Content

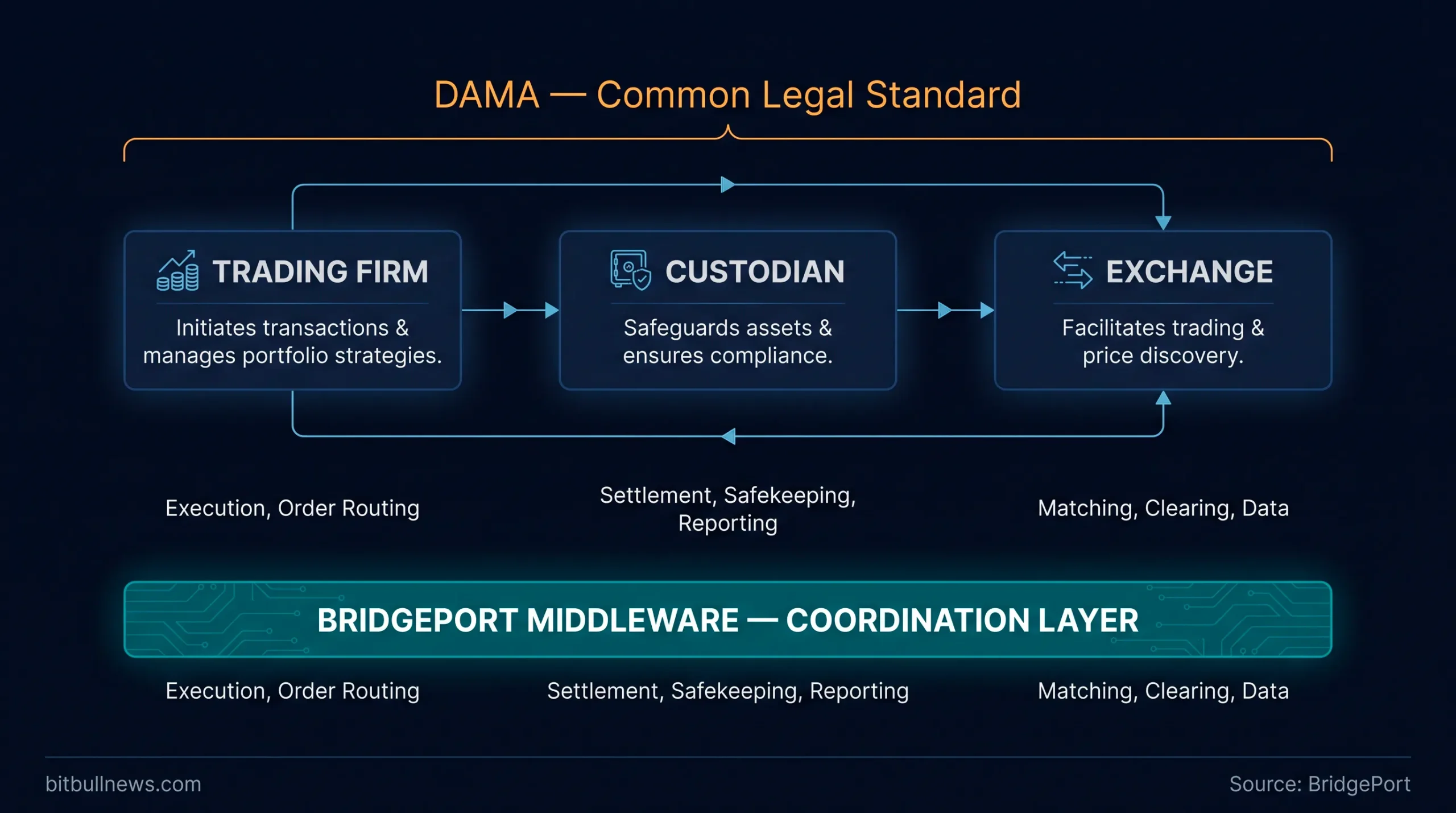

BridgePort, the middleware coordination layer for institutional crypto, is piloting the Digital Asset Master Agreement (“DAMA”) — a common legal standard for off-exchange settlement (“OES”) relationships between trading firms, custodians, and exchanges. The New York-based firm confirmed the pilot in an official announcement on July 14, 2026.

The framework takes its inspiration from the ISDA Master Agreement, the document that standardized derivatives trading decades ago. And the ambition is similar: replace bespoke, months-long legal negotiations with a reusable foundation that firms configure rather than rebuild.

BitBullNews put a detailed set of questions to the company. Steve Bartfield, Chief Product Officer of BridgePort, answered them in full — including on governance, venue insolvency, and the timeline for live adoption.

Key Takeaways

- DAMA is a configurable master agreement for tri-party OES arrangements between trading firms, custodians, and trading venues.

- A working group is forming now, with BridgePort coordinating feedback and targeting consensus among participants this fall.

- The standard is intended to be open. Using BridgePort’s middleware is not a requirement, and the access and licensing framework is being finalized.

- Venue insolvency — the scenario that pushed institutions toward OES in the first place — is addressed explicitly in the document.

- Over the next 12 to 24 months, success means legal documentation becoming a routine onboarding step rather than a barrier.

Why Off-Exchange Settlement Needed A Common Rulebook

Off-exchange settlement lets a trading firm keep its assets with a qualified custodian while trading across multiple exchanges. Capital stays in one place, counterparty exposure to any single venue shrinks, and collateral works harder.

The catch has always been paperwork. Each new OES arrangement is a three-way legal negotiation between a trading firm, a custodian, and a venue — and each one has typically been drafted from scratch. According to the announcement, these onboarding cycles are costly and can take months to resolve.

The infrastructure for off-exchange settlement is largely in place

BridgePort CEO Nirup Ramalingam said in the release. In his view, the next phase of the market depends on standardizing the legal foundation underneath that infrastructure, as every institutional market has eventually done.

What DAMA Actually Standardizes

DAMA is built on a shared set of definitions and contractual provisions covering the terms counterparties would otherwise negotiate independently for every new relationship. The company groups the framework into four areas:

- Custody. How collateral is safeguarded and segregated, and whether it is held in trust or pledged under a security interest.

- Settlement. How settlement credit is extended against collateral, how balances are reconciled, and how the settlement cycle runs.

- Operations. How operational failures are handled, including erroneous transfers, failed settlements, and outages in the balance feed between custodian and venue.

- Default And Termination. What counts as a default — including venue insolvency or failure — and how close-out, termination, and the return of collateral proceed.

Flexibility is deliberate. Participants can tailor key provisions — from collateral structure to whether the agreement plugs into an existing ISDA relationship or stands alone — without rewriting the document.

The most contested design choice? Bartfield points to collateral structure. “Trust versus security interest is a good example of why the structure needs to be flexible,” he told BitBullNews, noting that different participants and jurisdictions require different approaches, which DAMA supports through elections and annexes.

Inside The Working Group

BridgePort is now assembling a working group of trading firms, custodians, and exchanges to pilot DAMA across live OES relationships. Names are not being disclosed yet — the company says it cannot identify firms without their permission — but interest is broad across its network.

The process is already mapped out. Interested participants will review the existing documentation, and BridgePort will coordinate feedback and work toward consensus among the parties this fall.

Bartfield frames the initiative as demand-driven rather than top-down. “It addresses a problem our participants face today, and they are asking for an industry-wide solution,” he said in response to our inquiry.

An Open Standard, Not A Product Lock-In

A natural question for any vendor-initiated standard is whether it doubles as a sales funnel. BridgePort’s answer is direct: DAMA is intended to be an open industry standard, and firms will not need the company’s middleware to use it.

The governance model follows the same logic. Proposed changes go through the working group, which reviews them and works toward consensus as the standard evolves. The specific access and licensing framework is still being finalized.

Bartfield also addressed why a commercial participant is convening the effort at all. BridgePort connects trading firms, custodians, and exchanges but does not execute trades, hold assets, or act as a counterparty to these agreements — and today, no single industry body represents all three constituencies involved in OES.

The door is open to established bodies, too. The company says it would welcome participation from ISDA, GDF, or any other industry organization looking to extend its coverage into off-exchange settlement. And on the question of incentives, Bartfield is transparent: BridgePort benefits when OES becomes easier to adopt, but it does not set the commercial terms or risk allocation in these agreements — credibility, he argues, will come from open use, participant-led governance, and broad adoption.

The Legal Fine Print: Governing Law, Insolvency, And Enforceability

The initial version of DAMA was developed by BridgePort in consultation with existing OES participants, drawing on established market standards and referencing ISDA concepts where appropriate. Governing law is selected by the parties to each agreement.

Independent legal opinions on enforceability have not yet been commissioned. That work is being handed to the working group, which will identify the jurisdictions and issues where formal opinions would be most useful — a sequencing consistent with how earlier market standards matured.

Venue insolvency gets explicit treatment, and for good reason: it is the scenario that drove institutions toward OES in the first place. DAMA does not replace applicable insolvency law. Instead, it establishes in advance the contractual treatment of assets and the steps each party takes if a venue fails.

Loss allocation is not one-size-fits-all. As Bartfield explained to BitBullNews, outcomes depend on the agreed structure, the circumstances of the failure, and applicable law — the standard defines rights and procedures rather than prescribing a single formula.

From Months Of Negotiation To Reusable Legal Work

Where does the “months” figure come from? Bartfield says it reflects BridgePort’s direct experience negotiating and implementing these relationships at exchanges and trading firms, reinforced by feedback across its OES network. Timelines vary, but one pattern repeats: firms keep negotiating substantially the same language.

DAMA is designed to standardize that repeatable language. The first review by a firm’s legal team may still take time. But that work becomes reusable as the firm adds new custodians, exchanges, or counterparties — leaving only the terms that genuinely differ on the table.

That reuse effect compounds across the market. In the release, Bartfield noted that widely adopted frameworks give market participants, law firms, and industry organizations a reason to build shared legal analysis and operational expertise instead of recreating it for every relationship.

What Comes After The Legal Layer

BridgePort’s platform is built to make many venues behave like one market from the perspective of credit, collateral, and settlement. Institutions separate where they trade from where they carry risk, so liquidity stays distributed while risk management runs through a common network.

With the technical and orchestration layers handled by the platform and the legal layer addressed by DAMA, one challenge remains: coordinated adoption. Trading firms still need to establish the necessary custodial relationships and standardize workflows that are currently fragmented across systems.

The Road To A De Facto Standard

ISDA needed years to become the norm in derivatives, and BridgePort is not claiming it will replicate that breadth. DAMA targets the narrower requirements of OES while building on the groundwork ISDA laid.

The 12-to-24-month benchmark is pragmatic. Success, per Bartfield, means legal documentation becoming a routine, predictable step in onboarding rather than a barrier to launching new relationships. Full background documentation on DAMA is available here.