Content

The most important tokenization event this week was not another fund launch. It was the U.S. market’s core securities depository moving tokenized assets closer to production.

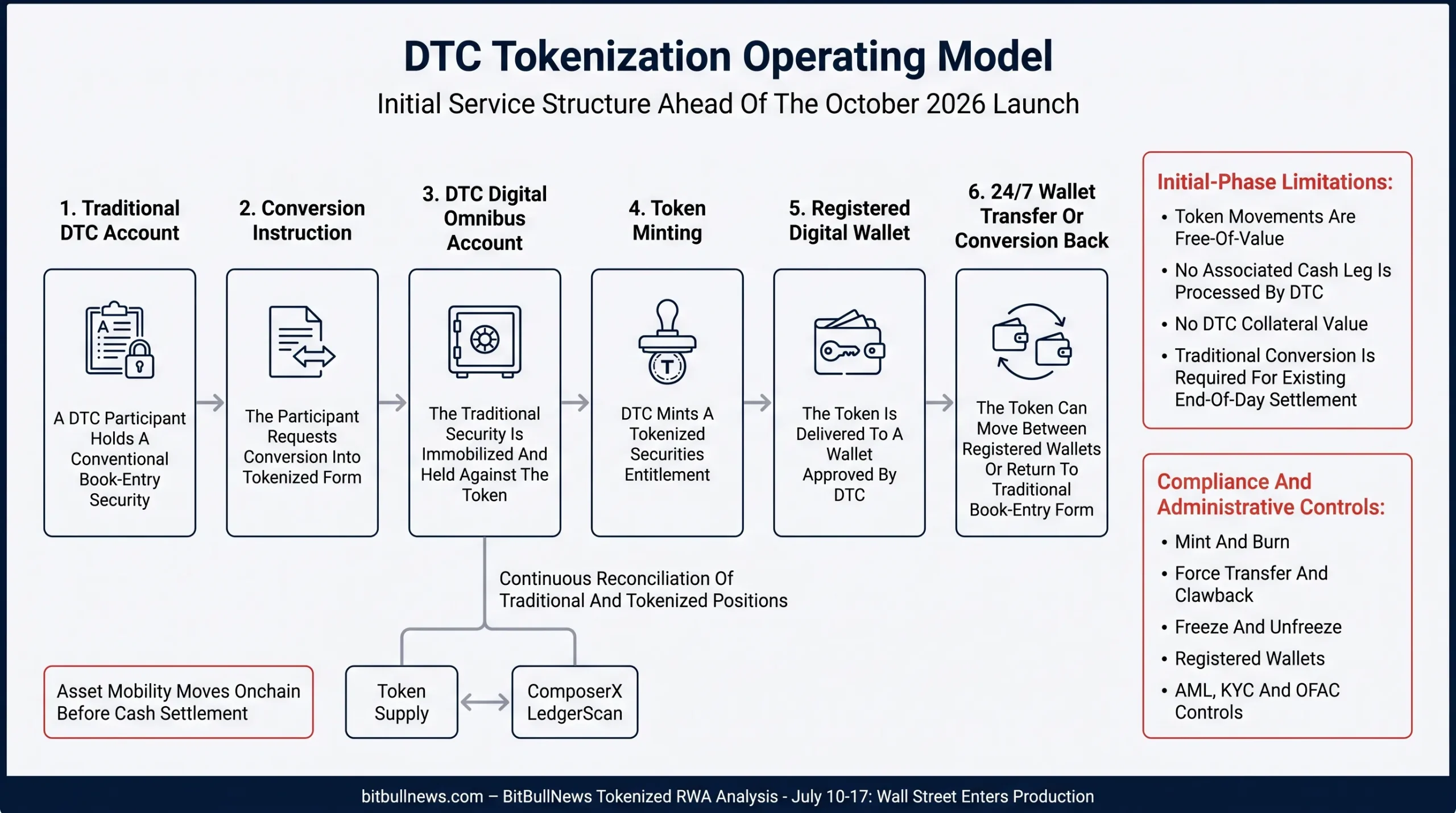

On July 15, the Depository Trust & Clearing Corporation completed a major milestone in the development of its tokenization service. Nearly 40 financial institutions and technology firms participated in the exercise, including JPMorgan, Goldman Sachs, BlackRock, Vanguard and the New York Stock Exchange. The securities selected for tokenization included public-company shares, major exchange-traded funds and U.S. Treasuries. A formal service launch remains scheduled for October.

The milestone changes the institutional RWA discussion. Tokenization is no longer confined to specialist issuers placing Treasury funds or private-credit instruments on public blockchains. It is entering the infrastructure that already records, services and settles mainstream U.S. securities.

The public-chain market continued growing at the same time, but the data carried a warning. Tokenized stock and commodity values increased while transfer activity and active-address counts contracted. More assets are being represented onchain, yet that does not automatically mean deeper secondary liquidity.

RWA Market Scorecard

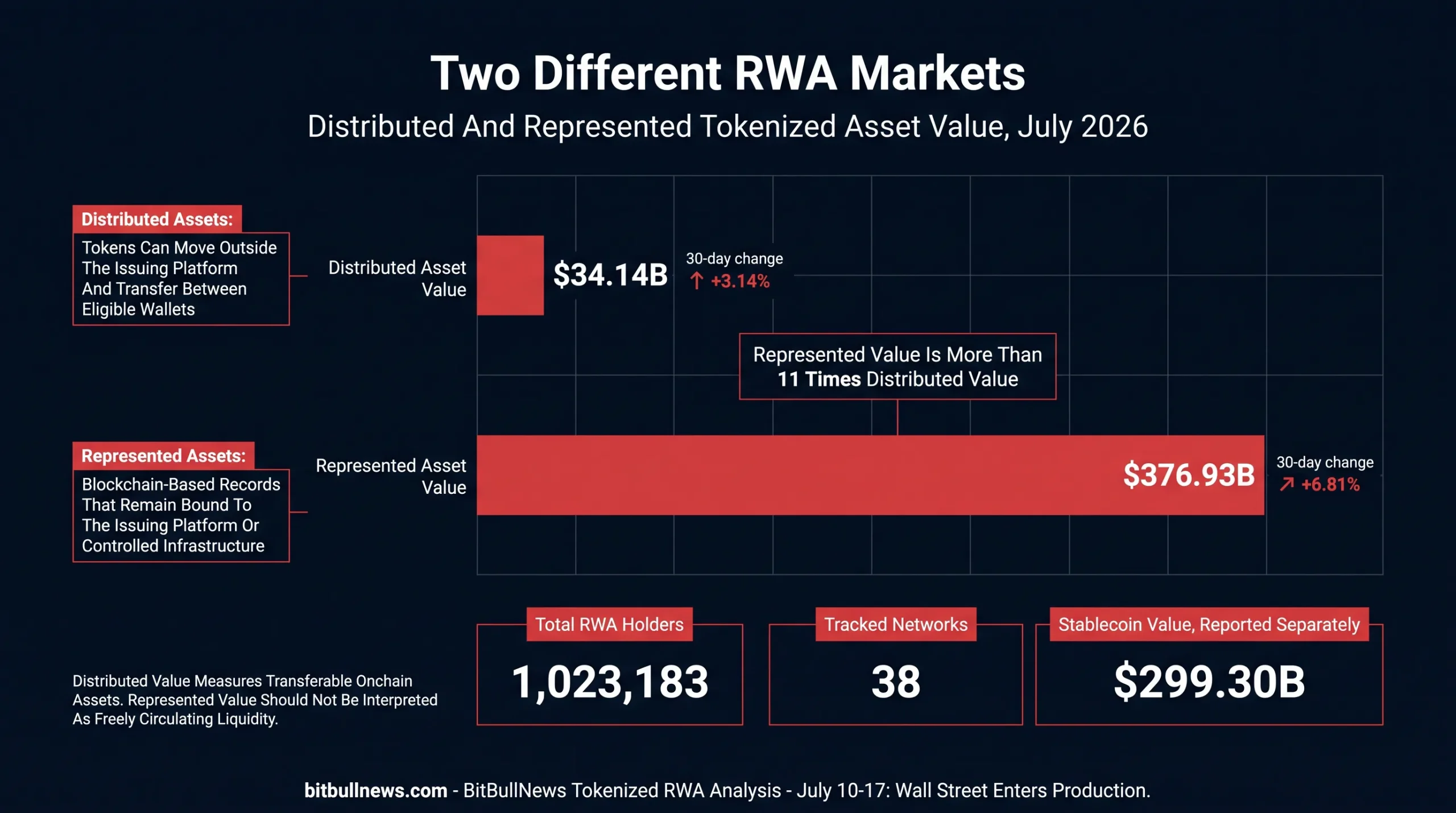

The latest RWA.xyz network snapshot showed $34.14 billion of distributed asset value and $376.93 billion of represented asset value. The market included more than 1.02 million RWA holders across 38 tracked networks. Stablecoins, reported separately, accounted for another $299.30 billion.

| Market Metric | Current Reading | 30-Day Change | Market Read |

|---|---|---|---|

| Distributed Asset Value | $34.14B | +3.14% | Transferable onchain assets continued expanding |

| Represented Asset Value | $376.93B | +6.81% | Institutional recordkeeping structures grew faster |

| Total RWA Holders | 1,023,183 | +11.63% | Ownership expanded faster than distributed value |

| Stablecoin Value | $299.30B | +0.51% | Payment-token growth remained comparatively slow |

| Tracked Networks | 38 | — | Issuance remains spread across a growing infrastructure base |

RWA.xyz classifies an asset as distributed when it can move outside the issuing platform and transfer between eligible wallets. A represented asset remains platform-bound, with blockchain used mainly for recordkeeping, reconciliation or controlled institutional workflows. The distinction separates assets designed for external onchain circulation from assets using distributed ledgers as a modernized back-office layer.

That difference is now central to market analysis. Represented value is more than 11 times larger than distributed value, but it should not be read as freely circulating onchain liquidity. The larger figure shows how quickly institutions are adopting blockchain-based records. The smaller figure is closer to the capital that can actually move through external wallets and onchain applications.

Two-Bar Comparison Showing Distributed RWA Value At $34.14B And Represented RWA Value At $376.93B. Add A Secondary Row Showing 1.02M RWA Holders And 38 Networks. Clearly Define Distributed As Externally Transferable And Represented As Platform-Bound.

Asset Growth Broadened Beyond Treasuries

Tokenized Treasuries remain the largest readily transferable financial RWA category, but they were not the fastest-growing segment in the latest public snapshots.

Active investment strategies grew 13.02% over 30 days. Tokenized stocks increased 12.56%, while commodities gained 7.43%. Credit expanded 4.44%. Treasury growth was much slower at 1.25%.

| Asset Class | Current Distributed Value | 30-Day Change | Additional Market Metric |

|---|---|---|---|

| U.S. Treasuries | $15.16B | +1.25% | 3.48% average seven-day APY |

| Commodities | $7.46B | +7.43% | $12.76B monthly transfer volume |

| Credit | $7.03B | +4.44% | $35.63B represented value |

| Active Strategies | $1.77B | +13.02% | 29,031 holders |

| Stocks | $1.08B | +12.56% | 190,610 holders |

| Real Estate | $176.96M | -0.38% | $279.84M represented value |

Data note: RWA.xyz category pages refresh on different schedules. Treasury figures were displayed with a July 11 market snapshot, while credit and active-strategy pages showed July 17 data. The values should not be mechanically summed to recreate the overall network dashboard.

The broader growth pattern matters. Tokenized RWAs are moving beyond the original cash-equivalent trade in which issuers placed short-duration government debt onchain for crypto-native investors seeking dollar yield.

That trade remains the market’s foundation. The faster-growing categories now include managed portfolios, public-equity exposure, credit strategies and commodity-backed tokens. The market is adding economic diversity even though liquidity remains concentrated in a relatively small number of products.

DTCC Moves Tokenization Into Existing Market Infrastructure

DTCC’s July 15 milestone is different from most RWA launches because it does not create a separate synthetic market alongside conventional securities.

DTC-issued tokens are designed to share the same CUSIP and carry the same legal and economic rights as the corresponding traditional securities. Participants will be able to move assets between conventional and tokenized form rather than holding a disconnected wrapper that merely tracks the price of an underlying asset. DTCC also plans to preserve corporate-action rights, including dividends and other benefits, in both forms.

This structure addresses one of the largest risks in tokenized securities: the gap between the token and the legal claim.

The SEC has distinguished issuer-sponsored tokenized securities from third-party custodial and synthetic structures. In a custodial model, the token may represent an indirect entitlement to an underlying security. In a synthetic model, the token can provide economic exposure without giving the holder ownership, voting or other rights against the original issuer.

DTCC’s design keeps the token inside the existing securities-entitlement system. That makes the blockchain record an extension of regulated market infrastructure rather than a substitute for it.

Production Does Not Yet Mean Fully Onchain Settlement

The initial service still has important limitations.

Registered DTC participants will be able to move tokens between approved digital wallets 24/7, but those movements will initially be free-of-value. DTC will not process the corresponding cash leg onchain, and tokenized securities will not receive collateral or end-of-day settlement value within DTC’s risk-management system. A participant that wants to use the asset in traditional settlement will need to convert it back into a conventional book-entry entitlement.

That means the first phase improves asset mobility and recordkeeping, but it does not deliver full atomic delivery-versus-payment.

| DTCC Tokenization Feature | Initial Capability | Remaining Limitation |

|---|---|---|

| Legal Ownership | Same legal and economic rights as traditional form | Rights still depend on established DTC structure |

| Token Transfers | 24/7 transfers between registered wallets | Transfers are initially free-of-value |

| Corporate Actions | Supported in traditional and tokenized form | Some actions may still process offchain |

| Cash Settlement | Not included in initial token movement | No native onchain payment leg |

| Collateral Treatment | Token can be held and transferred | No DTC collateral value in the first phase |

| Conversion | Traditional securities can be converted into tokens and back | Traditional conversion required for existing end-of-day settlement |

| Compliance | Registered wallets, controls and monitoring | Participation remains permissioned |

DTCC retains administrative controls over the tokens, including minting, burning, force transfers, clawbacks, freezes and pauses. Its LedgerScan system will reconcile onchain token movements against the securities held in DTC’s digital omnibus account.

Those controls may disappoint investors expecting permissionless securities. They are also the reason a systemically important market utility can move into production without abandoning its compliance and reconciliation obligations.

Institutional Process Diagram Showing A Traditional Security In A DTC Participant Account Moving Into DTC’s Digital Omnibus Account, Being Minted As A Token, Transferred Between Registered Wallets And Converted Back For Traditional Settlement. Mark Token Movements As 24/7 And Free-Of-Value.

Onchain Capital Formation Moves Closer

The same day as the DTCC milestone, Securitize and Cantor Fitzgerald announced an agreement to support blockchain-based initial public offerings and follow-on offerings.

Cantor will provide equity-capital-markets and trading capabilities, while Securitize will provide the regulated infrastructure used to issue, distribute and service the tokenized securities. The companies said the model would operate within the established framework for traditional public offerings.

This pushes tokenization into primary capital formation.

Most tokenized-stock products currently place a blockchain representation around securities that were already issued and trade in traditional markets. An onchain IPO would integrate the tokenized ownership record at the point when new capital is raised.

That is a more meaningful use of the technology than creating another mirrored trading product. It can potentially connect issuance, investor records, transfer restrictions and post-trade servicing within one operating system.

The agreement is not evidence that a tokenized IPO has already occurred. No issuer, offering size or launch date was disclosed in the announcement. The significance lies in regulated infrastructure being assembled before the first transaction.

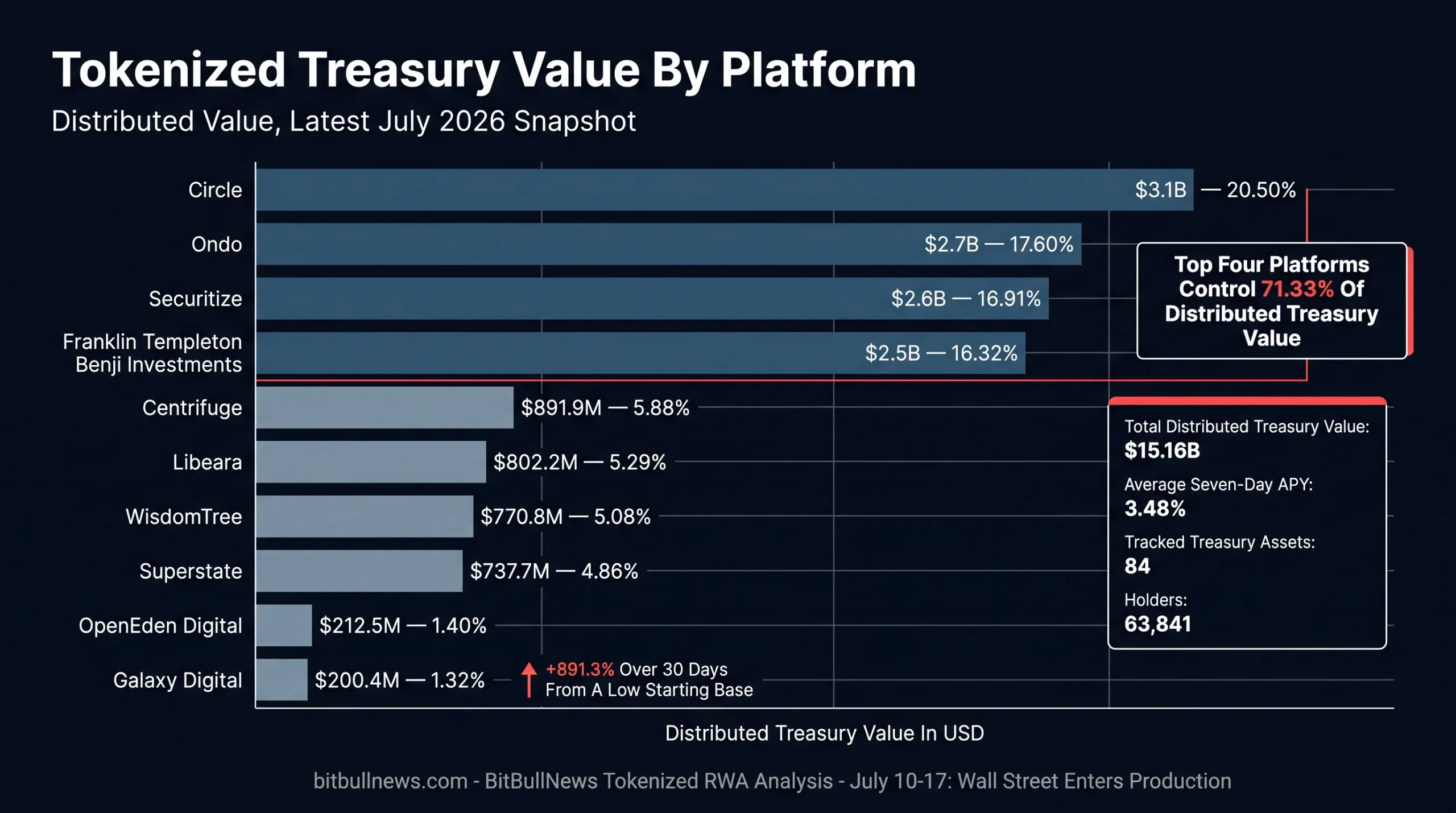

Treasuries Remain The Market’s Collateral Base

Tokenized U.S. Treasury products held approximately $15.16 billion in distributed value in the latest RWA.xyz snapshot. The category included 84 assets, 63,841 holders and an average seven-day yield of 3.48%.

Growth slowed to 1.25% over 30 days, but the category still accounted for almost half of the main distributed RWA classes in the scorecard.

The market remained highly concentrated.

| Treasury Platform | Distributed Value | 30-Day Change | Market Share |

|---|---|---|---|

| Circle | $3.1B | +3.22% | 20.50% |

| Ondo | $2.7B | -3.13% | 17.60% |

| Securitize | $2.6B | +1.78% | 16.91% |

| Franklin Templeton Benji Investments | $2.5B | -1.69% | 16.32% |

| Centrifuge | $891.9M | +0.53% | 5.88% |

| Libeara | $802.2M | -2.48% | 5.29% |

| WisdomTree | $770.8M | -12.69% | 5.08% |

| Superstate | $737.7M | +3.42% | 4.86% |

| OpenEden Digital | $212.5M | -2.44% | 1.40% |

| Galaxy Digital | $200.4M | +891.30% | 1.32% |

The four largest platforms controlled 71.33% of distributed Treasury value.

Circle’s USYC, BlackRock’s BUIDL, Ondo’s USDY and Franklin Templeton’s institutional and retail products remain the main blocks of onchain government-debt liquidity. The category is no longer controlled by a single issuer, but it is still far from evenly distributed.

Galaxy Digital produced the largest percentage increase among the top 10 platforms. Its value reached approximately $200.4 million after the State Street Galaxy Onchain Liquidity Sweep Fund expanded from a low starting base. SWEEP is designed to place short-duration Treasury exposure into a structure that can accept stablecoins and support continuous onchain cash management.

The rise of products such as SWEEP shows how the Treasury segment is changing. The first generation focused on putting Treasury yield inside a token. The newer generation is trying to make the token useful as cash-management inventory, stablecoin reserves or collateral.

Horizontal Bar Chart Showing The Top 10 Tokenized Treasury Platforms By Distributed Value. Highlight Circle, Ondo, Securitize And Franklin Templeton, With A Callout Showing Their Combined 71.33% Market Share.

Active Strategies Outpaced Passive Cash Products

Tokenized active strategies reached $1.77 billion, up 13.02% over 30 days. Holders increased 14.06% to 29,031, broadly matching the growth in asset value.

Spiko accounted for $992.9 million, or 56.15% of the category, after expanding 38.64%. OpenTrade ranked second with $181.7 million, while Securitize held $126.7 million.

The category includes actively managed credit, basis, hedge-fund and multi-asset strategies rather than passive exposure to a single pool of government securities.

Its growth points to a change in allocator behavior. Investors are beginning to use tokenized structures to access portfolio management and strategy execution, not only to hold blockchain-based cash equivalents.

The concentration risk is substantial. More than half of the category sits on one platform. AUM growth therefore says more about the success of a small number of products than about broad secondary-market depth.

Credit Expanded, But Platform Concentration Persisted

Distributed tokenized credit reached $7.03 billion, up 4.44% over 30 days. Represented credit was much larger at $35.63 billion, reflecting the sector’s reliance on controlled institutional structures and platform-based records.

Maple and STOKR each held close to $1.4 billion. Centrifuge followed with $746.3 million. Together, the three largest platforms controlled 51.98% of distributed credit value.

The faster-growing platforms were further down the ranking:

- Chainlink CCIP-linked credit value increased 55.07% to $365.9 million.

- OnRe expanded 19.33% to $224.9 million.

- Pareto grew 12.02% to $204.0 million.

- Maple declined 4.15% despite retaining the largest individual platform position.

This is healthier than growth concentrated entirely in the incumbent leaders. It suggests newer distribution, interoperability and insurance-linked structures are gaining capital.

Credit still requires a different risk framework from tokenized Treasuries. The token may settle quickly, but repayment depends on borrower quality, collateral, servicing, underwriting and enforcement rights outside the blockchain.

A faster token transfer does not improve the credit quality of the underlying loan.

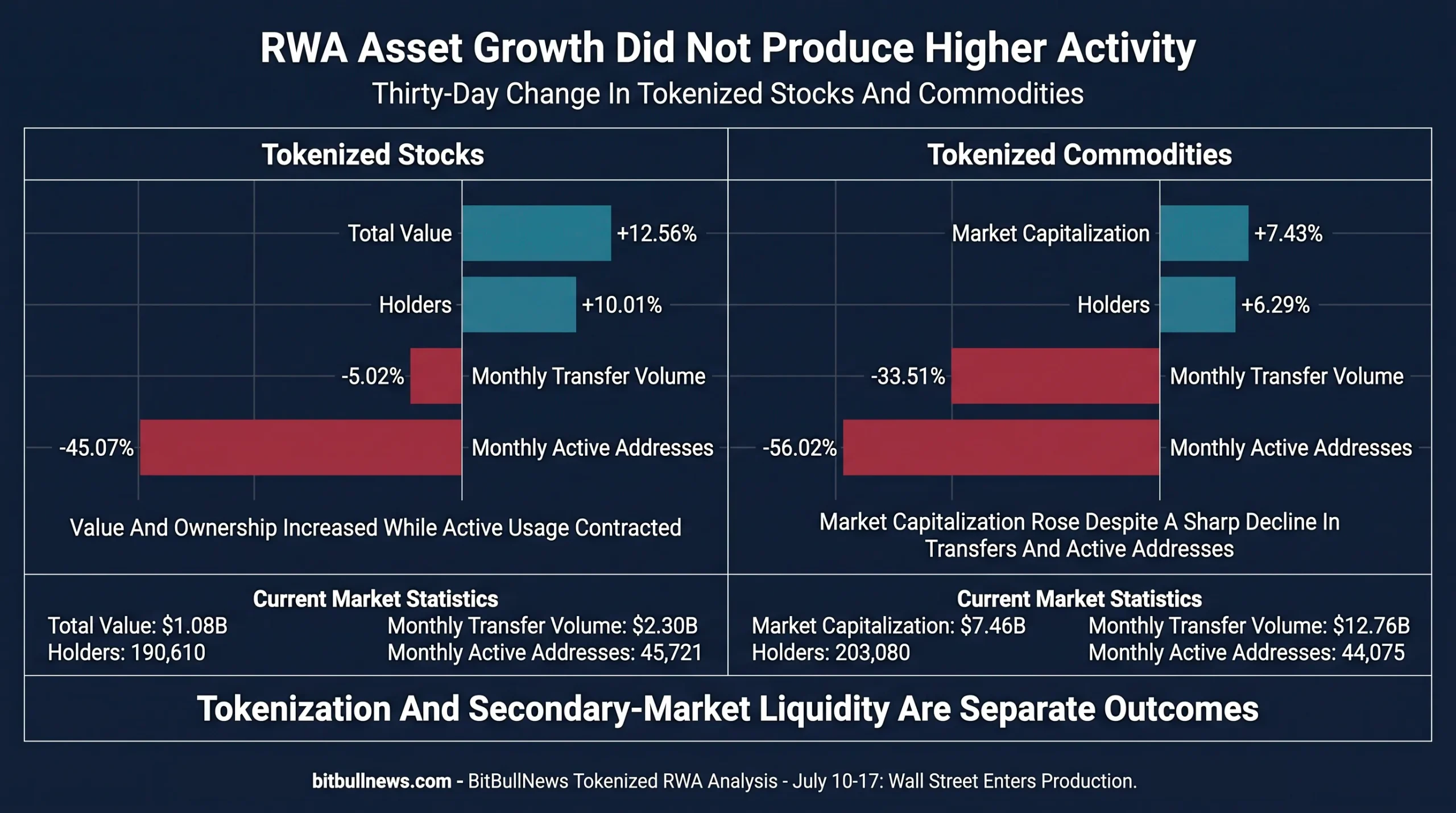

Tokenized Stocks Crossed $1 Billion

Tokenized stock value reached $1.08 billion, up 12.56% over 30 days. The number of holders increased 10.01% to approximately 190,610.

Ondo led the category with $644.0 million and a 60.49% market share. xStocks held $252.8 million, or 23.75%, while Securitize accounted for another $98.0 million. The three platforms controlled 93.45% of the market.

The concentration is only one part of the story.

Monthly transfer volume declined 5.02% to $2.30 billion, while monthly active addresses fell 45.07% to 45,721. Asset value and holder count increased, but usage contracted.

That divergence prevents a simple conclusion that tokenized equity liquidity improved alongside market capitalization.

Value can rise because of new issuance, investor inflows or changes in the price of the underlying shares. None of those guarantees that large positions can be traded onchain without meaningful slippage or that holder activity remains persistent.

The DTCC and Securitize–Cantor initiatives may eventually improve this structure by connecting tokenized equities to established capital-markets infrastructure. For now, the public-chain tokenized-stock market remains small, concentrated and unevenly active.

Commodity Value Rose While Activity Contracted

Tokenized commodity market capitalization increased 7.43% to $7.46 billion. Holders rose 6.29% to approximately 203,080.

Operational activity moved in the opposite direction:

| Commodity Metric | Current Reading | 30-Day Change |

|---|---|---|

| Market Capitalization | $7.46B | +7.43% |

| Holders | 203,080 | +6.29% |

| Monthly Transfer Volume | $12.76B | -33.51% |

| Monthly Active Addresses | 44,075 | -56.02% |

Tether accounted for 39.78% of tokenized commodity value, Paxos held 34.39% and Justoken controlled 24.61%. Together, the three managers represented almost the entire category.

The category is dominated by precious-metal products, particularly gold-backed tokens. Their market values can increase with the underlying commodity even when token-transfer activity declines.

That is why market capitalization cannot serve as a standalone liquidity measure. A token may be fully backed, correctly priced and legally structured while still lacking a broad or consistently active secondary market.

Two-Panel Divergence Chart Comparing Tokenized Stocks And Commodities. Panel One Shows Market Value And Holder Growth. Panel Two Shows Declining Transfer Volume And Active Addresses. Emphasize That Asset Growth Did Not Produce Higher Activity.

Tokenization Still Does Not Guarantee Liquidity

The week’s data reinforced a basic distinction: making an asset transferable is not the same as making it liquid.

Recent empirical research based on RWA.xyz and Ethereum data found substantial differences in turnover, holder breadth and active-address activity across tokenized Treasuries, gold and credit assets. Outstanding asset value alone did not reliably predict observed market liquidity.

State Street reached a similar institutional conclusion in its July research on tokenized money-market funds. The firm said secondary liquidity remains in development even as the use of tokenized funds as collateral is expected to increase with better settlement infrastructure.

This does not weaken the case for tokenization. It narrows the claim.

Tokenization can improve transferability, ownership records, subscription processing, settlement availability and collateral mobility. Liquidity still requires buyers, sellers, market makers, reliable pricing, redemption capacity and enough balance-sheet support to absorb large trades.

What Institutional Allocators Should Measure

Legal Rights Before Token Mechanics

Investors need to know whether a token represents direct ownership, a securities entitlement, a fund share, a debt obligation or synthetic price exposure.

Two tokens referencing the same stock can expose holders to entirely different legal and counterparty risks.

Distributed Value Before Headline RWA Value

Represented assets demonstrate institutional adoption of blockchain records. Distributed assets provide a better starting point for assessing external wallet movement and composability.

Neither measure should be presented as guaranteed secondary-market liquidity.

Transfer Volume And Active Addresses

AUM growth without higher transfer activity can indicate that assets are being issued or held rather than actively used.

For cash-management products, low turnover may be acceptable. For products marketed as continuously tradable securities, it deserves closer scrutiny.

Platform And Issuer Concentration

The top four Treasury platforms control 71.33% of their category. The top three tokenized-stock platforms control 93.45%. One platform represents more than half of active-strategy value.

Legal, operational or technical disruption at a leading provider can therefore affect a large part of the market.

Redemption And Conversion Mechanics

The ability to transfer a token does not guarantee immediate access to cash.

Investors should review redemption windows, settlement currencies, minimum sizes, fees, whitelisting requirements and whether the token must return to conventional form before use in established market infrastructure.

Collateral Eligibility

A tokenized asset becomes materially more useful when regulated lenders, exchanges and clearing systems accept it as collateral.

DTCC’s initial service does not grant its tokens collateral value for DTC risk-management purposes. That limitation will be one of the most important items to watch after the October launch.

| Signal | Current Reading | Interpretation | Confirmation Needed |

|---|---|---|---|

| Distributed RWA Value | $34.14B, +3.14% Over 30 Days | Transferable assets continue expanding | Higher transfer activity and secondary depth |

| Represented RWA Value | $376.93B, +6.81% | Institutions favor controlled ledger structures | Broader conversion into transferable formats |

| Treasury Growth | +1.25% | Core category remains large but slowed | Renewed net issuance across several platforms |

| Active Strategies | +13.02% | Demand broadening beyond passive yield | Lower platform concentration |

| Tokenized Stocks | Value +12.56%, Active Addresses -45.07% | Supply and ownership grew faster than activity | Recovery in transfers and active users |

| Commodities | Value +7.43%, Transfer Volume -33.51% | Market value rose without stronger usage | Sustained transfer and redemption activity |

| DTCC Tokenization | Limited-production milestone completed | Core U.S. infrastructure is moving onchain | October launch and real transaction volumes |

| DTC Settlement | Token movements are initially free-of-value | Asset mobility improves before cash settlement | Onchain payment and collateral integration |

| Onchain IPO Infrastructure | Cantor–Securitize agreement announced | Tokenization moving into primary issuance | First named issuer and completed offering |

Issuance Is Scaling. Usable Liquidity Is the Test

Tokenization crossed an important institutional threshold this week.

DTCC’s July 15 milestone brought public equities, ETFs and U.S. Treasuries into a structure connected directly to the existing U.S. securities depository. The tokens are designed to carry the same legal and economic rights as traditional holdings and move between registered wallets around the clock.

The first version is not a complete onchain market. Token movements remain free-of-value, cash settlement stays outside the token transfer and the assets initially receive no collateral value inside DTC’s settlement system. The infrastructure is entering production one layer at a time.

Public-chain RWA markets also continued to grow. Treasuries reached $15.16 billion, credit exceeded $7 billion, commodities stood at $7.46 billion and tokenized stocks moved above $1 billion. Active strategies delivered the strongest 30-day expansion.

The weak point was market quality. Stock and commodity values increased while active addresses and transfer volumes declined. Issuer and platform concentration also remained high across nearly every category.

The next phase will not be measured only by the value of assets placed onchain. It will be measured by how often those assets move, whether institutions accept them as collateral, whether redemptions remain reliable during stress and whether tokenized ownership can settle against tokenized cash without returning to legacy rails.

Issuance is scaling. Usable liquidity is still the test.

Data Sources & References

- RWA.xyz Network Analytics

- RWA.xyz Tokenized U.S. Treasuries

- RWA.xyz Tokenized Credit

- RWA.xyz Tokenized Stocks

- RWA.xyz Tokenized Commodities

- RWA.xyz Tokenized Active Strategies

- RWA.xyz Tokenized Real Estate

- RWA.xyz Distributed And Represented Asset Methodology

- DTCC Tokenization Service

- DTCC Tokenization Service FAQ

- DTCC July And October Tokenization Timeline

- SEC Statement On Tokenized Securities

- Securitize And Cantor Onchain Offerings Announcement

- State Street Research On Tokenized Money-Market Funds

- Tokenized But Illiquid? Evidence From RWA Markets