Content

Crypto regulation has crossed a line. The story is no longer whether major jurisdictions will regulate digital assets. They are already doing it, and the new question is which firms can survive the licensing, capital, disclosure, custody, market-abuse, and AML burden.

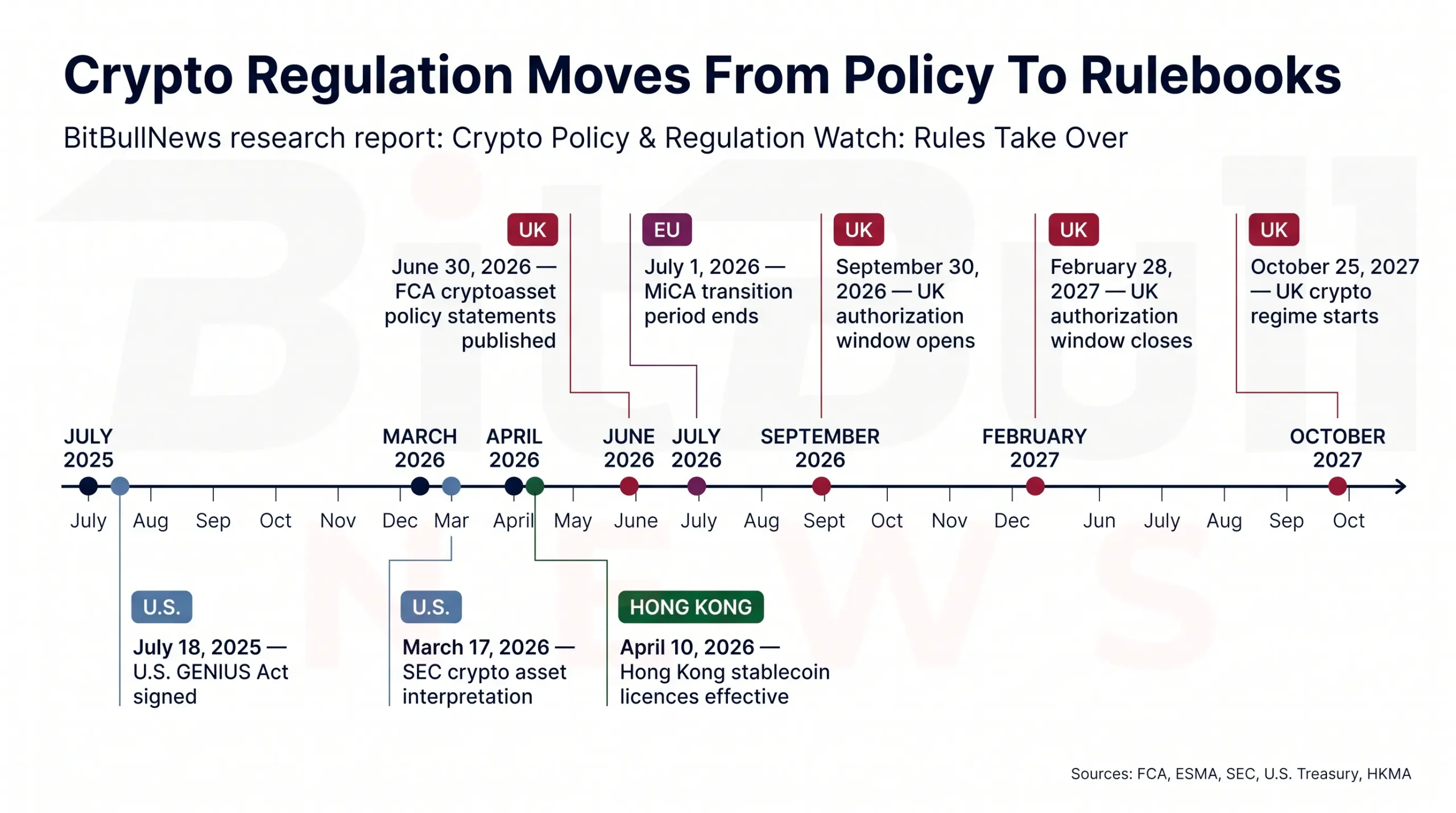

As of June 30, 2026, the most important move came from the United Kingdom. The FCA published its cryptoasset regime policy statements today, covering admissions and disclosures, market abuse, stablecoin issuance, regulated cryptoasset activities, prudential requirements, and application of the FCA Handbook. The full UK regime starts on October 25, 2027, but the authorization window opens on September 30, 2026 and closes on February 28, 2027. Existing registrations will not convert automatically.

Europe is also hitting a deadline. ESMA has told unauthorized crypto-asset service providers to wind down activity as the MiCA transitional period ends on July 1, 2026. That turns MiCA from a passporting promise into a licensing filter.

The United States is moving on a different track. The GENIUS Act became law on July 18, 2025, giving the U.S. its first federal stablecoin framework, while Treasury, FinCEN, and OFAC are now writing the implementation rules. The SEC and CFTC have also moved toward clearer agency interpretation, but the broader market-structure framework remains less settled than the stablecoin framework.

This matters because the regulated object is no longer small. DefiLlama tracks total stablecoin market capitalization at $312.3 billion, while CoinGecko shows total crypto market capitalization near $2.15 trillion. Regulators are not chasing a niche market anymore. They are setting rules for a large, dollar-linked, cross-border settlement layer.

Chart: Global Regulatory Timeline Showing The GENIUS Act Signing, Treasury Rulemaking, SEC Interpretation, Hong Kong Stablecoin Licences, FCA Policy Statements, And The MiCA July 1 Transition Deadline

Global Policy Dashboard

| Jurisdiction | Current Status | Key Date | Main Activities Covered | Market Read |

|---|---|---|---|---|

| United States | Stablecoin Law In Force; Market Structure Still Agency-Led | GENIUS Act Signed July 18, 2025 | Payment Stablecoins, AML, Sanctions, Securities Law Interpretation | Strongest On Stablecoins, Less Final On Spot Market Structure |

| European Union | MiCA Transition Ending | July 1, 2026 | CASPs, Stablecoins, Market Abuse, White Papers, Passporting | Licensing Becomes The Main Access Gate |

| United Kingdom | FCA Final Crypto Policy Statements Published | June 30, 2026; Regime Starts October 25, 2027 | Stablecoins, Custody, Trading Platforms, Staking, Lending, DeFi, Market Abuse | The UK Is Moving From AML Registration To Full FSMA Authorization |

| Hong Kong | Stablecoin Licensing Live | First Licences Effective April 10, 2026 | Fiat-Referenced Stablecoin Issuance And Relevant Stablecoin Services | Small Number Of Licensed Issuers, High Institutional Signal |

| Singapore | DPT Licensing Active; Stablecoin Framework Finalized | MAS Directory Updated June 30, 2026 | Digital Payment Token Services, Single-Currency Stablecoins | Regulated Access Model, Not Open-Ended Market Entry |

| FATF / Global AML | Stablecoins And Unhosted Wallets Under Review | Targeted Report Published March 3, 2026 | Stablecoin P2P Transfers, Unhosted Wallets, VASP Controls | AML Pressure Is Moving Closer To Wallet-Level Flows |

The Numbers Behind The Regulatory Push

The stablecoin market is the cleanest explanation for why policymakers moved faster. DefiLlama shows $312.3 billion in total stablecoin market cap, with USDT dominance at 59.13% and a 30-day market contraction of 2.30%. CoinGecko’s stablecoin category shows a similar scale, with roughly $308 billion in stablecoin market cap.

| Metric | Latest Public Reading | Source | Why It Matters |

|---|---|---|---|

| Total Crypto Market Cap | $2.148T | CoinGecko | Policy Now Affects A Trillion-Dollar Asset Class, Not A Fringe Market |

| Stablecoin Market Cap | $312.3B | DefiLlama | Stablecoins Are The Main On-Chain Dollar Liquidity Layer |

| USDT Dominance | 59.13% | DefiLlama | Issuer Concentration Remains A Market-Structure Risk |

| CoinGecko Stablecoin Category | $308B | CoinGecko | Confirms The Same Broad Scale Across A Separate Data Provider |

| Stablecoin 30D Change | -2.30% | DefiLlama | Regulation Is Arriving During A Liquidity Cooldown, Not A Pure Expansion Phase |

The regulatory cycle is now tied to liquidity, not ideology. A licensing decision can affect exchange access. A reserve rule can affect stablecoin issuance. A custody rule can affect institutional onboarding. A market-abuse rule can affect which tokens a platform lists and how quickly it delists them.

United States: Stablecoins Are Law, Market Structure Is Still Being Built

The U.S. has its clearest digital-asset rulebook in stablecoins. The GENIUS Act provides a federal framework for payment stablecoins, and Treasury’s April 2026 rulemaking states that issuers with consolidated outstanding issuance of not more than $10 billion may opt into a qualifying state-level regulatory regime if that regime is substantially similar to the federal framework.

Treasury, FinCEN, and OFAC have also proposed rules to treat permitted payment stablecoin issuers as financial institutions for Bank Secrecy Act purposes and to impose AML and sanctions compliance program requirements. That is the practical enforcement layer. Stablecoin issuers are being pulled into the same compliance perimeter that banks, money services businesses, and payment firms already understand.

The SEC’s March 17, 2026 interpretation is the other major U.S. development. The agency said it was clarifying how federal securities laws apply to certain crypto assets and transactions, and its fact sheet states that protocol mining, protocol staking, and wrapping a non-security crypto asset do not involve the offer and sale of a security under the interpretation described.

That does not solve every U.S. issue. It does, however, change the compliance conversation. For institutional firms, the U.S. path now looks split:

| U.S. Policy Track | Status | Impact On Market Participants |

|---|---|---|

| Payment Stablecoins | GENIUS Act Enacted; Treasury Rulemaking Underway | Issuers Need Reserve, Licensing, AML, Sanctions, And Disclosure Readiness |

| Securities Law Interpretation | SEC Interpretation Effective March 2026 | Token Issuers And Platforms Get More Guidance, But Facts Still Matter |

| SEC-CFTC Coordination | CFTC Joined SEC Interpretation And Issued Crypto-Related FAQs | Registered Firms Get More Operational Signals, Especially Around Derivatives And Collateral |

| Broader Spot Market Structure | Not Fully Settled In The Sources Reviewed | Exchanges Still Face Strategic Uncertainty Around Federal Jurisdiction |

The strongest U.S. policy signal is simple: dollar stablecoins are now inside federal financial regulation. The harder question is whether the U.S. can produce a durable spot-market framework without leaving exchanges in another cycle of interpretive risk.

European Union: MiCA Moves From Transition To Enforcement

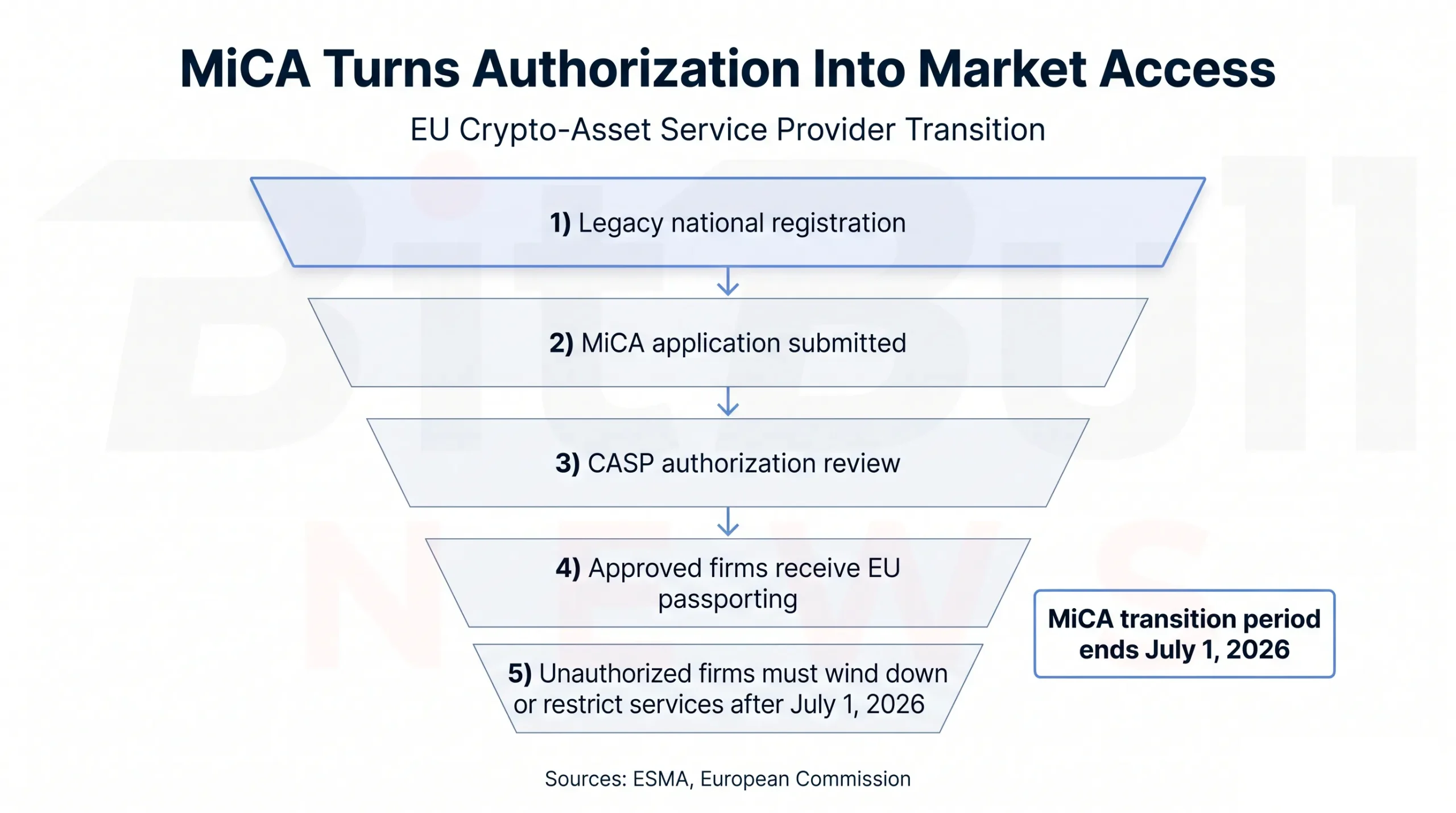

The EU is at the opposite stage. MiCA is not waiting for a first framework. It is moving into full operational enforcement.

ESMA has clarified that crypto-asset service providers that operated legally before December 30, 2024 could rely on the transitional regime only until July 1, 2026, or until they were granted or refused authorization, whichever came first. ESMA’s June 2026 statement tells unauthorized CASPs to wind down in an orderly way and protect client interests as that deadline arrives.

That creates a real market-access event. A firm that does not have MiCA authorization cannot treat EU access as business as usual. The practical outcomes are likely to be tighter onboarding, more conservative token listings, and more pressure on offshore platforms serving EU clients.

The European Commission is already reviewing whether MiCA remains fit for purpose after initial implementation. Its May 2026 consultation asks whether the framework should be adjusted in light of market and policy developments since entry into application.

| MiCA Area | Current Signal | Market Impact |

|---|---|---|

| CASP Authorization | Transitional Period Ends July 1, 2026 | Unauthorized Providers Face Exit Or Service Restrictions |

| Stablecoins | ARTs And EMTs Covered Under MiCA | Issuers Must Operate Inside A Formal Reserve And Supervision Framework |

| Market Abuse | MiCA Includes Market Integrity Requirements | Trading Venues Need Surveillance, Reporting, And Disclosure Controls |

| EU Passporting | Authorization Becomes The Access Key | Licensed Firms Gain A Stronger Competitive Position |

| Review Process | Commission Is Reviewing MiCA | DeFi, Non-EU Access, And Market Scope Could Become Next-Phase Issues |

The EU advantage is regulatory completeness. The EU risk is fragmentation in application. If national supervisors apply MiCA unevenly, firms will still shop for the most workable entry point. That is exactly why ESMA keeps stressing supervisory convergence.

Chart: EU MiCA Enforcement Funnel Showing Legacy National Registration, CASP Authorization, Passporting, And Wind-Down For Unauthorized Firms

United Kingdom: The FCA Turns Crypto Into A Full FSMA Regime

The UK just delivered the most detailed policy package of the week.

The FCA’s June 30 policy statements cover five core pillars: admissions and disclosures with a market-abuse regime, stablecoin issuance, regulated cryptoasset activities, prudential requirements, and application of the FCA Handbook. The FCA says the regime is underpinned by the Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026 and will bring a broad range of cryptoasset activities inside its perimeter from October 25, 2027.

The detail matters. The FCA is applying key Handbook obligations across regulated cryptoasset activities, including Consumer Duty, conduct rules, senior-manager accountability, operational resilience, and financial crime frameworks. That is a major shift from the UK’s previous position, where crypto firms were mainly inside the perimeter for AML registration and financial promotions.

For stablecoins, the FCA maintained its core framework but made changes for proportionality and operability. It simplified backing-asset composition requirements, confirmed statutory trust arrangements for backing assets, adjusted redemption timelines, allowed limited intragroup custody subject to safeguards, and permitted up to a 5% excess in the backing asset pool.

The prudential section is where the market will pay attention. The FCA cut the stablecoin issuance K-factor coefficient from 2% to 1%, and qualifying cryptoassets that can be prudently valued and are admitted to a UK qualifying cryptoasset trading platform will face a 40% net risk position requirement and a 40% volatility adjustment. Cryptoassets that do not meet the conditions are deducted from regulatory capital and receive a 100% volatility adjustment for counterparty credit default.

| UK Rule Area | Final FCA Direction | Institutional Takeaway |

|---|---|---|

| Stablecoin Issuance | Backing Asset, Redemption, Disclosure, And Safeguarding Rules Finalized | Issuers Need Treasury-Grade Reserve Controls |

| Crypto Custody | CASS 17 Safeguarding For Client Cryptoassets | Custody Becomes A Formal Control Function |

| Trading Platforms | Admissions, Disclosure, Due Diligence, And Market Abuse Controls | Token Listings Become A Compliance Event |

| Lending And Borrowing | Enhanced Disclosures, Consent, Appropriateness Testing, Records, And Safeguards | Retail Credit-Like Crypto Products Face Heavy Scrutiny |

| Staking | Disclosures, Contractual Terms, Consent, And Record-Keeping | Staking Moves From Product Feature To Regulated Service |

| DeFi | Rules Apply Where There Is An Identifiable Controlling Entity | “Decentralized” Will Not Be A Complete Shield |

The FCA’s DeFi position deserves special attention. The regulator says its rules and guidance will apply where there is an identifiable controlling entity, and it plans tailored DeFi guidance with objective indicators of decentralization. That is a clear warning to front ends, governance groups, and protocol operators that labels will matter less than control.

The UK is not done. The FCA says more work is coming on DeFi, DLT, cryptoasset derivatives, stablecoin policy, audit requirements, transitional provisions, resolution, financial crime, and regulatory reporting. The first package is final, but the operating regime will keep expanding.

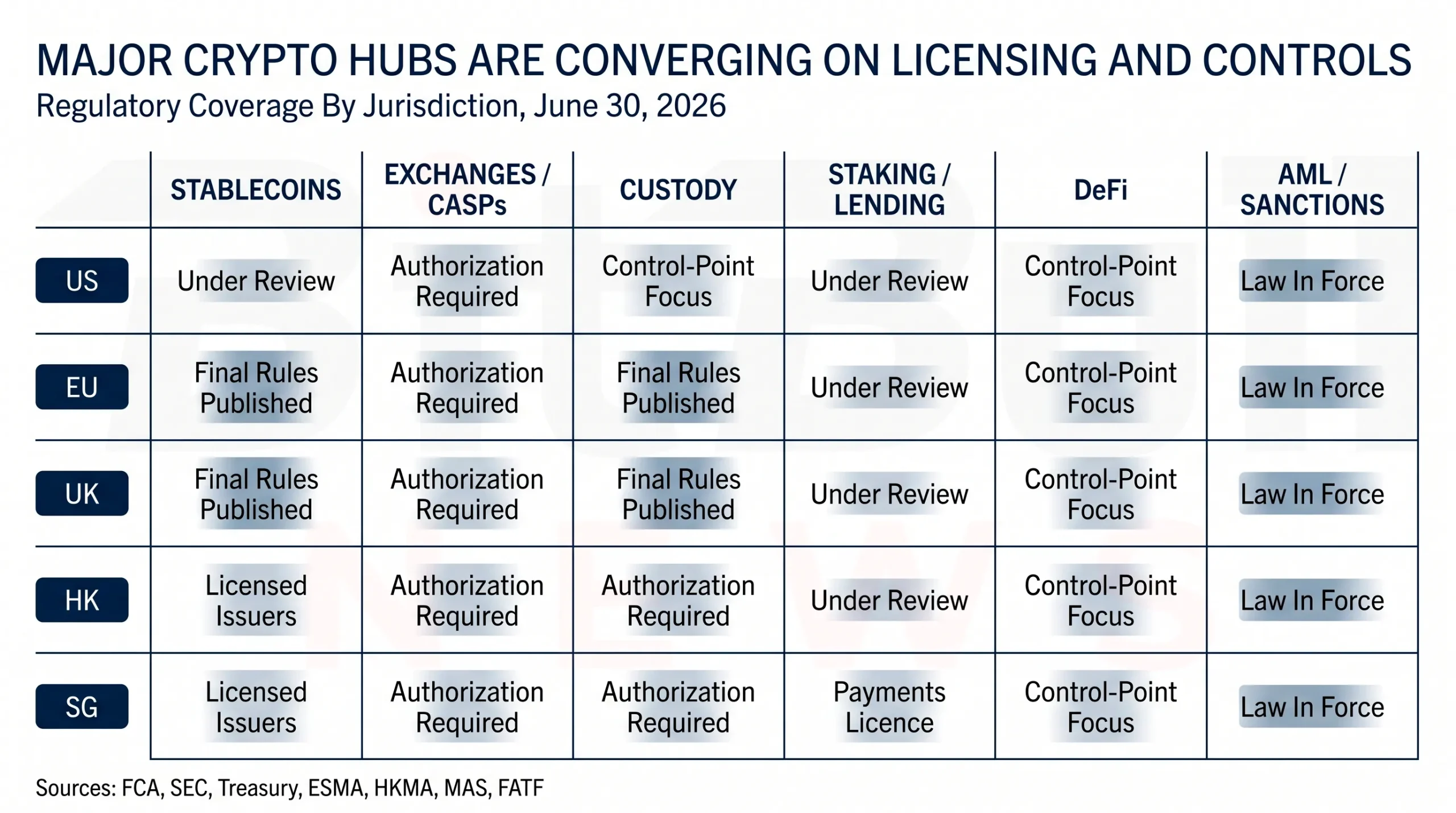

Asia: Hong Kong Licenses Stablecoins, Singapore Keeps The Gate Narrow

Hong Kong has moved from consultation to visible licensing. The HKMA register lists two licensed stablecoin issuers under the Stablecoins Ordinance: Anchorpoint Financial Limited and The Hongkong And Shanghai Banking Corporation Limited, both effective April 10, 2026.

That is a small number, and that is the point. Hong Kong is not opening the door to every issuer. It is building a supervised stablecoin channel tied to licensed entities, bank-grade controls, and public registration. The SFC’s May 2026 circular also sets expected standards for licensed virtual asset trading platforms and licensed corporations when dealing with “Relevant Stablecoins.”

Singapore is taking a broader payments-licensing route. MAS’s Financial Institutions Directory shows 37 results for Digital Payment Token Service under Major Payment Institution status, while MAS’s stablecoin framework applies to single-currency stablecoins pegged to the Singapore dollar or a G10 currency and issued in Singapore.

| Market | Regulatory Access Point | Current Signal | Strategic Read |

|---|---|---|---|

| Hong Kong | HKMA Stablecoin Issuer Licence | Two Licensed Issuers Listed | Stablecoin Issuance Is Institution-Led |

| Hong Kong | SFC Relevant Stablecoin Standards | Licensed Platforms Must Meet Expected Standards | Trading Access Depends On Regulatory Classification |

| Singapore | MAS DPT Licensing | 37 Major Payment Institution DPT Results | Crypto Access Runs Through Payment Regulation |

| Singapore | MAS Stablecoin Framework | SGD And G10-Pegged SCS Issued In Singapore Covered | Stablecoin Policy Focuses On Reserves, Audit, Custody, And Value Stability |

Asia’s pattern is not deregulation. It is curated market access. Hong Kong is using stablecoins as a controlled financial-market product. Singapore is using payments licensing and stablecoin reserve standards to keep digital money inside a supervisory perimeter.

Chart: Jurisdiction Comparison Matrix Showing U.S., EU, UK, Hong Kong, And Singapore Across Stablecoins, Exchanges, Custody, Staking, DeFi, And AML

FATF And AML: Stablecoins Move To The Top Of The Illicit-Finance File

The FATF’s March 2026 report puts stablecoins and unhosted wallets directly in the AML spotlight. The report focuses on illicit-finance risks linked to stablecoin misuse, especially peer-to-peer transactions through unhosted wallets, and recommends stronger controls for countries and private-sector actors.

This is where the policy debate becomes difficult. Stablecoins are useful because they move quickly, settle globally, and work outside bank hours. Those same properties make them attractive for sanctions evasion, fraud, ransomware settlement, and laundering through peer-to-peer routes.

The regulatory direction is predictable:

- Licensed issuers will face stronger wallet-screening, redemption, and sanctions controls.

- VASPs will be pushed to improve counterparty due diligence and Travel Rule implementation.

- Platforms will face more pressure to identify when “self-hosted” activity is really professional intermediation.

- DeFi interfaces with identifiable operators will have less room to claim they sit outside compliance rules.

The next battle is not whether AML applies to crypto. It is where the obligation attaches when value moves through smart contracts, self-custody wallets, bridges, and stablecoin issuers at the same time.

What Changed In Market Structure

The regulatory shift is compressing the gap between crypto-native firms and traditional finance. That does not mean banks automatically win. It means the winning crypto firms will start looking more like regulated financial institutions in their treasury operations, controls, disclosures, custody systems, and governance.

The largest change is in token listing. In the UK and EU, listing is moving from a growth function to a controlled approval process. Platforms will need due diligence, disclosure files, market-abuse monitoring, and rules for withdrawal rights or supplementary disclosure where required.

The second change is in stablecoin reserve management. The U.S., UK, Hong Kong, Singapore, and EU are not using identical rulebooks, but they are converging around the same policy demands: high-quality reserves, redemption rights, disclosures, custody controls, AML controls, and supervisory access.

The third change is in DeFi. Regulators are not trying to regulate every smart contract line by line. They are looking for control points: front ends, administrators, governance entities, intermediaries, custody arrangements, and fee-taking entities. The FCA’s “identifiable controlling entity” approach is likely to become a reference point for other regulators watching DeFi without pretending every protocol is the same.

Actionable Signals For Traders, Investors, And Firms

| Audience | Signal To Watch | Why It Matters |

|---|---|---|

| Traders | Exchange Licensing Status In The EU And UK | Token Availability And Liquidity Could Shift As Unauthorized Firms Exit Or Restrict Access |

| Stablecoin Users | Issuer Licence, Reserve Disclosure, Redemption Rights | The Safest Stablecoin Is Not Always The Most Liquid One |

| Institutional Investors | Custody Rule Alignment Across Jurisdictions | Asset Managers Need Custody Structures That Work Across SEC, FCA, MiCA, And Asian Regimes |

| Token Issuers | Listing Disclosure Requirements | Launch Strategy Now Needs Legal, Technical, And Market-Abuse Review Before Exchange Admission |

| DeFi Teams | Control, Governance, Front-End, And Fee Structures | “Protocol” Status Will Not Protect A Clearly Controlled Business |

| Policymakers | Cross-Border Stablecoin Flows And Offshore VASPs | Regulation Can Be Strong Domestically And Still Leak Through Unlicensed Foreign Access |

For traders, the near-term risk is access fragmentation. A token can remain liquid globally while becoming harder to trade in one jurisdiction. That matters for spreads, exchange routing, and market depth.

For investors, the core question is counterparty quality. A licensed custodian, regulated stablecoin issuer, and authorized trading platform now carry strategic value. Regulatory status is becoming part of due diligence, not a back-office detail.

For crypto firms, the lesson is harsher. Firms that delay authorization work until 2027 may already be late. The FCA’s application window opens in three months, and MiCA’s transition ends tomorrow.

Key Anomalies And Open Questions

The first anomaly is timing. The UK has published final policy statements but will not switch on the full regime until October 2027. The EU, by contrast, is already at the end of its MiCA transition. This creates a temporary arbitrage window where Europe is stricter on live authorization while the UK is stricter in published future detail.

The second anomaly is the U.S. split between stablecoin clarity and broader market-structure uncertainty. Stablecoins now have a federal statute and Treasury implementation path. Many other crypto assets still depend on SEC interpretation, CFTC coordination, and unresolved legislative work.

The third anomaly is Hong Kong’s small license count. Only two stablecoin issuers are currently listed by HKMA. That is not a weak signal. It suggests a deliberate institutional rollout rather than a broad issuer land rush.

The fourth anomaly is DeFi. Regulators increasingly agree that pure software is different from controlled intermediation, but they have not settled the operational test. The UK’s promised indicators of decentralization will be important beyond the UK because they may shape how lawyers classify governance, front-end control, treasury management, and protocol revenue.

BitBullNews View

The regulatory center of gravity has shifted from enforcement after the fact to licensing before market access.

That is bullish for large, well-capitalized firms with compliance teams, banking relationships, custody infrastructure, and issuer-grade disclosures. It is bearish for offshore exchanges, thinly governed issuers, opaque stablecoin structures, and DeFi projects with centralized control points but no regulatory plan.

The market should not treat regulation as a single global event. The U.S. is building stablecoin rules first. The EU is enforcing a comprehensive rulebook. The UK is publishing detailed future rules and opening its gateway soon. Hong Kong is licensing stablecoin issuers selectively. Singapore is keeping digital-token services inside a payments framework.

The common thread is tighter access. Crypto is not being banned in major financial centers. It is being filtered.

What To Watch Next

The first watch item is the MiCA transition on July 1, 2026. The key signal will be which firms restrict EU access, transfer clients, halt marketing, or secure authorization.

The second watch item is the FCA gateway on September 30, 2026. Applications filed early will tell the market which firms are serious about remaining in the UK under FSMA authorization.

The third watch item is Treasury’s GENIUS Act implementation. The state-versus-federal pathway for issuers below the $10 billion threshold could shape whether stablecoin competition stays broad or consolidates around federally supervised giants.

The fourth watch item is DeFi perimeter guidance. The next phase of regulation will not be about whether DeFi exists. It will be about who controls the interface, who earns fees, who can change the system, and who is responsible when users are harmed.

Data Sources & References

- FCA Cryptoasset Regime Policy Statements, Published June 30, 2026.

- FCA Summary Of Final Rule Changes Across Stablecoins, Custody, Trading, Staking, Lending, DeFi, Market Abuse, And Prudential Requirements.

- FCA Preparation Page For The New Cryptoasset Regulatory Regime.

- SEC Interpretation On Application Of Federal Securities Laws To Crypto Assets, March 17, 2026.

- SEC Fact Sheet On Crypto Asset Interpretation.

- CFTC Release On SEC-CFTC Crypto Asset Interpretation.

- U.S. Treasury GENIUS Act State-Level Regulatory Regime NPRM.

- U.S. Treasury / FinCEN / OFAC GENIUS Act AML And Sanctions Proposed Rule.

- White House Statement On GENIUS Act Signing.

- ESMA / AMF Statement On MiCA Transitional Period Ending.

- ESMA Q&A On MiCA Transitional Period.

- European Commission Targeted Consultation On MiCA Review.

- HKMA Register Of Licensed Stablecoin Issuers.

- Hong Kong SFC Circular On Relevant Stablecoin Services.

- MAS Financial Institutions Directory For Digital Payment Token Services.

- MAS Stablecoin Regulatory Framework.

- FATF Targeted Report On Stablecoins And Unhosted Wallets.

- DefiLlama Stablecoin Market Cap, Supply, And Peg Data.

- CoinGecko Global Crypto Market Data And Stablecoin Category Data.