Content

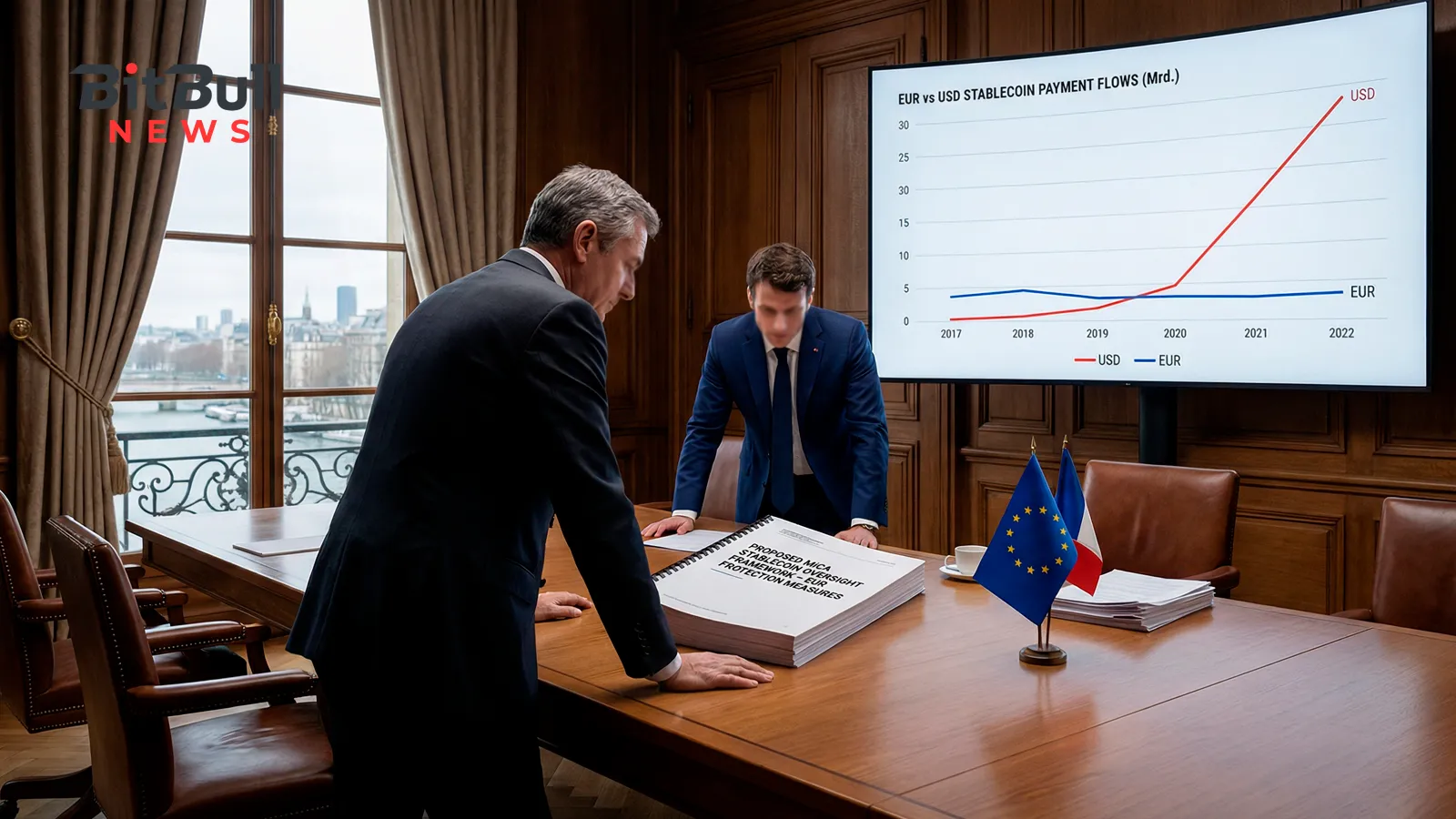

Europe needs to move faster and more aggressively if it wants tokenized finance to develop without sliding into what Banque de France calls “stablecoinisation” and “dollarisation” of the payment system. In speaking points delivered on March 26, First Deputy Governor Denis Beau said the EU should respond to predominantly dollar-denominated stablecoins with a three-part strategy: adapt central bank money for tokenized finance, support euro-based tokenized private money, and strengthen regulation.

The strongest news angle is regulatory. Beau says MiCA was a major step forward, but now only partially addresses the risks that would emerge if non-European stablecoins became widely used, especially in payments. His answer is not to reject tokenization, but to make sure Europe builds it on public money, regulated European private money, and stricter rules for stablecoins that could otherwise pull the region toward dollar-based settlement.

Paris is warning against a dollarized tokenized payment system

Beau’s core concern is strategic as much as financial. He says the efficiency gains promised by tokenized finance could come with monetary stability, financial stability and strategic autonomy risks if stablecoins became major settlement assets in Europe and led to “stablecoinisation” and “dollarisation” of a significant part of the payment system.

That matters because the speech does not treat stablecoins as a niche crypto issue. It treats them as a payments sovereignty issue for Europe. In Beau’s framing, the question is not only whether stablecoins are useful, but who issues them, what currency they are tied to, and whether Europe ends up relying on non-EU digital money for core transactions. This is an analytical conclusion based on the speech’s emphasis on autonomy and settlement structure.

The Banque de France wants Europe to build around public money and regulated private money

Beau says tokenization should develop on the foundation of Europe’s current two-tier monetary system, meaning the coexistence of public money issued by the central bank and private money issued by regulated European financial intermediaries, both exchangeable at par. He says Europe therefore needs secure, efficient and pan-European public and private payment solutions for both wholesale and retail use.

He also says the response should mobilize both public and private actors toward three connected goals: adapting Eurosystem central bank money services for digitalized payments and tokenized finance, supporting tokenized private money issued by European financial institutions, and designing the right regulatory framework while supervising its implementation.

That policy mix is important because it shows France is not arguing for a public-only model. It is backing a hybrid European stack: tokenized central bank money, tokenized deposits, euro stablecoins and the digital euro, all under a tighter rulebook. This is an inference grounded in the structure Beau lays out in the speech.

France says MiCA now needs a second, tougher phase

The sharpest part of the speech comes in the regulatory section. Beau says MiCA is the world’s first comprehensive framework for crypto-assets and that its first year of implementation is a vital step forward, bringing legal certainty for issuance and related services. But he also says MiCA only partially addresses the risks from sector changes, especially if non-European stablecoins become widely adopted.

His proposed fix is clear. He says France is pushing for a strengthening of MiCA, particularly to restrict the use of stablecoins for everyday payments, especially when those stablecoins are backed by a currency other than the euro. He also says MiCA should impose much stricter rules on the multi-issuance of the same stablecoin within and outside the EU to reduce arbitrage risks in periods of stress.

That is a meaningful policy signal for crypto. France is not just asking for better supervision of existing stablecoins. It is signaling that non-euro stablecoins could face tighter limits in everyday European payments if policymakers conclude they pose monetary or regulatory risks at scale. This is an analytical conclusion based on Beau’s call to restrict payment use.

Euro stablecoins and tokenized deposits are part of the answer, not the problem

Beau also used the speech to back projects that would give Europe its own digital alternatives. He pointed to support for initiatives led by European financial intermediaries, including EPI-related work and efforts to develop euro tokenized deposits and euro stablecoins, particularly for cross-border transactions and cash management needs of international companies.

He adds that Banque de France, together with the French Treasury and AMF, has created a strategic group focused on innovation, DLT and tokenization in the French financial center. That shows France is trying to shape the ecosystem through both regulation and market development, not through restriction alone.

The central bank wants its own tokenized money live this year

One of the most concrete lines in the speech concerns infrastructure timing. Beau says the Banque de France is already well advanced on three projects — Pontes, Appia and the digital euro — and says wholesale services in tokenized central bank money will be deployed by the end of this year. He also says the digital euro is a critical part of the response on the retail side, though not the only one.

That timeline matters because it turns the speech from a regulatory critique into a market-structure plan. France is not only arguing that Europe should defend itself against dollar stablecoins. It is saying the public side of the European tokenized money stack should begin arriving soon.

Beau draws a clear line between bank-linked issuers and non-banks

The final section of the speech is also telling. Beau says stablecoins issued directly by a bank, or by an electronic money institution belonging to a banking group, present structurally lower counterparty risk than those issued by non-bank actors. He says banks benefit from direct access to central bank liquidity and European supervision, which strengthens resilience during financial stress.

He also notes that non-bank stablecoin issuers currently do not meet the eligibility criteria for access to central bank accounts under Eurosystem policy. Still, he leaves the door slightly open, saying such access could potentially be considered in the future for non-bank stablecoin issuers that also provide payment services, subject to conditions.

That is important because France is not calling for a blanket ban on non-bank issuers. But it is clearly signaling a preference hierarchy: bank-issued or bank-linked stablecoins first, non-bank models only under tighter conditions and with more caution. This is an analytical inference from Beau’s issuer-risk distinction.

Why it matters for crypto

- France is openly pushing to tighten MiCA, especially around non-euro stablecoins used in everyday payments.

- The speech shows Europe’s stablecoin debate is no longer just about innovation versus regulation, but about monetary sovereignty and payment control.

- Banque de France is backing euro stablecoins and tokenized deposits, but only inside a framework anchored by central bank money and strong European supervision.

- The issuer hierarchy in the speech suggests bank-linked stablecoin models may be politically and regulatorily favored over standalone non-bank issuers in Europe.

What to watch next

- Whether France succeeds in turning its call for tighter MiCA into actual EU-level revisions on payment use and multi-issuance rules.

- Whether euro-denominated stablecoins and tokenized deposits scale fast enough to offer a credible European alternative to dollar-based stablecoins. This is an inference based on Beau’s policy framing.

- Whether tokenized central bank money services really go live by year-end, as Beau said.

- Whether Europe ultimately gives any non-bank stablecoin issuers conditional access to central bank services, a possibility Beau mentions but leaves highly qualified.