS DPT Major Payment Institution Results | 38 | Regulated Access Channels Are Becoming More Visible |

This scale explains the policy shift. Regulators are no longer only reacting to fraud after collapse. They are setting operating conditions before firms serve customers.

Chart: Regulatory Coverage Matrix Comparing EU, UK, U.S., Hong Kong, And Singapore Across Stablecoins, Exchanges / CASPs, Custody, Market Abuse, Staking / Lending, DeFi, And AML

What Changed In Market Structure

The biggest structural change this week is that regulatory status became a live commercial variable.

In the EU, a MiCA licence is now a market-access instrument. It affects whether a platform can onboard clients, provide services, and compete for customer migration from unlicensed firms. In the UK, the FCA’s final rules let firms price the cost of authorization before the regime starts. In the U.S., stablecoin issuers can no longer treat compliance design as optional because AML, sanctions, reserve, and supervisory frameworks are moving through implementation.

The second change is product governance. Token listings, stablecoin reserves, custody models, staking products, lending programs, and DeFi front ends are no longer just product decisions. They are legal-risk decisions.

The third change is geography. Crypto firms can still be global, but their access model is becoming local. A firm can be viable in one jurisdiction, restricted in another, and forced to redesign product access in a third.

Actionable Signals For Traders, Investors, And Crypto Firms

| Audience | Signal To Watch | Why It Matters |

|---|---|---|

| Traders | EU Exchange Access Restrictions | Liquidity Can Fragment When Unlicensed Venues Limit EU Clients |

| Investors | Stablecoin Issuer Licensing And Reserve Rules | Redemption Quality Matters More As Stablecoins Become Regulated Money Instruments |

| Exchanges | MiCA And FCA Authorization Strategy | Licensing Determines Whether Growth Markets Remain Open |

| DeFi Teams | Identifiable Control Points | Front Ends And Governance Structures Can Pull Protocols Into The Perimeter |

| Custodians | UK CASS And Operational Resilience Requirements | Institutional Clients Need Regulated Safeguarding Standards |

| Policymakers | Cross-Border Client Migration | Strict Domestic Rules Can Leak Through Offshore Access Unless Supervision Is Coordinated |

For traders, the short-term signal is access risk. A token can remain globally liquid while becoming harder to access in Europe. That matters for spreads, routing, and venue selection.

For investors, the key signal is counterparty quality. A licensed exchange, regulated custodian, and transparent stablecoin issuer now carry strategic value.

For firms, delay is becoming expensive. Authorization work is no longer a legal side project. It is part of market entry.

Key Anomalies To Watch

The first anomaly is the EU’s authorization cliff. ESMA is pushing orderly wind-down, but customer migration can be messy. Retail users may be slow to respond, offshore firms may retain passive accounts, and national regulators may apply pressure unevenly.

The second anomaly is the UK timing gap. The FCA has published detailed rules, but the regime does not start until October 2027. That creates a period where UK firms know the direction but still operate under today’s more limited perimeter.

The third anomaly is stablecoin divergence. The U.S. is building a dollar-stablecoin framework around permitted payment stablecoin issuers. The EU treats stablecoins through MiCA’s ART and EMT architecture. Hong Kong is starting with a small number of licensed issuers. These systems are converging around reserves and supervision, but they are not identical.

The fourth anomaly is DeFi. The FCA’s identifiable-controlling-entity approach is practical, but difficult. Control can sit across governance tokens, foundations, multisigs, front ends, relayers, legal entities, and fee flows. The next phase of regulation will need tests that are specific enough to enforce and flexible enough not to misclassify genuinely decentralized systems.

BitBullNews View

This week marks the end of soft-launch crypto regulation in major financial centers.

The EU has moved into authorization enforcement. The UK has published its full future rulebook. The U.S. is turning stablecoin law into operational compliance. Hong Kong and Singapore are keeping access controlled through licensed issuers and payment institutions.

That is not anti-crypto. It is anti-informal crypto.

The winners are firms with licensing discipline, custody controls, reserve transparency, legal clarity, operational resilience, and credible governance. The losers are firms that relied on regulatory lag, offshore ambiguity, loose token listings, or “decentralized” branding without real decentralization.

Crypto is still global. Access to regulated markets is becoming local, licensed, and much less forgiving.

What To Watch Next

The first watch item is EU client migration. If unauthorized platforms restrict accounts without smooth withdrawals or transfers, MiCA’s first enforcement phase could create operational friction for users.

The second watch item is the FCA’s preparation track. The UK regime starts in 2027, but firms need to map authorization requirements now, especially if they operate trading, custody, staking, lending, or stablecoin activities.

The third watch item is U.S. GENIUS Act implementation. Reserve rules, AML programs, sanctions controls, and state-versus-federal pathways will determine whether stablecoin issuance consolidates around large institutions or leaves room for smaller issuers.

The fourth watch item is DeFi perimeter guidance. The next meaningful regulatory battle will not be whether DeFi exists. It will be who controls it, who profits from it, and who can be held responsible when users are harmed.

Data Sources & References

- FCA — Overview Of Cryptoasset Regime Policy Statements

- FCA — A New Regime For Cryptoasset Regulation

- ESMA — Public Statement On MiCA Transitional Period Ending

- ESMA — Statement On The End Of Transitional Periods Under MiCA

- Belgian FSMA — Crypto-Asset Service Provider Information

- U.S. Treasury — GENIUS Act AML And Sanctions Proposed Rule

- U.S. Treasury — GENIUS Act State-Level Regulatory Regime Notice

- SEC — Application Of Federal Securities Laws To Certain Crypto Assets

- SEC — Crypto Assets And Federal Securities Laws

- SEC — Staff Statement On Tokenized Securities

- HKMA — Register Of Licensed Stablecoin Issuers

- HKMA — Granting Of Stablecoin Issuer Licences

- MAS — Financial Institutions Directory, Digital Payment Token Service

- FATF — Targeted Report On Stablecoins And Unhosted Wallets

- DefiLlama — Stablecoin Market Cap And Issuer Data

- CoinGecko — Global Crypto Market Charts