Content

Start with the uncomfortable part. If you hold crypto in your own wallet, it is almost certainly not insured, and no realistic policy will make you whole if you lose your seed phrase or get phished.

That’s not a scare tactic. It’s the structure of the market. Insurance exists in crypto, but it protects institutions and platforms far more than it protects you, and the coverage that does reach retail holders excludes exactly the losses people suffer most. This guide lays out what’s actually available, what each layer really covers, and what you’re left to handle yourself.

Government Insurance Does Not Cover Crypto

This is the first thing to get straight, because plenty of platforms have blurred it — some deliberately.

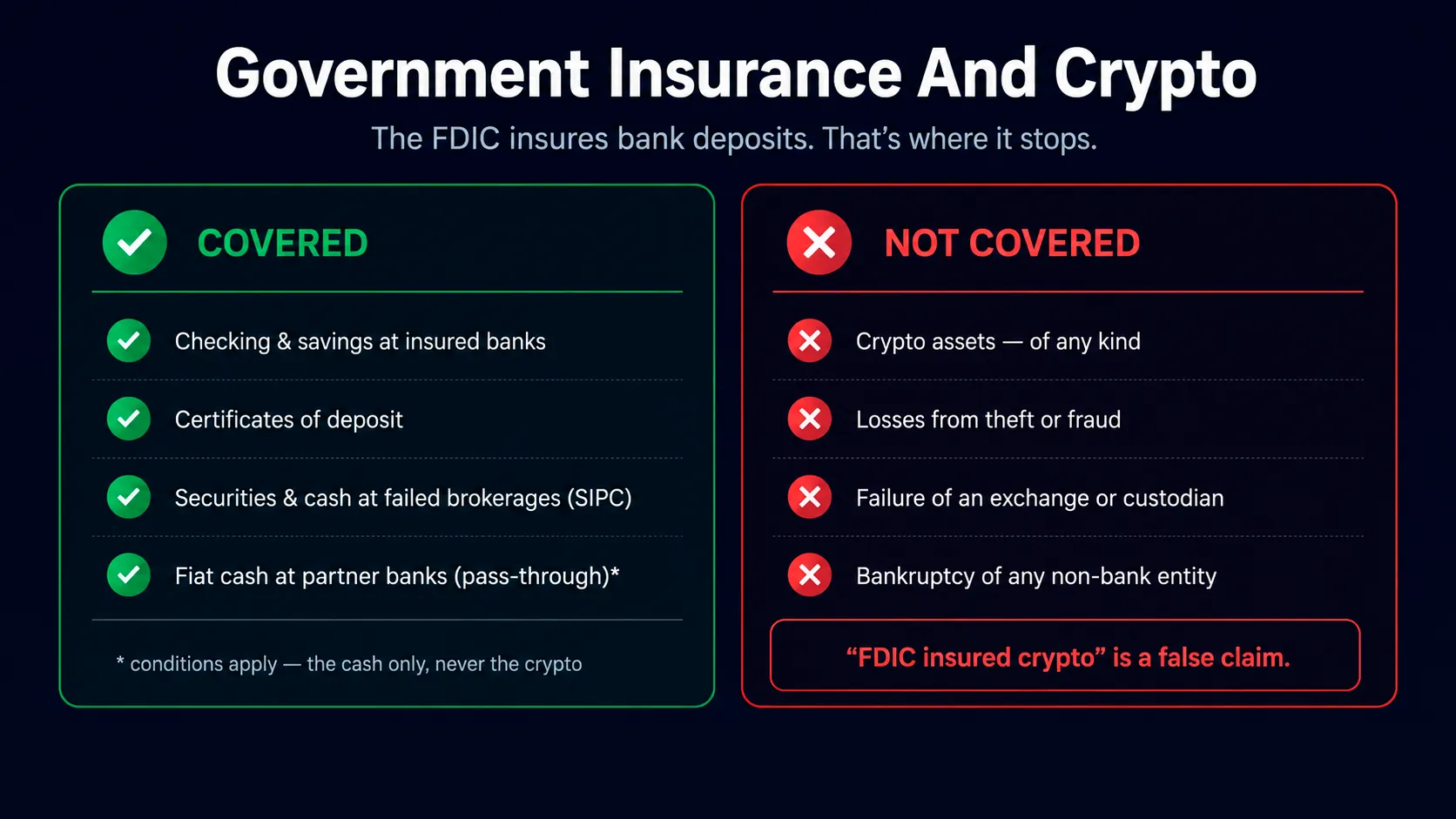

The FDIC states it plainly: deposit insurance does not apply to crypto assets, it does not cover losses from theft or fraud, and it does not protect against the failure or bankruptcy of any non-bank entity, including crypto exchanges, custodians, brokers, and wallet providers. The FDIC insures deposits at insured banks, and nothing else.

SIPC doesn’t fill the gap either. It protects securities and cash at failed member brokerages. Cryptocurrency isn’t a security in that sense and isn’t covered.

One narrow exception is worth knowing. If a platform holds your US dollar cash balance in custodial accounts at partner banks, that cash may qualify for pass-through FDIC coverage, subject to conditions. Your Bitcoin, Ether, and tokens never do.

Warning: Any platform implying your crypto is “FDIC insured” is misrepresenting the facts. The FDIC has taken enforcement action over exactly this claim.

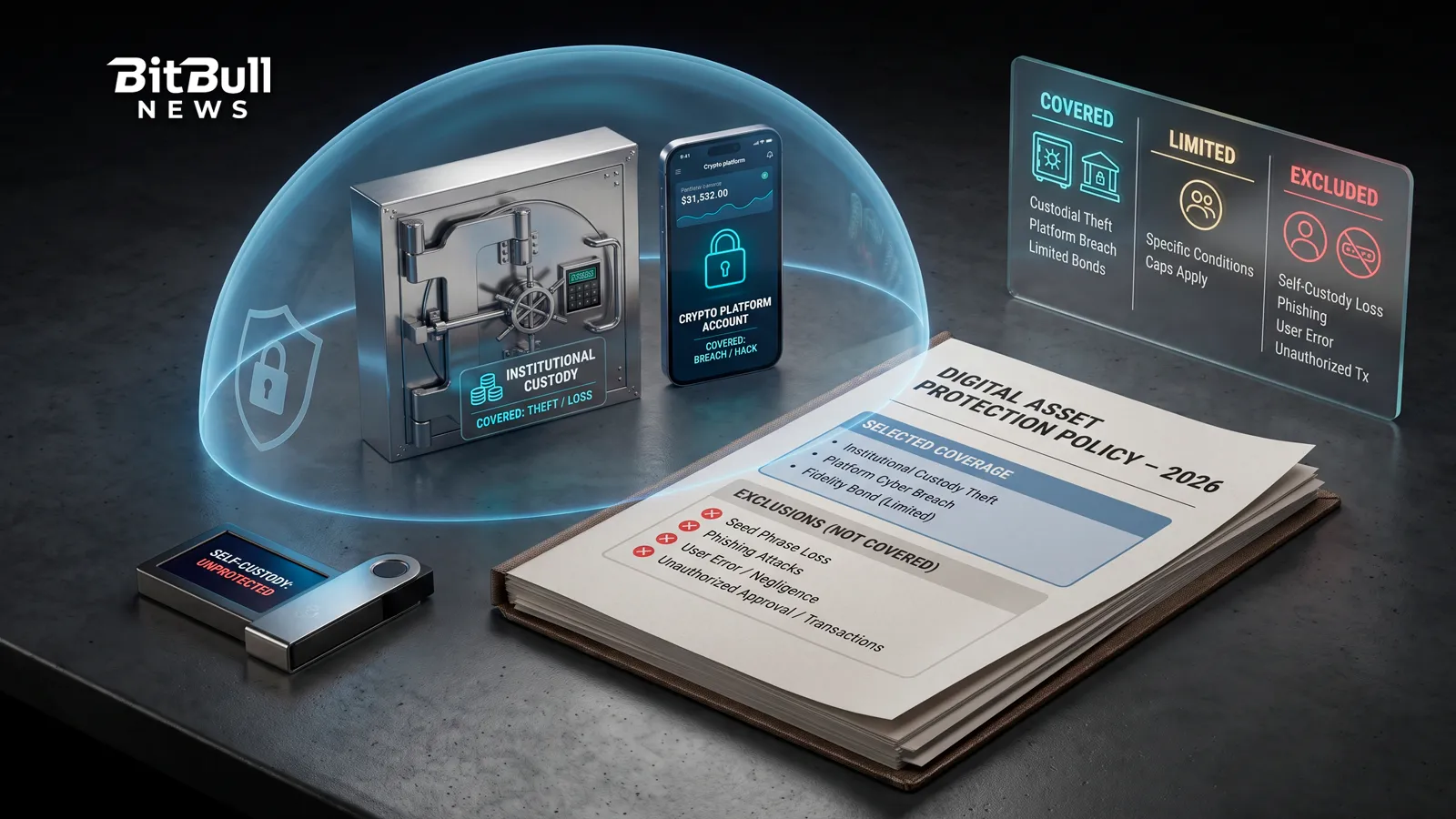

Exchange Crime Insurance: What It Really Protects

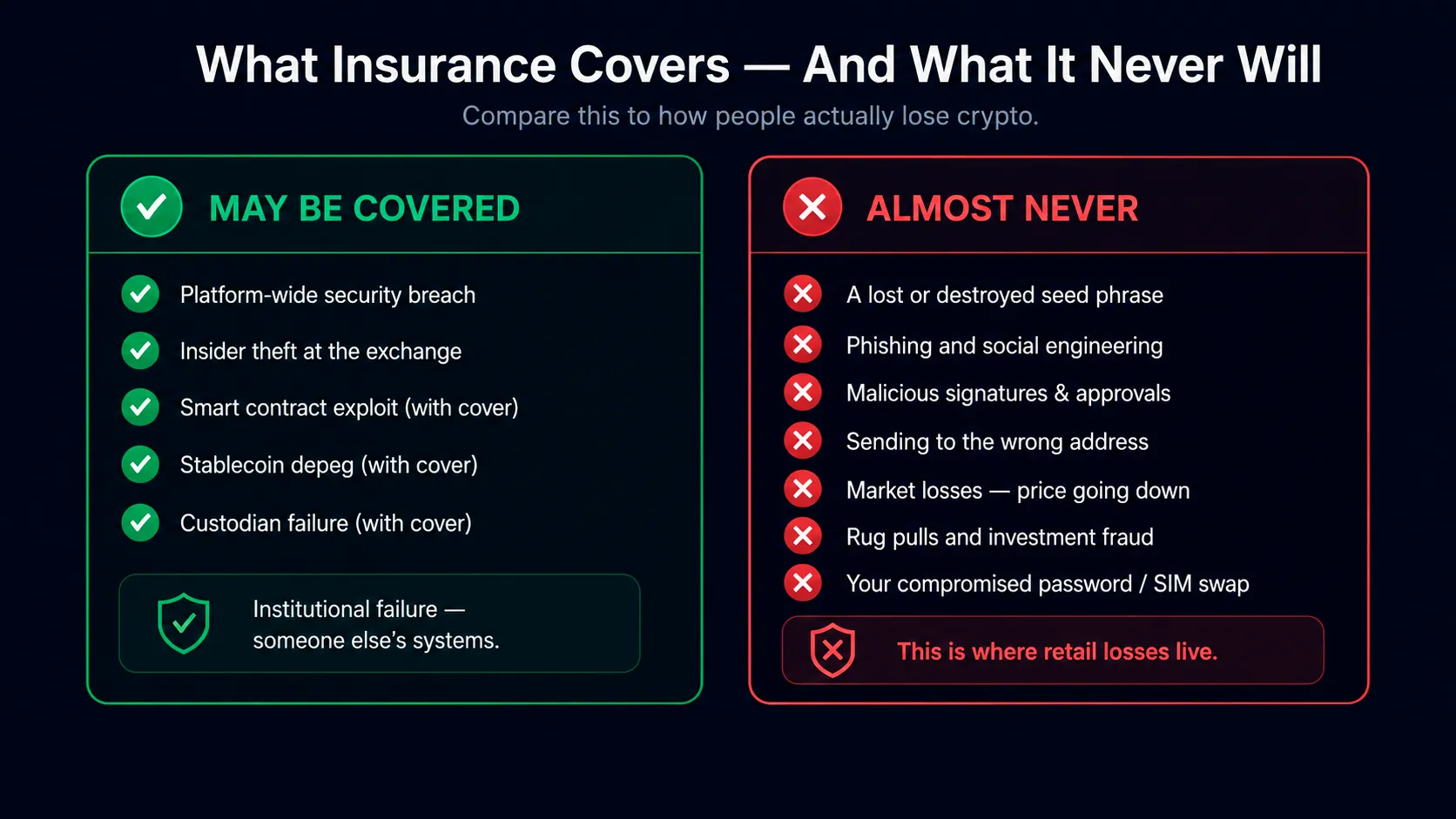

Large exchanges and custodians carry commercial crime policies, usually underwritten through specialist markets like Lloyd’s syndicates. These cover theft of digital assets from the platform’s own storage systems — a cybersecurity breach of the exchange, or insider theft.

Read that carefully. It insures the platform, not your account.

Coinbase, which publishes its position clearly, says its crime insurance covers a portion of digital assets held across its storage systems against theft — but explicitly does not cover losses from unauthorized access to your personal account due to a breach or loss of your credentials. Protecting your password and login is your responsibility.

That single carve-out is the whole story. If a hacker breaches the exchange, the policy may respond. If a phisher gets into your account, or you’re SIM-swapped, or you approve a malicious signature, it won’t.

The exclusions in these policies (visible in custodians’ public filings) typically run further:

- Losses from unauthorized access to a customer’s account.

- Fraud committed by the company’s own officers or directors.

- Catastrophic failure of a cryptocurrency or protocol itself.

- Terrorism and force majeure events.

Coverage is also capped, and the cap applies across the whole platform — not per user. A breach larger than the policy limit means losses may exceed what insurance pays.

Some exchanges also maintain self-funded reserve pools instead of, or alongside, third-party insurance. These are company promises backed by company money, not enforceable insurance contracts. They’ve paid out before. They’re also discretionary.

Qualified Custodians And Institutional Coverage

If you’re an institution, a fund, or a very large holder, real coverage exists. Qualified custodians — regulated firms that hold assets on your behalf — carry specie and crime policies covering cold storage, often placed with Lloyd’s syndicates.

This is the most substantive insurance in crypto. It’s also mostly out of reach for individuals: high minimums, institutional onboarding, and fees that only make sense at scale.

The trade-off is real, too. You give up self-custody. You’re now exposed to the custodian’s solvency and operational risk instead of your own key management — which is a different risk, not a smaller one.

DeFi Cover Protocols

On-chain, a different model emerged. Protocols like Nexus Mutual let members pool capital and buy cover against specific crypto-native risks, with claims assessed by member vote rather than an insurance company.

Typical cover products include:

- Protocol cover — losses from smart contract exploits, oracle manipulation, or governance attacks on a DeFi protocol.

- Custody cover — failure of a centralized custodian or exchange.

- Depeg cover — a stablecoin or yield-bearing token losing its peg for a sustained period.

Understand what you’re buying. Most of these are discretionary mutuals, not regulated insurance. Claims are decided by members, payouts depend on the pool’s capital, and you take on the mutual’s own smart contract and solvency risk. Cover is time-limited, capacity is finite, and pricing moves with perceived risk.

And the key exclusion again: they don’t cover lost private keys, phishing, or your own mistakes.

What Insurance Almost Never Covers

Here’s the list that matters most, because it’s where nearly all retail losses actually happen.

- A lost or destroyed seed phrase. No policy resurrects a secret that no longer exists.

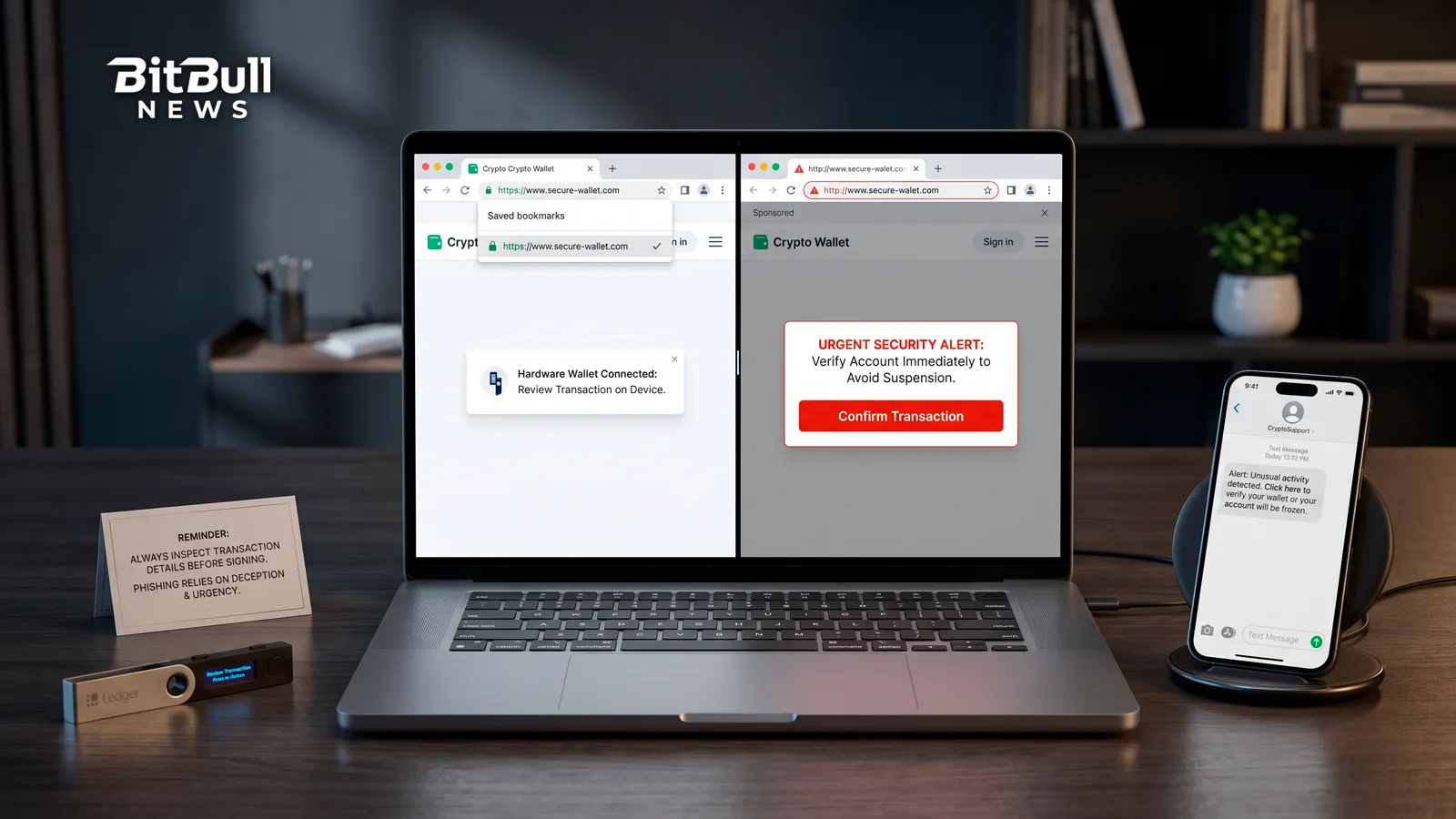

- Phishing, scams, and social engineering. You authorized it. That’s the whole design of the attack.

- Malicious signatures and token approvals you granted yourself.

- Sending funds to the wrong address. Irreversible, and not an insurable event.

- Market losses. Insurance covers theft and failure, never price.

- Rug pulls and investment fraud in the project you chose.

- Your compromised credentials — the explicit carve-out in exchange policies.

Read that list again and compare it to how people actually lose crypto. The overlap is nearly total. Insurance protects against institutional failure. It does not protect against you.

How To Evaluate Any Crypto Insurance Claim

Whenever a platform advertises that your assets are “insured,” ask these questions before you believe it.

- Who is the policyholder? If it’s the company, the policy protects the company’s balance sheet — not your individual account.

- What exactly triggers a payout? Platform breach only? Or does it reach account-level theft?

- Is my account compromise covered? Almost always no. Get this in writing.

- What’s the cap, and is it per-user or platform-wide? A shared cap can be exhausted by a single large event.

- Who underwrites it? A named regulated insurer, a discretionary mutual, or a company promise?

- What are the exclusions? Read them. They’re the actual product.

- Has it ever paid out? A track record beats a marketing page.

If a platform won’t answer these clearly, treat the “insured” label as marketing.

Self-Insurance Is The Realistic Answer

For almost every individual holder, your security setup is your insurance policy. It’s not a consolation prize — it’s a better instrument, because it prevents the loss instead of arguing about it afterward.

- Cold storage for anything long-term. A hardware wallet removes the risks that no policy would have covered anyway.

- Multisig for meaningful holdings, so one compromised key doesn’t end you.

- Redundant, offline seed backups in separate locations, ideally on metal.

- Split wallets — a small hot wallet for apps, a cold wallet that never signs anything risky.

- Regular approval revocation and disciplined signing habits.

- Spread counterparty risk. Don’t keep everything on one platform, insured or not.

- Size your exposure honestly. Hold what you can afford to lose entirely, because that’s the actual downside.

A few hundred dollars of hardware and an hour of setup outperform any policy you can realistically buy as an individual.

The Market Changes — Verify Before You Rely On It

Coverage terms, providers, limits, and regulatory treatment all shift, and some cover protocols that existed a few years ago no longer operate. Treat the specific products named here as examples of models, not a permanent catalog.

The structure, though, has been stable for years: governments don’t insure crypto, platform policies protect platforms, institutional custody insurance is real but out of retail reach, and self-custody losses are on you. Confirm the current terms directly with any provider, and read the exclusions before you count on anything.

FAQ

- Is My Crypto FDIC Insured?

No. The FDIC does not insure crypto assets, does not cover theft or fraud, and does not protect you if a crypto exchange or custodian fails. Only US dollar cash balances held at partner insured banks may qualify for pass-through coverage — never the crypto itself. - Does Exchange Insurance Protect My Account If I Get Hacked?

Generally no. Exchange crime policies cover theft from the platform’s own storage systems. They explicitly exclude losses from unauthorized access to your personal account through phishing, SIM swapping, or stolen credentials — that’s your responsibility. - Can I Insure Crypto Held In My Own Hardware Wallet?

Realistically, no. Retail self-custody insurance barely exists, and the losses that actually happen to individuals — lost seed phrases, phishing, bad signatures — are exactly what policies exclude. Your security setup is your coverage. - What Is DeFi Cover, And Is It Real Insurance?

DeFi cover protocols let members buy protection against smart contract exploits, custodian failure, and stablecoin depegs. Most are discretionary mutuals rather than regulated insurance, so claims are decided by member vote and payouts depend on the pool’s capital. - Will Insurance Pay If I Lose My Seed Phrase?

No. A lost seed phrase isn’t an insurable event, because nothing was stolen and nothing can be reconstructed. This is the single most common way people lose crypto, and it’s uninsurable — which is why redundant offline backups matter so much. - Does Insurance Cover Losses From A Scam Or Rug Pull?

No. Scams, phishing, and rug pulls involve transactions you authorized, so they fall outside theft coverage. Insurance addresses institutional failure and platform breaches, not decisions you were tricked into making. - Are Insured Exchanges Safer Than Uninsured Ones?

Somewhat, but less than the label suggests. The policy protects the platform against a breach, is capped platform-wide, and won’t help if your individual account is compromised. Security practices, solvency, and proof of reserves tell you more than an “insured” badge.