Content

Tokenized real-world assets had another strong data week on the surface. Underneath, the story was more complicated.

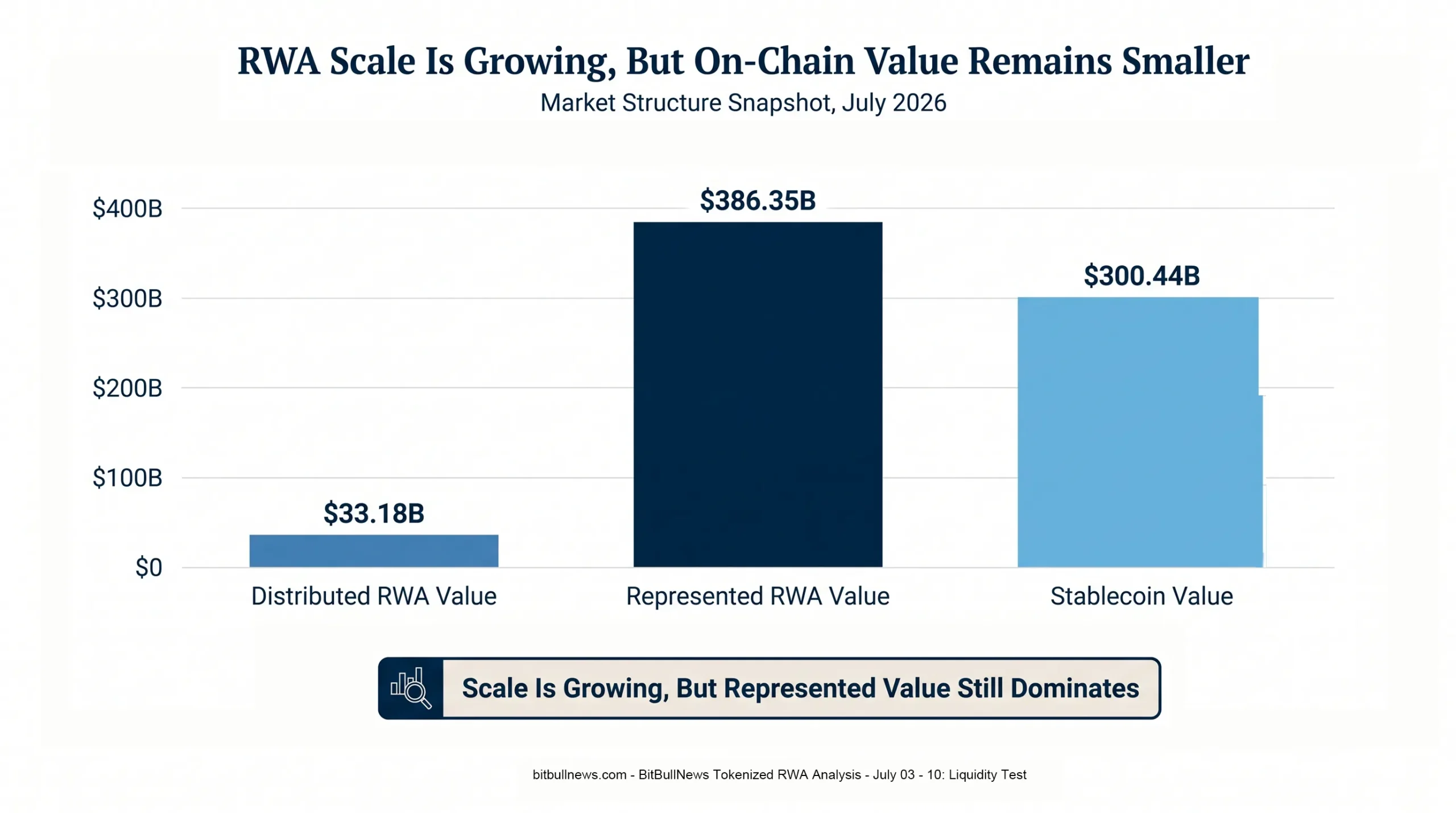

During the July 03 – July 10, 2026 reporting window, the RWA market continued to show scale across tokenized Treasuries, credit, commodities, funds, and tokenized securities. RWA.xyz’s current market snapshot showed $33.18 billion in distributed asset value, $386.35 billion in represented asset value, $300.44 billion in stablecoin value, and 966,378 RWA holders. Distributed value was up 2.50% over 30 days, while represented value was up 10.54% over the same period.

That headline looks bullish. It is. But it is not clean.

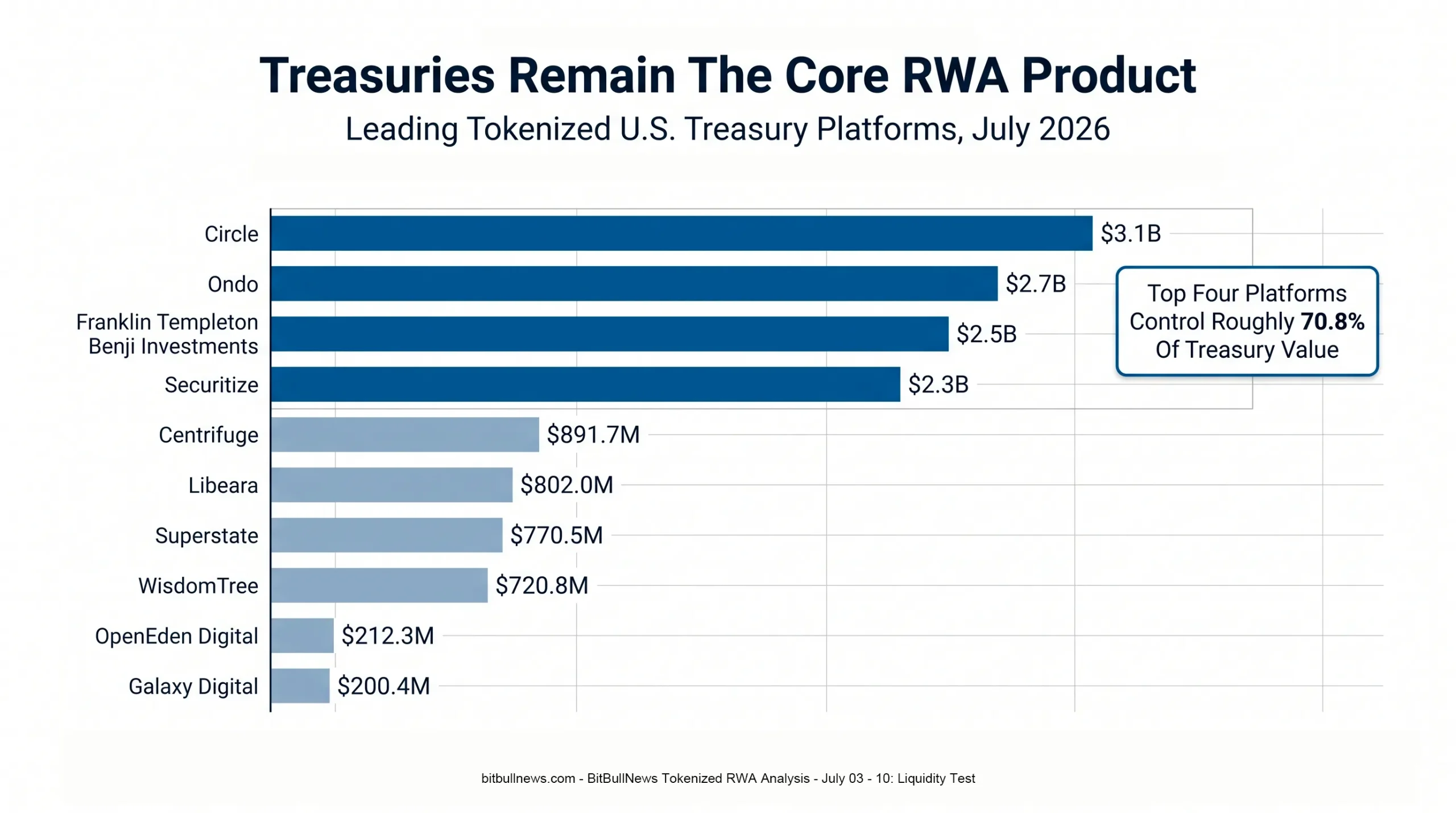

The market’s strongest live segment remains tokenized U.S. Treasuries and money-market-style products. RWA.xyz’s tokenized Treasury dashboard showed $14.89 billion in distributed Treasury value, 84 assets, 64,420 holders, and a 3.22% 7-day APY as of July 09, 2026. Circle, Ondo, Franklin Templeton Benji Investments, and Securitize controlled the top four platform slots by Treasury value.

Credit also expanded. RWA.xyz showed tokenized credit at $6.58 billion in distributed value and $24.66 billion in represented value as of July 10, 2026, with distributed credit up 7.56% over 30 days. The holder count, however, slipped 0.15% over the same period. That is the tension in one line: more value, not much broader participation.

The week’s most important signal came from liquidity, not market cap. A BeInCrypto Intelligence report built with RWA.xyz data found that roughly $60 billion in tokenized RWAs was spread across more than 7,000 products and 12 asset classes, but just 62 assets held 88% of total value, and 910 tokenized assets worth $32.9 billion showed zero weekly transfers.

Tokenization is working. Liquidity is not evenly following.

Chart: Grouped Bar Chart Comparing Distributed RWA Value, Represented RWA Value, And Stablecoin Value. Show $33.18B Distributed RWA Value, $386.35B Represented RWA Value, And $300.44B Stablecoin Value. Add A Callout: “Scale Is Growing, But Represented Value Still Dominates.”

Market Structure Snapshot

RWA is no longer one market. It is a stack of very different markets using similar language.

Distributed assets are closer to the crypto-native promise: investors can hold, transfer, and manage positions through wallets or custodians. Represented assets use blockchain more as a record layer around off-chain legal, custodial, or administrative systems. Stablecoins sit beside both because they are the cash and settlement layer for tokenized finance. RWA.xyz defines distributed assets as assets where blockchain acts as a distribution layer for on-chain investors.

| Segment | Latest Public Reading | 30D Change | Market Read |

|---|---|---|---|

| Distributed RWA Value | $33.18B | +2.50% | On-Chain RWA Value Still Expanding |

| Represented RWA Value | $386.35B | +10.54% | Off-Chain Reference Layer Is Much Larger |

| Stablecoin Value | $300.44B | +0.71% | Settlement Layer Remains Deep |

| Total RWA Holders | 966,378 | +6.88% | Adoption Broadened, But Still Concentrated |

| Total Stablecoin Holders | 272.08M | +2.96% | Stablecoins Remain The Mass-Market Base |

The gap between represented and distributed value is the market’s most important structural feature. Tokenized finance is not just “assets moving on-chain.” In many cases, it is traditional finance wrapping records, claims, and transfer workflows in blockchain-compatible form. That is useful, but it is not the same as deep, freely transferable secondary liquidity.

Treasuries Still Carry The Production-Grade RWA Case

Tokenized Treasuries remain the most mature RWA category because the product-market fit is obvious: institutional investors want short-duration dollar yield, crypto-native desks want collateral, and on-chain trading venues want cash-like instruments that can move faster than traditional money-market fund shares.

RWA.xyz showed $14.89 billion in distributed tokenized Treasury value as of July 09, down 0.77% over 30 days. The category had 84 assets, 64,420 holders, and a 3.22% 7-day APY.

| Treasury Platform | Total Value | 30D Change | Market Share | Read |

|---|---|---|---|---|

| Circle | $3.1B | +6.90% | 20.86% | Largest Treasury Platform By Value |

| Ondo | $2.7B | -3.23% | 17.92% | Strong Distribution, But Monthly Outflow |

| Franklin Templeton Benji Investments | $2.5B | -1.29% | 16.62% | TradFi Brand Still In Top Tier |

| Securitize | $2.3B | -9.35% | 15.40% | Major Infrastructure Platform, But Value Fell |

| Centrifuge | $891.7M | +0.53% | 5.99% | Smaller Positive Growth |

| Libeara | $802.0M | -3.67% | 5.38% | Moderate Monthly Contraction |

| Superstate | $770.5M | +6.65% | 5.17% | Positive Mid-Tier Growth |

| WisdomTree | $720.8M | -18.83% | 4.84% | Largest Top-10 Decline |

| OpenEden Digital | $212.3M | +25.93% | 1.43% | Fast Growth From Smaller Base |

| Galaxy Digital | $200.4M | +891.3% | 1.35% | Newer Entrant With Sharp 30D Jump |

The top four platforms controlled roughly 70.8% of the tokenized Treasury platform market in the July 09 snapshot. That concentration is not necessarily unhealthy. Treasury tokenization is still an institutional market, and institutional markets often consolidate around brand, custody, distribution, and compliance.

The more important detail is the split in monthly performance. Circle, Superstate, OpenEden, and Galaxy grew. Ondo, Franklin Templeton Benji Investments, Securitize, Libeara, and WisdomTree declined. That tells us the category is not moving as one block. Distribution channels, collateral integrations, investor eligibility, and redemption design are starting to matter more than the simple label “tokenized Treasury.”

Chart: Horizontal Bar Chart Showing Tokenized Treasury Platform Market Share By Total Value. Use Circle $3.1B, Ondo $2.7B, Franklin Templeton Benji Investments $2.5B, Securitize $2.3B, Centrifuge $891.7M, Libeara $802.0M, Superstate $770.5M, WisdomTree $720.8M, OpenEden Digital $212.3M, And Galaxy Digital $200.4M. Highlight The Top Four Platforms.

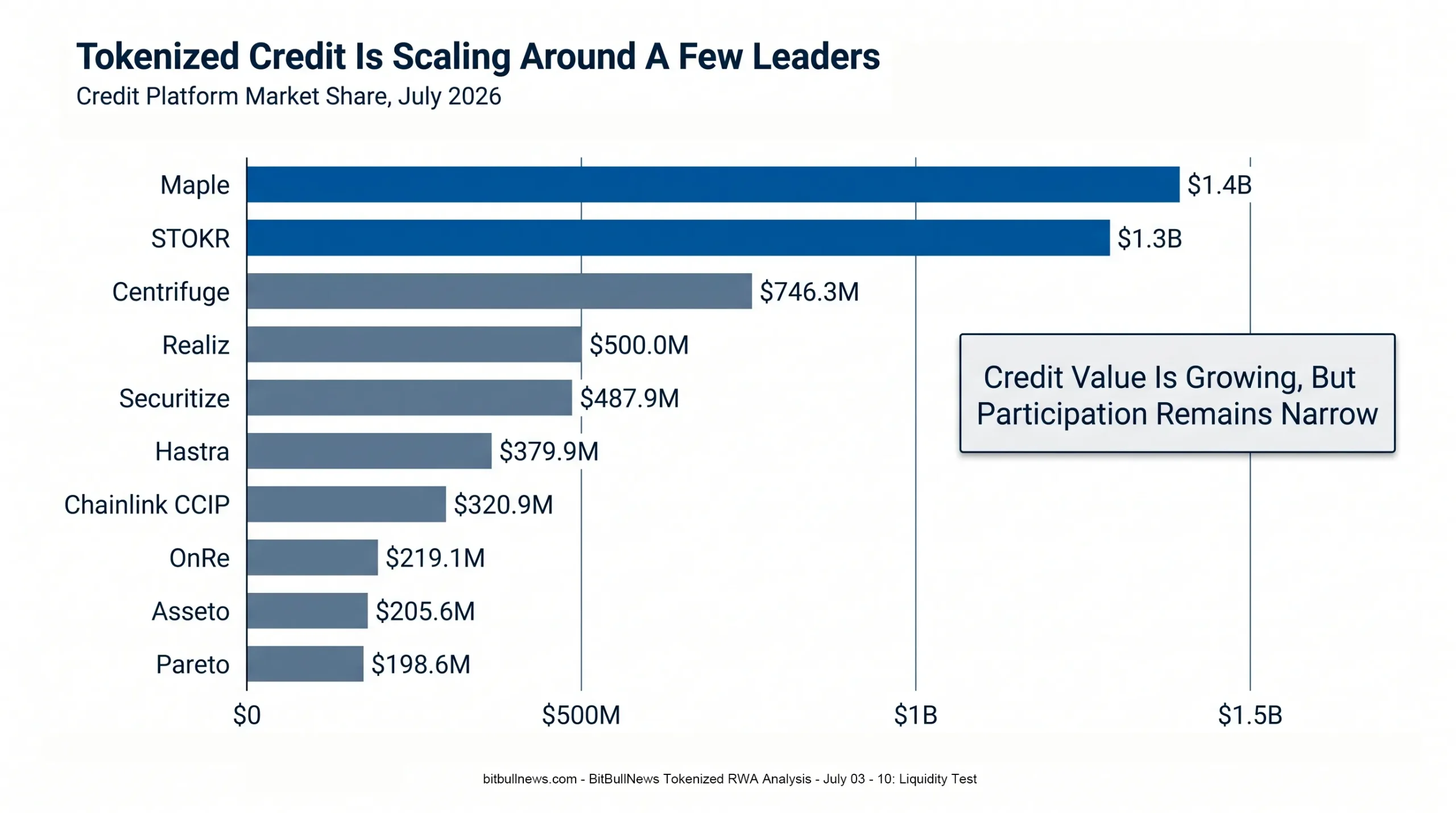

Credit Is Growing, But Participation Is Narrow

Tokenized credit had a strong value week.

RWA.xyz showed tokenized credit at $6.58 billion in distributed value, up 7.56% over 30 days, and $24.66 billion in represented value, up 4.72%. The asset count reached 2,506, while holders stood at 184,993, down 0.15% over 30 days.

Credit is a different animal from Treasuries. The underlying assets are less uniform. Asset-backed credit, private credit, corporate credit, specialty finance, reinsurance, and structured products all sit inside the category. That makes headline growth harder to interpret.

Maple and STOKR still dominate the platform table, but Securitize’s 106.4% 30-day growth and Chainlink CCIP’s 34.16% gain show that infrastructure-linked credit products can expand quickly from smaller bases.

The asset table shows the same divide. Figure HELOC Token represented $19.74 billion in value, while Syrup USDC carried $1.39 billion in distributed value with 7,980 holders. Blockstream Mining Note 2 stood at $697.3 million, PKH Mining Note 2 at $577.5 million, and VuMe Bond 2030 at $500.0 million.

That is not a retail credit market. It is an institutional and semi-institutional structured-finance market using blockchain rails.

Chart: Horizontal Bar Chart Showing Tokenized Credit Platform Market Share. Use Maple $1.4B, STOKR $1.3B, Centrifuge $746.3M, Realiz $500.0M, Securitize $487.9M, Hastra $379.9M, Chainlink CCIP $320.9M, OnRe $219.1M, Asseto $205.6M, Pareto $198.6M. Highlight Maple And STOKR As The Top Two.

The Liquidity Gap Is The Real Story

Tokenized RWAs are growing. Many of them still do not trade.

The BeInCrypto Intelligence report built with RWA.xyz data found that 910 assets worth $32.9 billion had zero weekly transfers among 1,289 tokenized assets valued above $100,000. The same report found that 62 assets accounted for about 88% of total value, while five products made up roughly half of the market.

| Liquidity Metric | Reading | Why It Matters |

|---|---|---|

| Tokenized RWA Market Tracked In Report | ~$60B | Shows The Sector Has Reached Real Scale |

| Products Tracked | 7,000+ | Product Count Is Broad, But Value Is Concentrated |

| Asset Classes | 12 | RWA Is No Longer Just Treasuries |

| Assets Holding 88% Of Value | 62 | Market Cap Is Highly Concentrated |

| Assets With Zero Weekly Transfers | 910 | Tokenization Does Not Guarantee Trading Activity |

| Value Of Zero-Transfer Assets | $32.9B | A Large Share Of Value Is Static |

| Market Outside U.S. Retail Reach | 97% | Access Remains Heavily Restricted |

| Stock Tokens With Synthetic Exposure | 59% | Equity Tokenization Still Has Ownership-Quality Issues |

This is the key distinction: tokenization improves recordkeeping, transfer design, settlement workflow, transparency, and collateral mobility. It does not automatically create buyers, sellers, market makers, credit analysis, price discovery, or regulatory access.

Academic work is starting to reach the same conclusion. One 2026 paper using RWA.xyz and Etherscan data found that on-chain representation and secondary-market liquidity are separate outcomes, and that asset value alone does not reliably predict observed liquidity. Another 2026 paper argued that TVL can hide liquidity, concentration, and market-quality risk, especially when tokens have low turnover, limited active-address activity, and concentrated ownership.

For investors, this is where the RWA market stops being a headline-growth story and becomes a due-diligence problem.

Infrastructure Is Moving Faster Than Secondary Markets

Traditional market infrastructure is now moving into tokenization in a more concrete way.

DTCC said it plans to facilitate initial limited production trades of real-world assets tokenized through DTC’s tokenization service in July 2026, with a broader launch planned for October 2026. More than 50 firms joined the DTCC working group, including BlackRock, Goldman Sachs, J.P. Morgan, Morgan Stanley, Nasdaq, NYSE Group, Robinhood, State Street, UBS, Wells Fargo, Circle, Ondo Finance, Ripple Prime, and Kraken parent Payward. DTCC also said the service is designed for DTC-custodied assets that keep the same entitlements, investor protections, and ownership rights as traditional-form assets.

That matters because it points to the likely path of institutional tokenization. The winner may not be the most crypto-native token. It may be the structure that connects tokenized records to existing custody, settlement, entitlement, and compliance systems.

Securitize provided the week’s equity-tokenization case study. The company began trading on the NYSE under ticker SECZ on July 2, 2026, and made tokenized versions of its own shares available to eligible U.S. investors on Avalanche and Solana through its regulated platform. TheStreet reported that SECZ was issuer-sponsored and represented the same common stock trading on the NYSE, not a synthetic wrapper.

The timing was important. Securitize did not tokenize a concept-stage product. It tokenized its own public equity on listing day.

Regulatory Risk: Tokenized Securities Are Still Securities

The legal question is not whether blockchain can represent a security. It can. The question is what rights the token actually gives the holder.

The SEC’s January 2026 staff statement described issuer-sponsored tokenized securities and third-party-sponsored tokenized securities. It also warned that third-party tokenized products may expose holders to risks tied to the third party, including bankruptcy risk that would not necessarily apply to direct holders of the underlying security.

Commissioner Hester Peirce made the cleaner point in 2025: tokenized securities are still securities, and market participants must comply with federal securities laws when transacting in them. She also warned that tokenized instruments can differ materially depending on whether they represent direct ownership, a security entitlement, a receipt, or a security-based swap.

That is why the SECZ example matters. Issuer-sponsored tokenization is structurally different from offshore synthetic stock tokens. One points toward regulated ownership infrastructure. The other may only provide price exposure.

The market will need to separate these models clearly, because investors will.

What The Market Actually Means This Week

RWA tokenization is not slowing down. It is becoming more selective.

Treasuries are still the cleanest product-market fit because they offer dollar yield, short duration, transparent underlying markets, and collateral utility. Credit is growing, but the category carries more structural complexity. Represented assets are massive, but not always equivalent to liquid on-chain instruments. Tokenized equities are moving forward, but legal structure matters more than ticker availability.

This week’s market signal is not “RWA is booming.” That is too simple.

The better read is this:

- Treasuries are production-grade.

- Credit is scaling, but still narrow.

- Liquidity is uneven.

- Infrastructure is catching up.

- Regulatory structure is becoming the main quality filter.

That last point is the one investors should not miss. The difference between a regulated tokenized fund share, a permissioned credit token, a represented off-chain loan, and a synthetic equity token is not cosmetic. It changes redemption rights, transferability, counterparty exposure, investor eligibility, and legal enforceability.

| Audience | Signal To Watch | Why It Matters |

|---|---|---|

| Investors | Transfers, Holders, And Redemption Terms | Market Cap Alone Does Not Prove Liquidity |

| Issuers | Distribution And Integrations | Tokenized Assets Need Venues, Collateral Use, And Market Makers |

| DeFi Protocols | Treasury And Credit Collateral Quality | RWA Collateral Adds Yield, But Also Legal And Redemption Risk |

| Asset Managers | Investor Eligibility Rules | Restricted Products Can Scale Without Becoming Retail Markets |

| Policymakers | Third-Party Tokenized Securities | Synthetic Or Custodial Wrappers Can Create New Counterparty Risks |

| Market Infrastructure Firms | DTCC And Issuer-Sponsored Models | Institutional Adoption May Flow Through Existing Settlement Rails |

For investors, the question is no longer “Is this asset tokenized?” The question is: can it be sold, redeemed, financed, transferred, priced, and legally enforced?

For issuers, tokenization is no longer enough. The product needs distribution, custody confidence, compliance clarity, secondary-market design, and transparent reporting.

For policymakers, the challenge is not blocking tokenization. It is making sure tokenized claims are understandable, enforceable, and not mislabeled as ownership when they are only exposure.

Key Findings

- RWA.xyz showed $33.18 billion in distributed RWA value and $386.35 billion in represented value, with distributed value up 2.50% over 30 days.

- Tokenized U.S. Treasuries stood at $14.89 billion in distributed value, with 84 assets, 64,420 holders, and a 3.22% 7-day APY as of July 09, 2026.

- Circle, Ondo, Franklin Templeton Benji Investments, and Securitize controlled the top four tokenized Treasury platform slots by value.

- Tokenized credit reached $6.58 billion in distributed value and $24.66 billion in represented value as of July 10, 2026.

- Maple and STOKR led tokenized credit platform value with $1.4 billion and $1.3 billion, respectively.

- A BeInCrypto Intelligence report using RWA.xyz data found that 910 assets worth $32.9 billion had zero weekly transfers, and 62 assets held 88% of total tokenized RWA value.

- DTCC plans limited production trades of tokenized DTC-custodied assets in July 2026, followed by a planned service launch in October 2026.

- Securitize listed on the NYSE under SECZ on July 2, 2026, and tokenized its own common stock on Avalanche and Solana for eligible U.S. investors.

- The SEC has warned that tokenized securities can carry different legal and counterparty risks depending on structure, especially when third parties tokenize securities they do not issue.

What To Watch Next

The first watch item is Treasury concentration. If Circle, Ondo, Franklin Templeton, and Securitize keep controlling the category, the market will look more like institutional money markets than open DeFi.

The second watch item is credit holder growth. Tokenized credit value is rising, but RWA.xyz showed holders slightly down over 30 days. That divergence cannot persist forever if the category wants durable liquidity.

The third watch item is transfer activity. Zero-transfer assets are the market’s biggest warning label. A token that never moves may still be useful as an administrative record, but it is not a liquid market instrument.

The fourth watch item is issuer-sponsored equity tokenization. Securitize’s SECZ launch gives the market a cleaner benchmark than synthetic stock tokens. If more public companies or funds follow that model, tokenized securities could shift from offshore wrappers toward regulated ownership infrastructure.

The fifth watch item is DTCC’s July production phase. If DTC-custodied tokenized assets begin moving through institutional workflows with the same rights and protections as traditional-form assets, tokenization will move closer to core market infrastructure.

BitBullNews View

Tokenized RWA is past the proof-of-concept stage. It is not yet past the liquidity test.

Treasuries have found a real use case: yield-bearing dollar collateral for always-on markets. Credit is expanding, but it needs broader participation and better transfer activity. Tokenized equities are entering a more serious phase, but investors need to know whether they hold real ownership, an entitlement, or synthetic exposure.

The market’s next phase will not be won by the loudest tokenization announcement. It will be won by products that can answer five questions cleanly:

- What is the legal claim?

- Who holds the underlying asset?

- Who can redeem?

- Where can the token trade or transfer?

- What happens if the issuer, custodian, or wrapper fails?

That is where tokenization becomes finance rather than packaging.

Data Sources & References

- RWA.xyz — Tokenized Real-World Asset Analytics

- RWA.xyz — Tokenized U.S. Treasuries Dashboard

- RWA.xyz — Tokenized Credit Dashboard

- RWA.xyz — Networks Dashboard

- BeInCrypto — The Real State Of Tokenization: Experts React To The RWA Market’s Liquidity Problem

- FinanceFeeds — 56% Of Tokenized RWAs Show No Weekly On-Chain Activity

- SEC — Statement On Tokenized Securities

- SEC — Enchanting, But Not Magical: A Statement On The Tokenization Of Securities

- DTCC — DTCC Advances DTC Tokenization Service; 50+ Firms Join

- TheStreet — Securitize Brings Its Own Stock Onchain On Solana At NYSE Debut

- ArXiv — Tokenized But Illiquid? Evidence From Real-World Asset Markets

- ArXiv — Beyond TVL: An Explainable Risk Scoring Framework For Tokenized Real-World Assets