Content

TL;DR

- State Street plans to launch tokenized fund servicing from Luxembourg.

- The move builds on State Street’s Digital Asset Platform, which supports tokenized funds, ETFs, cash products, tokenized deposits and stablecoins.

- Luxembourg gives the rollout a practical European base because it is one of the region’s most important fund domiciles.

- The real shift is that tokenization is moving from product wrappers into fund servicing, operations and back-office infrastructure.

State Street is moving its tokenization push deeper into European fund infrastructure.

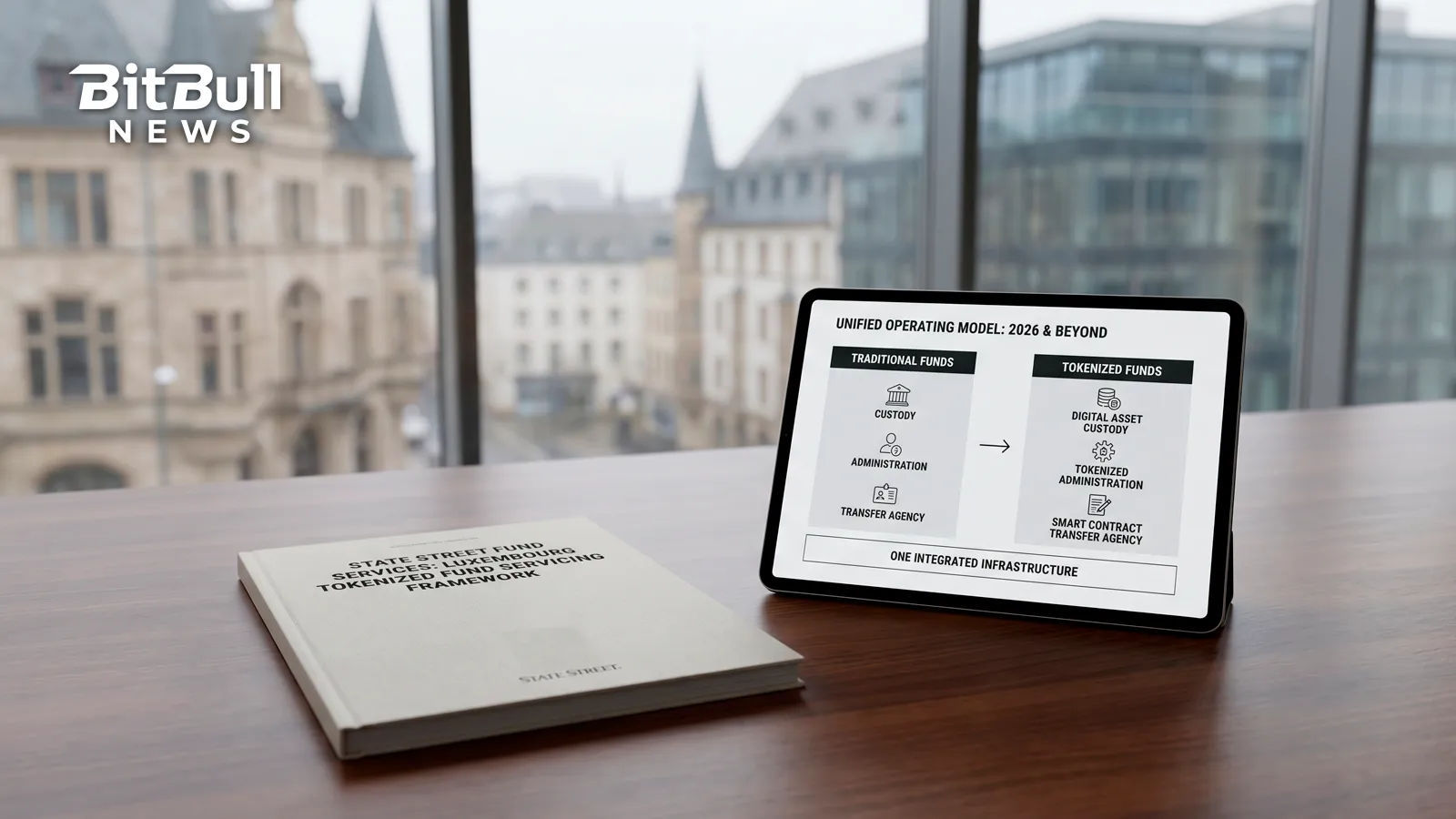

The custody and asset-servicing giant said it will launch tokenized fund servicing from Luxembourg, giving asset managers a new route to support tokenized fund products from one of Europe’s key fund hubs.

Simply put, this is not just about putting a fund onchain. It is about making the operational layer behind tokenized funds look more like the infrastructure asset managers already use.

State Street Is Taking Tokenization Into Fund Servicing

The key change is where the tokenization story is moving.

Earlier this year, State Street launched its Digital Asset Platform to support tokenized products such as money market funds, ETFs, tokenized assets, deposits and stablecoins. Now the company is tying that strategy to fund servicing from Luxembourg, a market built around cross-border fund administration and distribution.

That matters because asset managers do not only need token issuance. They also need servicing, accounting, custody, cash handling, reporting, compliance controls and connections to traditional systems. Without that layer, tokenized funds can look interesting onchain but hard to run at institutional scale.

This is the same direction showing up across tokenized securities more broadly: the market is moving from “can we tokenize this asset?” to “can we operate it safely inside existing financial workflows?”

Luxembourg Gives The Rollout A Real Distribution Angle

Luxembourg is not a random launch location. It is one of Europe’s most important fund domiciles and a major base for UCITS, ETFs and cross-border investment products.

That gives State Street’s move more weight. If tokenized funds are going to reach European asset managers, they need infrastructure in jurisdictions that already understand fund servicing, oversight and distribution.

State Street’s own 2026 ETF outlook also points to Luxembourg’s role in the next phase of fund innovation. The report notes that Luxembourg ETF assets surpassed EUR 500 billion at the end of 2025 and describes the market as a leading platform for active ETF growth, supported by regulatory and operational developments.

That context helps explain the timing. Tokenization is arriving just as asset managers are already rethinking wrappers, share classes, active ETFs and distribution models.

What Changed

Before this, State Street’s tokenization story was mostly about platform capability: digital wallets, custody, cash functions and support for tokenized products.

Now the company is attaching those capabilities to a specific fund-servicing hub. That changes the story from technology readiness to market execution.

For asset managers, the practical question becomes less abstract. Instead of asking whether tokenized funds are possible, they can start asking whether their administrator, custodian and servicing partner can support them in a regulated fund center.

That is where large asset servicers have an advantage. Crypto-native firms can build fast, but they rarely control the full operational stack that traditional fund managers already rely on.

Who It Affects Now

The immediate audience is asset managers exploring tokenized fund launches in Europe.

It also matters for ETF issuers, fund administrators, transfer agents, custodians and platforms building tokenized distribution models. If State Street can service these products from Luxembourg, it gives large managers a more familiar path into tokenization without forcing them to rebuild the entire operating model.

For institutional clients, the benefit is more practical than flashy: tokenized products may become easier to launch, administer and connect with existing reporting and custody workflows.

The same market-structure shift is already visible in tokenized collateral, where institutions are starting to use tokenized Treasury products inside trading workflows instead of treating them only as passive onchain holdings.

Why It Matters

This story matters because tokenized finance will not scale on issuance alone.

Fund managers need trusted infrastructure that can handle the full lifecycle of a product: launch, servicing, custody, valuation, recordkeeping, reporting and investor operations. State Street is trying to own that layer before tokenized funds become a larger part of mainstream asset management.

The next thing to watch is whether State Street names the first Luxembourg-serviced tokenized fund clients and what types of products come first. Money market funds and short-duration products remain the most obvious candidates, but ETFs and other regulated fund structures could become the more interesting test.

The bigger signal is clear: tokenization is moving into the back office. Once major custodians and fund servicers start building around it, the market stops looking like a crypto experiment and starts looking like a slow rebuild of financial infrastructure.