Content

Tokenized real-world assets are no longer a conference theme. They are now a measurable market with large funds, public-company experiments, regulated transfer agents, and live institutional infrastructure.

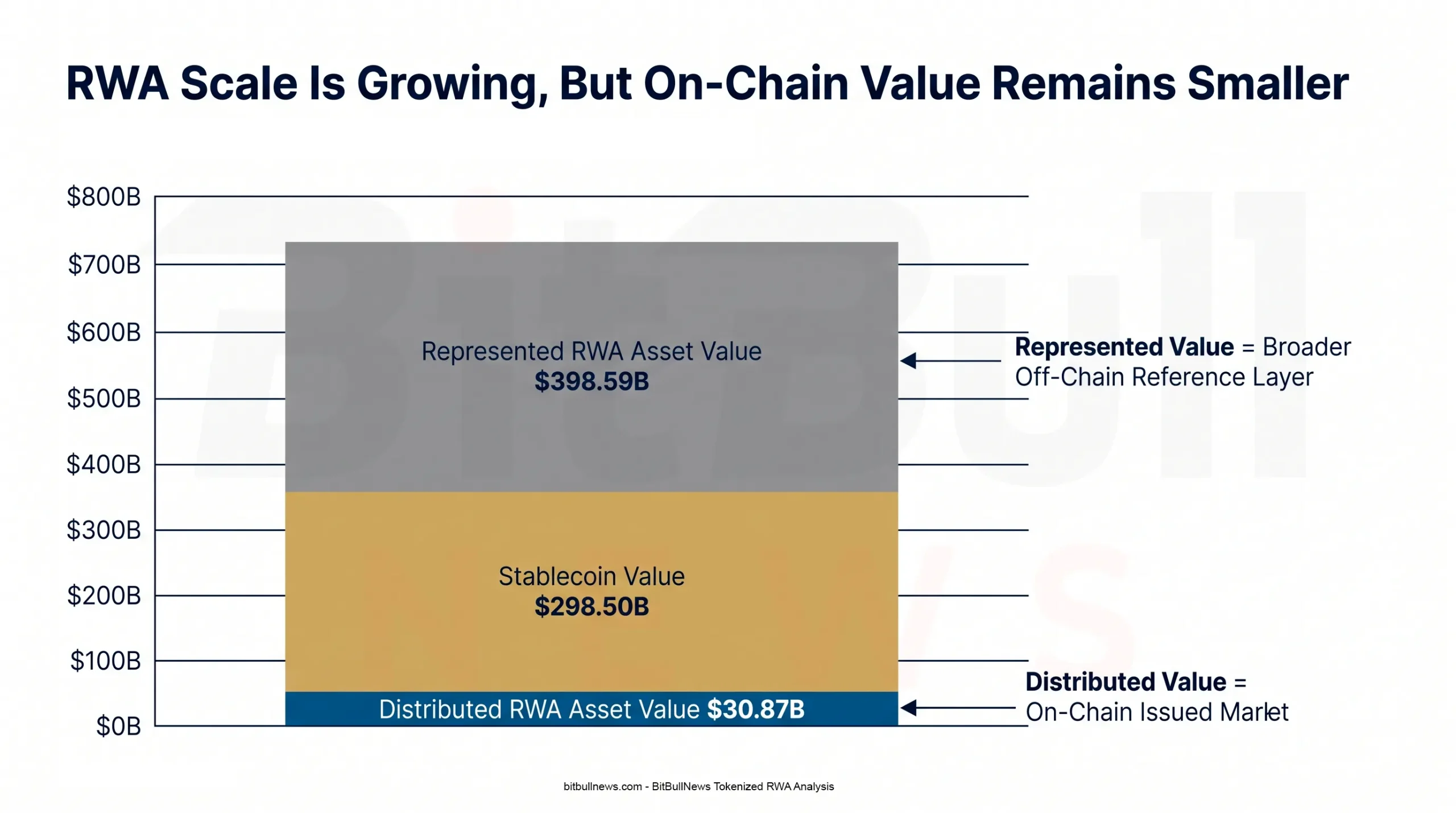

As of the latest RWA.xyz market snapshot available around July 4, 2026, tokenized RWAs showed $30.87 billion in distributed asset value, down 3.92% over 30 days, while represented asset value stood at $398.59 billion, up 3.72% over 30 days. The same dashboard showed 889,409 total asset holders, up 15.40% over 30 days. Stablecoins remain much larger at $298.50 billion, but they should be read separately from securities, credit, Treasuries, commodities, funds, and real-estate tokens.

The headline is not “RWAs are exploding.” The better read is sharper: tokenization is scaling, but the market is splitting between production-grade instruments and static wrappers.

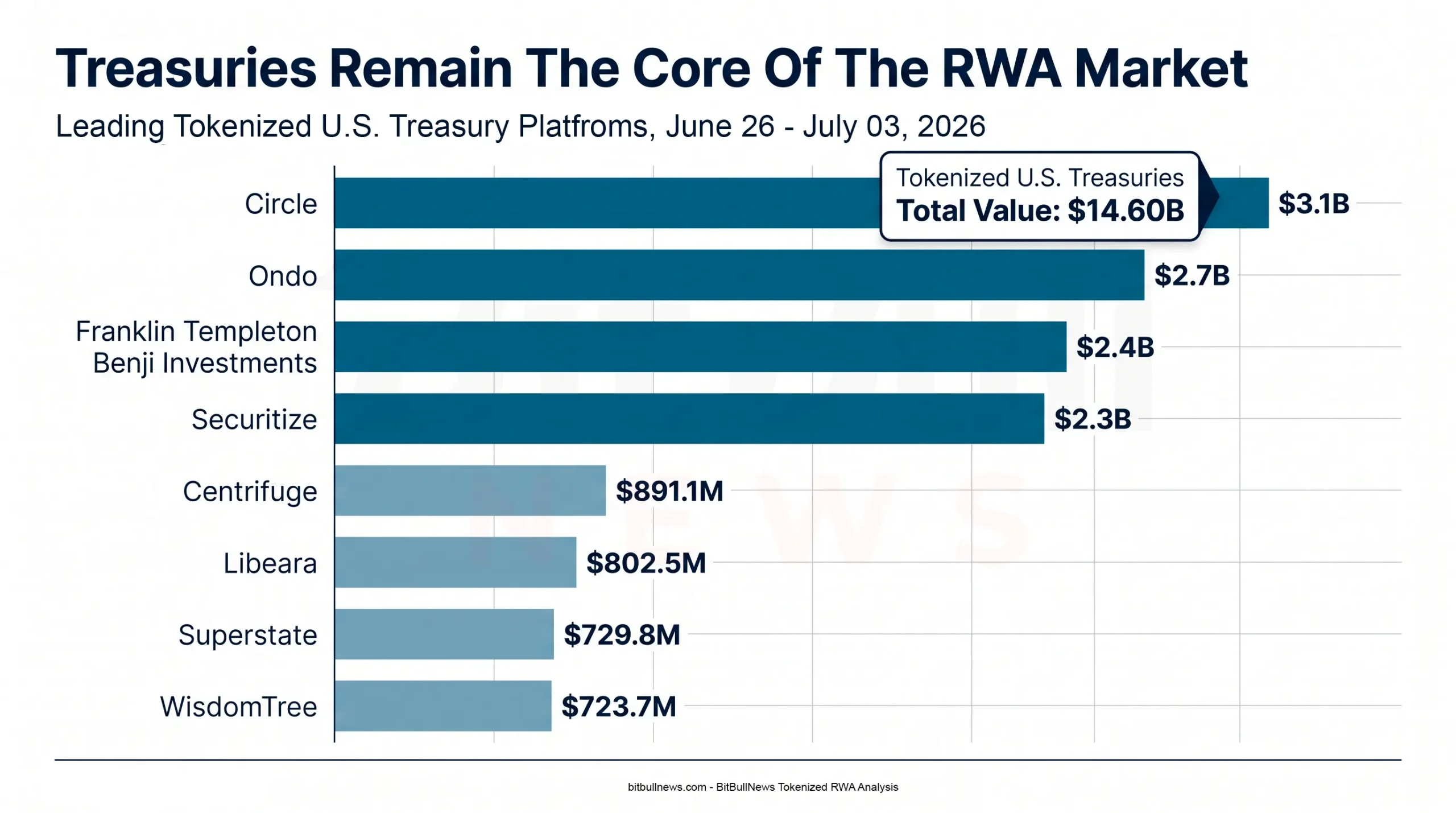

U.S. Treasuries are still the cleanest product-market fit. RWA.xyz showed $14.60 billion in tokenized U.S. Treasury value, with Circle, Ondo, Franklin Templeton Benji Investments, and Securitize leading the platform table. Tokenized credit is smaller but active, with $5.91 billion in distributed value and $23.97 billion in represented value.

The weak point is liquidity. A July 2026 report citing BeInCrypto Research and RWA.xyz found that 56% of tokenized RWA market value showed no weekly on-chain transfer activity, and that 62 assets accounted for about 88% of total tokenized RWA value. That is the core tension in this market: tokenized value is growing faster than active secondary-market depth.

Chart: Stacked Bar Chart Comparing Distributed RWA Value, Represented RWA Value, And Stablecoin Value. Use $30.87B Distributed RWA, $398.59B Represented RWA, And $298.50B Stablecoins. Add A Callout: “Distributed Value Is The On-Chain Market; Represented Value Is The Broader Asset Reference Layer.”

Market Structure Snapshot

| Metric | Latest Reading | 30D Change | Market Read |

|---|---|---|---|

| Distributed RWA Asset Value | $30.87B | -3.92% | On-Chain RWA Value Contracted |

| Represented RWA Asset Value | $398.59B | +3.72% | Off-Chain Reference Layer Expanded |

| Total RWA Asset Holders | 889,409 | +15.40% | Holder Base Grew Despite Value Decline |

| Total Stablecoin Value | $298.50B | -2.14% | Stablecoins Still Dwarf Non-Stablecoin RWAs |

| Stablecoin Holders | 263.08M | +5.24% | Payment-Dollar Adoption Remains Far Broader |

The market is giving two different signals at once. Value contracted on-chain, but holders grew. That means distribution is widening even as headline RWA value pulled back. For issuers, that is not a bad setup. More holders create a base for future activity. For investors, it is not enough. Holder growth without transfer activity can still leave a product difficult to exit.

The gap between distributed and represented value also matters. Distributed value reflects assets actually issued and tracked as on-chain instruments. Represented value captures a much broader claim or reference layer. That spread is useful, but it can mislead readers who treat every represented dollar as liquid on-chain collateral.

Treasuries Still Carry The RWA Market

Tokenized U.S. Treasuries remain the most mature RWA category because they solve a real market problem: institutions and crypto-native treasuries want short-duration dollar yield that can move on blockchain rails.

RWA.xyz showed $14.60 billion in tokenized Treasury value, down 2.00% over 30 days, with 84 assets and 63,994 holders. The same dashboard showed a 7-day APY of 3.26%. The top platform table was led by Circle at $3.1 billion, Ondo at $2.7 billion, Franklin Templeton Benji Investments at $2.4 billion, and Securitize at $2.3 billion.

| Tokenized Treasury Platform | Total Value | 30D Change | Market Share | Read |

|---|---|---|---|---|

| Circle | $3.1B | +5.07% | 21.27% | Largest Treasury Platform In The Dataset |

| Ondo | $2.7B | -2.86% | 18.33% | Major On-Chain Treasury Issuer |

| Franklin Templeton Benji Investments | $2.4B | -2.00% | 16.67% | Regulated Fund Structure With Broad Recognition |

| Securitize | $2.3B | -7.31% | 15.71% | Institutional Tokenization Infrastructure |

| Centrifuge | $891.1M | +0.57% | 6.10% | Smaller But Still Material |

| Libeara | $802.5M | -3.59% | 5.49% | Institutional Platform Exposure |

| Superstate | $729.8M | -2.83% | 5.00% | Treasury Product With Specialist Positioning |

| WisdomTree | $723.7M | -19.71% | 4.95% | Largest 30D Decline Among Top Platforms |

The Treasury segment is not just bigger than other non-stablecoin RWA categories. It is easier to underwrite. The underlying asset is liquid, the yield is simple to explain, pricing is transparent, and redemption logic is clearer than in private credit, real estate, or tokenized equity wrappers.

That is why Treasury RWAs have moved from demonstration to usage. They can act as collateral, treasury-management instruments, yield-bearing cash substitutes, and settlement assets. The rest of the RWA market still has to prove that tokenization improves more than the database layer.

Chart: Horizontal Bar Chart Showing Tokenized Treasury Platform Market Share. Highlight Circle, Ondo, Franklin Templeton Benji Investments, And Securitize As The Four Largest Platforms.

Credit Is Growing, But The Risk Profile Is Different

Tokenized credit is the second major RWA vertical, but it should not be analyzed like Treasuries.

RWA.xyz showed tokenized credit at $5.91 billion distributed value, up 10.42% over 30 days, and $23.97 billion represented value, up 4.22% over 30 days. The platform table was led by Maple at $1.4 billion, STOKR at $1.3 billion, Centrifuge at $744.6 million, and Securitize at $487.6 million.

| Tokenized Credit Platform | Total Value | 30D Change | Market Share | Read |

|---|---|---|---|---|

| Maple | $1.4B | -3.29% | 24.37% | Largest Distributed Credit Platform |

| STOKR | $1.3B | -1.62% | 21.64% | Large Specialty-Finance Exposure |

| Centrifuge | $744.6M | +49.59% | 12.61% | Strongest Growth Among Top Four |

| Securitize | $487.6M | +106.4% | 8.26% | Fast-Growing Institutional Credit Channel |

| Hastra | $395.2M | -0.24% | 6.69% | Mid-Sized Credit Platform |

| Chainlink CCIP | $232.8M | -12.48% | 3.94% | Interoperability-Linked Exposure |

| OnRe | $211.7M | +13.61% | 3.59% | Smaller But Growing |

| Asseto | $205.7M | -2.23% | 3.48% | Stable Mid-Tier Platform |

Credit growth looks healthy on the surface. The problem is that credit RWAs carry underwriting, borrower, maturity, collateral, legal, and servicing risk. A tokenized loan or credit pool can be easier to transfer, but that does not make the borrower safer or the secondary bid deeper.

The category also has a large represented-value component. RWA.xyz lists Figure HELOC Token at $19.53 billion represented value, far above most distributed credit assets. That is an important signal: the credit market contains large off-chain reference pools, but not all of that value behaves like liquid on-chain inventory.

Networks: Ethereum Still Dominates, But Solana And Stellar Are Moving

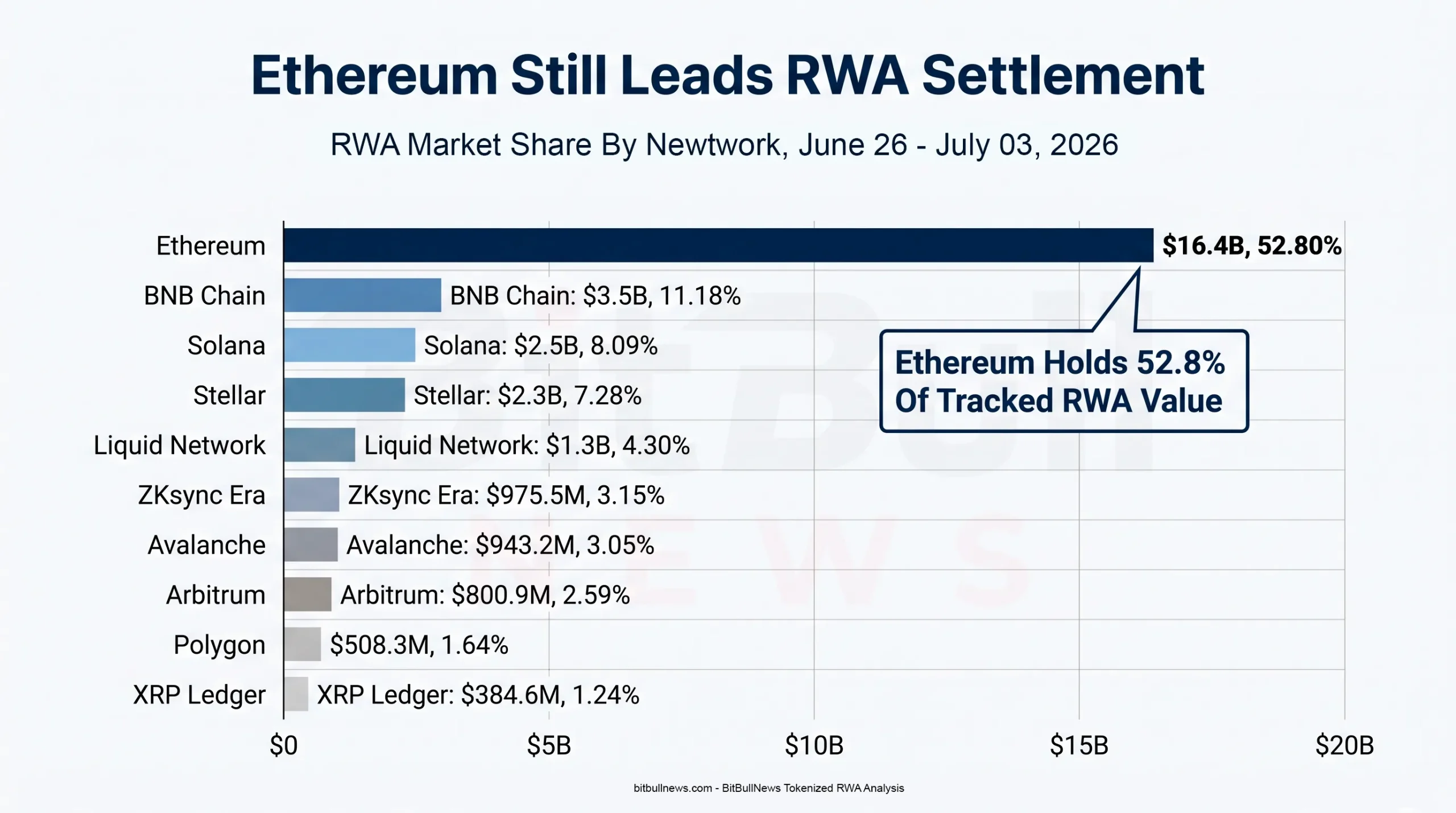

Ethereum remains the main RWA settlement venue. RWA.xyz showed Ethereum with 707 RWA assets, $16.4 billion in total value, and 52.80% market share, despite a 5.46% 30-day decline. BNB Chain ranked second at $3.5 billion, while Solana and Stellar showed stronger positive momentum at $2.5 billion and $2.3 billion, respectively.

| Network | RWA Count | Total Value | 30D Change | Market Share |

|---|---|---|---|---|

| Ethereum | 707 | $16.4B | -5.46% | 52.80% |

| BNB Chain | 479 | $3.5B | -13.31% | 11.18% |

| Solana | 420 | $2.5B | +7.34% | 8.09% |

| Stellar | 43 | $2.3B | +36.02% | 7.28% |

| Liquid Network | 8 | $1.3B | -9.97% | 4.30% |

| ZKsync Era | 1 | $975.5M | +1.22% | 3.15% |

| Avalanche | 60 | $943.2M | +13.44% | 3.05% |

| Arbitrum | 278 | $800.9M | -6.50% | 2.59% |

| Polygon | 139 | $508.3M | -13.65% | 1.64% |

| XRP Ledger | 19 | $384.6M | -11.31% | 1.24% |

This is not a simple Ethereum-only story anymore. Ethereum still owns the institutional center of gravity, but Solana, Stellar, and Avalanche posted positive 30-day growth while several other networks contracted. That suggests issuers are testing distribution and settlement rails beyond Ethereum, especially where speed, cost, institutional relationships, or specialized asset support matter.

Still, Ethereum’s share is too large to ignore. If an institutional desk asks where RWA liquidity actually sits, the answer is still Ethereum first. The other chains are growth signals, not full replacements.

Chart: Network Market Share Bar Chart Showing Ethereum, BNB Chain, Solana, Stellar, Liquid Network, ZKsync Era, Avalanche, Arbitrum, Polygon, And XRP Ledger. Add A Callout: “Ethereum Holds 52.8% Of Tracked RWA Value.”

Product-Level Concentration Is The Real Risk

RWA concentration is not just a chain issue. It is a product issue.

The latest market reporting based on BeInCrypto Research and RWA.xyz found that 62 assets accounted for about 88% of total tokenized RWA value, while five products represented roughly half of the market. That makes the market more fragile than aggregate growth suggests. A few large products can make the entire sector look deep, even if most assets have thin transfer activity or limited holder bases.

RWA.xyz’s visible asset list reinforces the same picture. In Treasuries, products such as iBENJI, WTGXX, JTRSY, BENJI, USTB, and OUSG dominate the visible high-value end of the table. In commodities, XAUT and PAXG carry most of the visible market value, with XAUT at $2.6 billion and PAXG at $2.0 billion.

| Segment | Large Visible Assets Or Platforms | What The Concentration Means |

|---|---|---|

| U.S. Treasuries | Circle, Ondo, Franklin Templeton Benji, Securitize | A Few Platforms Define Treasury RWA Liquidity |

| Credit | Maple, STOKR, Centrifuge, Securitize | Credit Value Is Platform-Heavy And Underwriting-Sensitive |

| Commodities | XAUT, PAXG | Gold-Backed Tokens Remain The Main Commodity Use Case |

| Networks | Ethereum, BNB Chain, Solana, Stellar | Chain Distribution Is Improving, But Ethereum Still Dominates |

| Tokenized Stocks | SECZ, CRCLon, CRCLx, NVDAon, TSLAx, SPYon | Equities Are Emerging, But Legal Rights And Trading Access Vary |

The practical investor question is no longer “Is this asset tokenized?” It is “Who can hold it, who can redeem it, who makes markets in it, what rights does the token carry, and what happens if the issuer, custodian, transfer agent, or wrapper fails?”

Tokenized Equities Are Moving From Wrapper To Market Infrastructure

The equity side of RWA tokenization became more important this week.

Securitize began trading on the NYSE on July 2, 2026 under the ticker SECZ, and made tokenized versions of its shares available to eligible U.S. investors through its regulated platform on Avalanche and Solana. Reports described it as the first newly public company to tokenize its own stock on day one of trading.

That matters because it is different from many offshore tokenized-stock models. A synthetic or third-party wrapper can track a stock price without giving the holder the same legal relationship as a registered shareholder. An issuer-sponsored tokenization model is a more serious test of whether public equities can move on-chain without breaking securities-law plumbing.

DTCC is also moving from concept to controlled implementation. DTCC said in May that more than 50 firms had joined development of its tokenization service, with initial limited production trades planned for July 2026 and a broader launch planned for October 2026. DTCC’s tokenization page says the service is designed to let DTC participants and clients convert supported assets between traditional book-entry and digital tokenized forms while maintaining investor protections and ownership rights.

This is the institutional direction: not “stocks on random chains,” but tokenized entitlements, regulated transfer agents, custody integration, issuer sponsorship, and exchange/DTC compatibility.

The SEC Message: Tokenized Securities Are Still Securities

The U.S. policy signal is not ambiguous. SEC staff stated in January 2026 that it had observed two models where a third party tokenizes securities issued by another person: custodial tokenized securities and synthetic tokenized securities. The statement also warned that holders may be exposed to risks relating to the third party, including bankruptcy risk, that holders of the underlying security may not face in the same way.

Commissioner Hester Peirce made the same point in simpler language in 2025: tokenization may help capital formation and collateral use, but “tokenized securities are still securities.”

That is the right framework for investors. The token is not the asset by magic. It is a legal, technical, and operational representation of a claim. The quality of that claim depends on the structure.

A recent academic taxonomy of RWA systems reached a similar conclusion. It found that current RWA systems are mostly hybrid architectures: tokens support representation, transfer control, redemption workflows, pricing, and composability, while core legal guarantees remain anchored in off-chain wrappers, custody arrangements, compliance processes, and verification mechanisms.

Liquidity Is The Hard Test

The RWA market has spent years proving that assets can be tokenized. The harder test is whether tokenization produces usable liquidity.

A 2026 study on tokenized RWA liquidity used RWA.xyz and Etherscan data across U.S. Treasury-backed tokens, gold-backed commodity tokens, and private-credit-related tokens. It found that outstanding asset value alone does not reliably predict observed liquidity, and that gold-backed tokens showed broader holder bases and more persistent on-chain activity than many Treasury and private-credit-related products.

Another 2026 risk-scoring paper built a framework around liquidity risk, concentration risk, and market-quality risk using indicators such as turnover, holder distribution, active addresses, transfer frequency, and network concentration. Its core point is straightforward: TVL alone can hide weak trading, concentrated ownership, and poor market quality.

This is where many RWA dashboards need stricter interpretation.

A tokenized fund with $1 billion in assets and five institutional holders is not the same thing as a liquid $1 billion secondary market. A tokenized credit pool with a large represented value is not the same thing as freely transferable credit exposure. A tokenized stock wrapper is not automatically equivalent to a common share unless the legal rights, voting, dividends, custody, and redemption mechanics align.

What The Data Actually Says

The RWA market is not weak. It is uneven.

Treasuries are production-grade because they combine clear demand, simple duration, transparent underlying assets, and institutional need for yield-bearing on-chain cash. Credit is growing but structurally more complex. Commodities have a clear gold-backed use case, but are still concentrated around a few products. Tokenized equities are moving quickly, but the market is split between issuer-sponsored models, custodial wrappers, synthetic exposure, and regulated infrastructure pilots.

The best signal this week is not the total-value number. It is the institutional stack forming around tokenization:

- Securitize going public and tokenizing its own listed shares.

- DTCC preparing limited production trades for tokenized assets.

- Treasury products sitting above $14 billion in tracked value.

- Credit platforms showing double-digit 30-day distributed-value growth.

- Regulators making clear that tokenized securities remain securities.

The weakest signal is activity quality. More than half of tokenized RWA value showing no weekly transfer activity is a direct challenge to the idea that tokenization automatically creates liquidity.

Actionable Signals For Investors, Issuers, And Policymakers

| Audience | Signal To Watch | Why It Matters |

|---|---|---|

| Investors | Transfer Activity And Active Addresses | Market Cap Does Not Prove Liquidity |

| Fund Managers | Redemption Terms And Eligible Holder Rules | Whitelisting Can Limit Exit Paths |

| Token Issuers | Legal Rights Embedded In The Token Structure | Custodial, Synthetic, And Issuer-Sponsored Models Carry Different Risks |

| Market Makers | Secondary Venue Depth | Tokenization Without Bids Is Just A New Recordkeeping Layer |

| Regulators | Third-Party Wrapper Risk | Holders May Face Counterparty Risk Separate From The Underlying Asset |

| DeFi Protocols | Collateral Quality And Oracle Design | RWA Collateral Needs Pricing, Legal Enforceability, And Liquidation Clarity |

For investors, the first screen should be liquidity, not yield. A high-yield tokenized product with thin transfer activity can be harder to exit than a lower-yield Treasury product with better institutional rails.

For issuers, the bar is rising. Smart contracts and a legal memo are no longer enough. Real adoption requires distribution, custody, reporting, market making, redemption, transfer-agent integration, and credible reserve or asset verification.

For policymakers, the goal should not be to stop tokenization. It should be to force clarity around claims, rights, custody, insolvency treatment, transfer restrictions, and investor disclosures.

Key Anomalies To Watch

The first anomaly is the split between distributed and represented value. RWA.xyz showed $30.87 billion in distributed asset value against $398.59 billion represented. That is useful market information, but it also shows why readers need to distinguish tokenized issuance from off-chain reference exposure.

The second anomaly is holder growth during value contraction. Total asset holders rose 15.40% over 30 days, while distributed asset value fell 3.92%. That looks like broader distribution into a softer valuation environment, not a clean expansion of capital locked on-chain.

The third anomaly is Stellar’s growth. Stellar held only 7.28% market share, but RWA.xyz showed its RWA value up 36.02% over 30 days, outpacing Ethereum, BNB Chain, and most top networks. That deserves monitoring because Stellar has a long history in payment and asset-issuance infrastructure, and its RWA growth may reflect specific issuer/product flows rather than generalized DeFi activity.

The fourth anomaly is tokenized equities. Securitize’s SECZ tokenization shows a more serious model than many synthetic stock tokens, but the category still needs consistent rights, settlement, secondary trading, and investor-protection standards before it can be treated like a full public-equity market on-chain.

BitBullNews View

Tokenized RWAs are entering their second phase.

The first phase was proof: show that Treasuries, funds, gold, credit, and equities can be represented on-chain. That part is done. The second phase is market structure: prove that these tokens can trade, redeem, settle, report, and survive legal stress without becoming expensive wrappers around traditional assets.

Treasuries are winning because they have the clearest use case. Credit is promising but harder to price. Commodities are real but concentrated. Equities are the most politically and legally sensitive segment. Real estate remains small and fragmented in the tracked data.

The market should stop treating every RWA dollar equally. A tokenized Treasury fund with transparent reserves, regulated transfer infrastructure, and active holders is not the same as a thinly transferred private asset with limited redemption rights. Both can appear on the same dashboard. They do not carry the same risk.

What To Watch Next

The first watch item is Treasury share. If tokenized Treasury value keeps holding above $14 billion while other categories remain thin, RWAs will stay a Treasury-led market.

The second watch item is credit growth quality. Centrifuge and Securitize showed strong 30-day gains in the credit platform table, but investors should watch whether that growth comes with more holders, more transfers, and better secondary-market depth.

The third watch item is DTCC’s July 2026 limited production activity. If DTC’s tokenization service starts moving real assets through participant infrastructure, tokenization becomes less about crypto-native issuance and more about modernization of existing securities plumbing.

The fourth watch item is SEC treatment of tokenized securities. The agency’s January 2026 statement already separates custodial and synthetic models. The next important step is whether regulated exchanges, transfer agents, broker-dealers, and clearing infrastructure can support tokenized securities at scale without creating a parallel market with weaker rights.

Data Sources & References

- RWA.xyz Global Market Overview, Distributed Asset Value, Represented Asset Value, Stablecoins, Holders, And Network Tables.

- RWA.xyz Tokenized U.S. Treasuries Dashboard And Platform League Table.

- RWA.xyz Tokenized Credit Dashboard, Platform Table, And Asset Data.

- SEC Staff Statement On Tokenized Securities.

- SEC Commissioner Hester Peirce Statement On Tokenization Of Securities.

- DTCC Tokenization Service Development Update.

- DTCC Digital Assets Tokenization Page.

- Public Reporting On Securitize NYSE Debut And SECZ Tokenization.

- FinanceFeeds Report On RWA Liquidity And Concentration, Citing BeInCrypto Research And RWA.xyz.

- “Tokenized But Illiquid? Evidence From Real-World Asset Markets.”

- “Beyond TVL: An Explainable Risk Scoring Framework For Tokenized Real-World Assets.”

- “A Taxonomy Of Real-World Asset Tokenization For Blockchain-Based Financial Infrastructure.“