Content

Stablecoins did not stop growing in the week of April 22–27, but the pace slowed enough to change the market read.

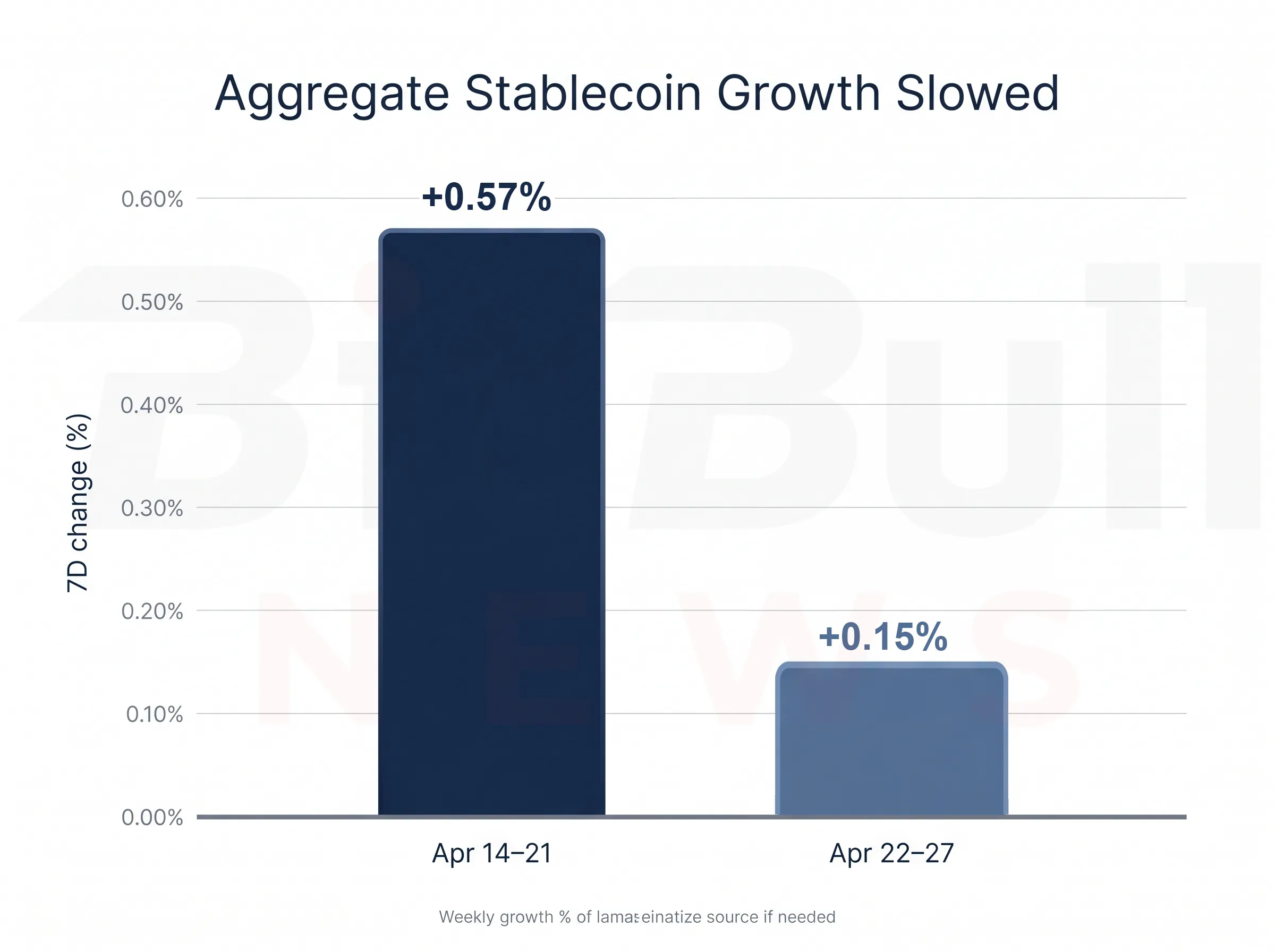

The nearest public end-window snapshot used in the uploaded report put total stablecoin supply near $320.433 billion, up only about $467.35 million over seven days, or roughly +0.15%. In a market this large, that is a small move. It points to a system that is still adding liquidity, but not in a way that suggests a broad new wave of capital rushing in.

The more important signal came from chain behavior. Ethereum’s stablecoin balance slipped slightly while DEX and derivatives activity jumped. Base and BSC both added stablecoin balances and also saw stronger DEX activity. Tron stayed structurally important and still looked like the main USDT settlement rail. Solana stayed active, but without fresh balance growth. Put simply, the market did not look uniformly bullish or uniformly defensive. It looked selective.

How This Extends the Previous Research

This edition should be read as a continuation of BitBullNews Stablecoin Flow Monitor: April 14–21, 2026, not as a separate reset. Last week, the key message was that stablecoin balances were still growing, but deployment was getting pickier by chain and venue. This week, that same pattern sharpened: aggregate growth slowed further, but a few venues still showed active stablecoin-to-risk conversion.

That is the real progression across the two reports. The market has moved from fresh supply growth earlier in April toward more selective use of existing balances. That distinction matters because a flat or slow-growing stablecoin base can still support meaningful trading activity if capital is being redeployed efficiently on the right chains.

Market Structure Snapshot

The stablecoin market remains concentrated enough that the top two issuers still define the macro picture.

The report says USDT held roughly 58.82% of all stablecoins near the window, while USDC sat around $78.2 billion to $78.9 billion depending on the source point used in the report. DAI stayed near $4.61 billion. Native BUSD remained economically tiny, while Binance-Peg BUSD still showed a larger but residual footprint. The “other” bucket — including USDS, USDe, USD1, PYUSD, USDG, and USDD — is now too large to ignore and increasingly matters for DeFi collateral, payments, treasury routing, and synthetic-yield structures.

Table 1. Stablecoin Mix Near the Report Window

| Stablecoin | Approximate size near window | What it signaled |

|---|---|---|

| USDT | Above $184B | Dominant settlement and exchange stablecoin |

| USDC | ~$78.2B to ~$78.9B | Regulated, programmable, payments-oriented dollar |

| DAI | ~$4.61B | Legacy DeFi dollar, still relevant but no longer the core growth engine |

| BUSD | ~$40M native / ~$233M Binance-Peg | Residual rather than macro-relevant |

| Others | Materially active | Growing role in DeFi carry, payments, and specialized liquidity |

The key point for readers is simple: the market still runs on USDT and USDC first, but the long tail is no longer just background noise. It has become part of the real liquidity map.

Weekly Flow by Chain

The cleanest read this week came from the chain-level comparison table in the report.

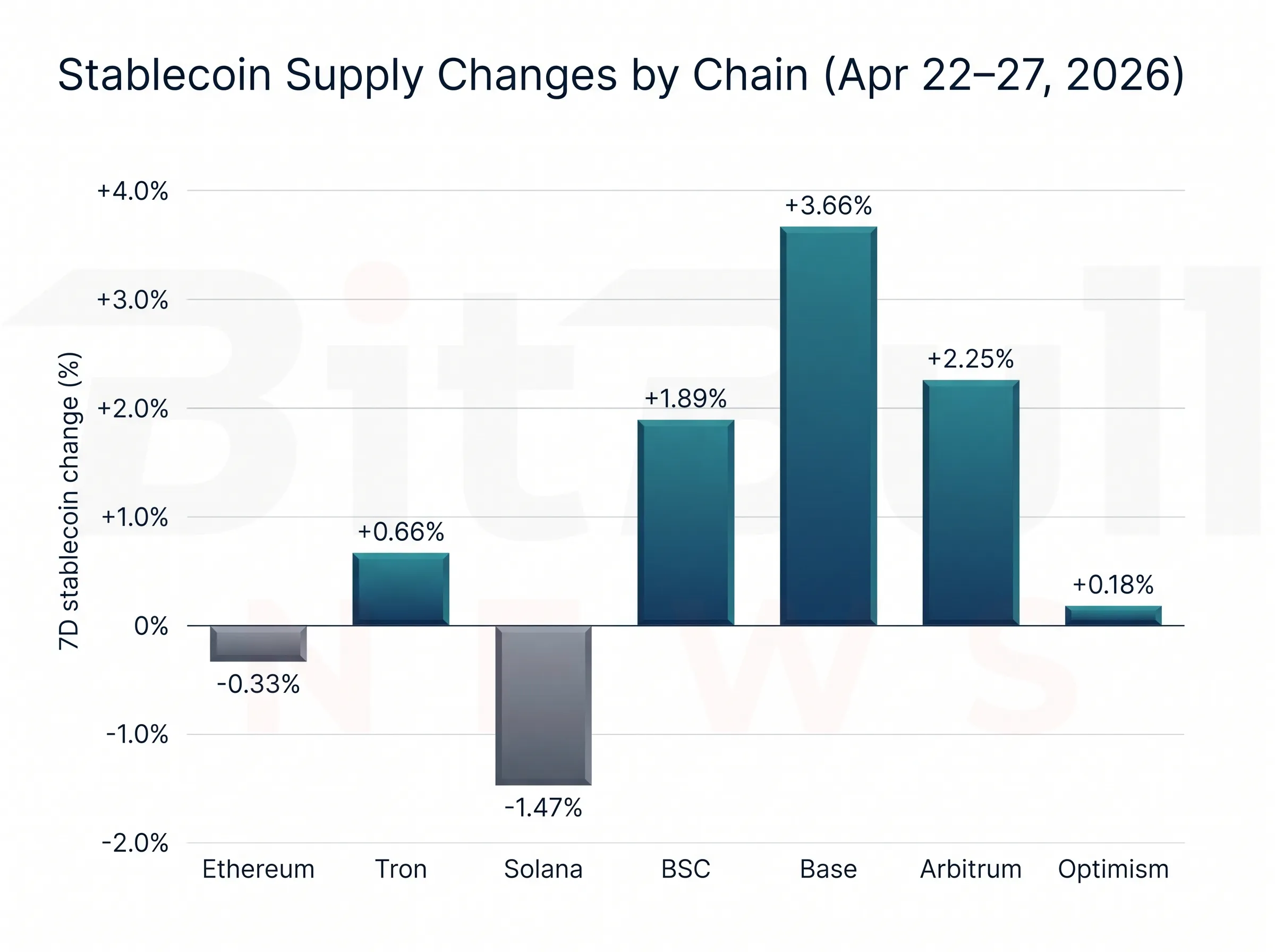

Ethereum stayed roughly flat in absolute stablecoin balances around $166.4 billion, but the reported seven-day change remained -0.33%. BSC rose from about $13.7 billion to $13.9 billion, while Base climbed from about $4.81 billion to $4.98 billion. Arbitrum also stayed positive, rising from around $3.63 billion to $3.93 billion, though more modestly than Base. Tron kept growing slowly, from about $86.0 billion to $87.1 billion. Solana was the standout reversal, moving from a positive prior-week supply read to -1.47% in the latest week. Optimism still grew, but only slightly.

Table 2. Chain-Level Stablecoin Positioning

| Chain | End-week stablecoins mcap | 7D supply change | Read |

|---|---|---|---|

| Ethereum | $166.4B | -0.33% | Existing balances were deployed harder |

| Tron | $87.1B | +0.66% | Settlement and exchange rail stayed strong |

| Solana | $14.66B | -1.47% | High turnover, weaker balance growth |

| BSC | $13.9B | +1.89% | Spot-led, constructive |

| Base | $4.98B | +3.66% | Strongest fresh inflow among major L2s |

| Arbitrum | $3.93B | +2.25% | Positive but smaller-scale than Base |

| Optimism | $580M | +0.18% | Activity up, leverage weaker |

The most useful takeaway is that this was not a week where money simply flowed everywhere. Stablecoin balances rose where the market still wanted optionality and app-layer liquidity, while some venues showed that they were willing to trade harder without needing much new balance-sheet growth.

Chart 1. Aggregate stablecoin growth remained positive, but the pace slowed materially versus the prior issue.

Ethereum: The Clearest Risk-On Deployment Signal

Ethereum was still the most important venue to watch, but for a different reason than a simple “inflows up” story.

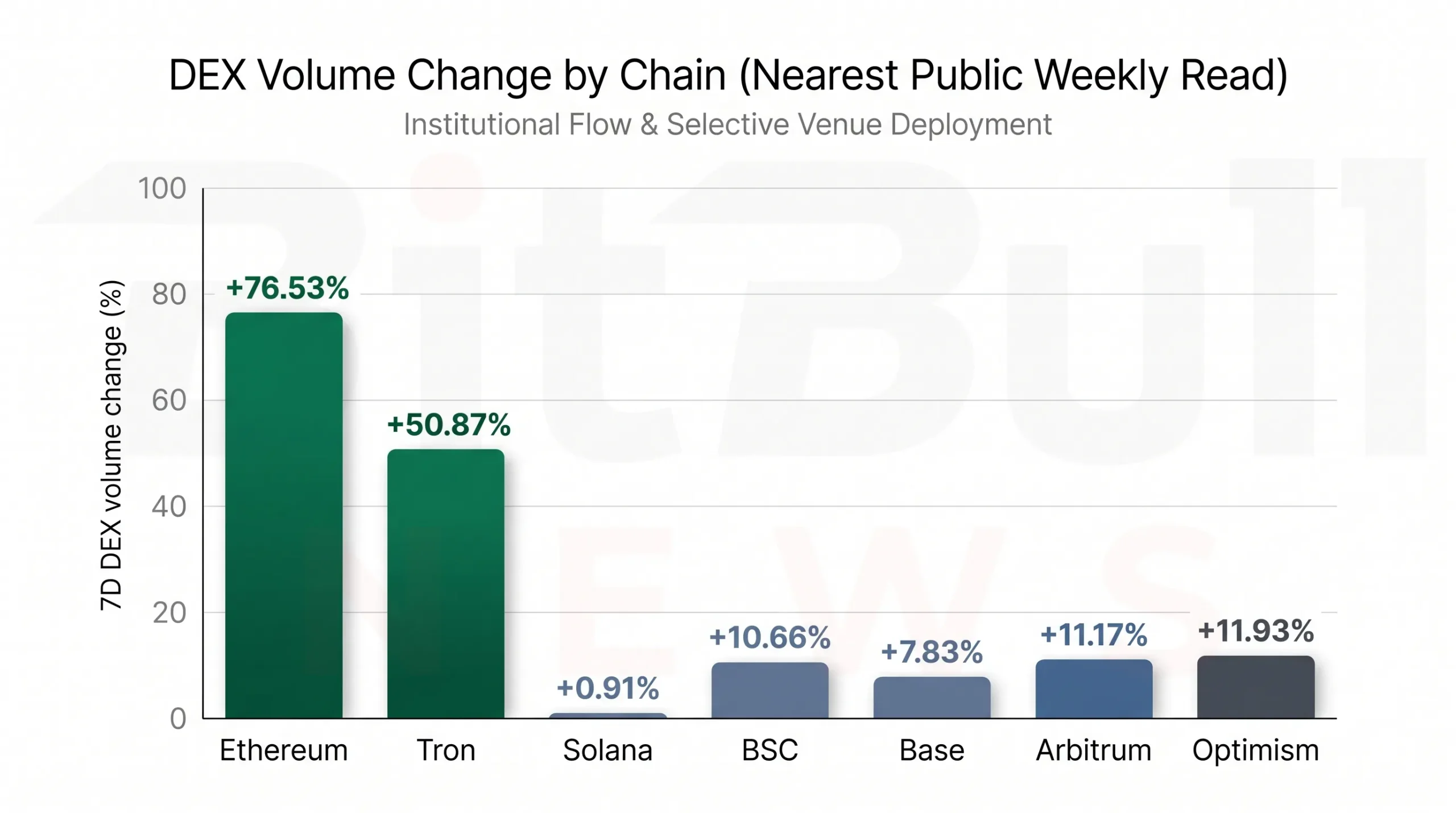

The report shows Ethereum stablecoin balances down 0.33%, while DEX volume surged 76.53% and perps volume rose 7.2%. That is the clearest single signal in the report that existing balances were actively being converted into trading, hedging, and collateral use. In stablecoin research, that pattern often matters more than raw supply growth. It tells you that capital already on-chain is no longer just parked.

That is why Ethereum still led the weekly narrative. It was the best example of deployment from existing liquidity, not just passive stablecoin accumulation. If next week shows stronger balance growth on top of that venue activity, the signal would turn even more constructive.

Base and BSC: Fresh Liquidity Still Found a Home

Base and BSC were the cleanest “fresh balances plus usable activity” chains in the report.

Base posted +3.66% stablecoin growth with DEX volume up 7.83%, although perps fell 18.44%. That combination suggests fresh balances were coming in for spot, apps, and general liquidity, not for leverage-heavy risk. BSC showed +1.89% stablecoin growth and DEX volume up 10.66%, with perps nearly flat. That looks like a healthier spot-led week than a leverage-led one.

For people trying to read stablecoin flows correctly, that distinction matters. A chain can be constructive without being speculative. Base and BSC looked more like growth with real usage than like blow-off risk.

Tron: Still the Main USDT Utility Rail

Tron remained structurally important for the same reason it has mattered all year: USDT settlement scale.

The report shows Tron at about $87.062 billion in stablecoins, up 0.66% on the week, with USDT dominance at 97.84%. DEX volume rose 50.87% and perps volume rose 15.87%, but Tron still should not be read the same way as Ethereum or Base. Its stablecoin behavior remains tied much more closely to settlement, exchange logistics, remittances, and utility-style turnover.

That interpretation lines up with BitBullNews’ recent TRON’s Q4 report: $2.2T stablecoin settlement, 994M transactions, which framed Tron as a stablecoin-first network built around transfer and settlement scale rather than purely DeFi-native liquidity.

Solana and Optimism: Activity Without the Same Balance-Sheet Support

Solana’s closest public read showed $14.66 billion in stablecoins, down 1.47%, while DEX volume was only slightly positive and perps were slightly negative. That is not a collapse. It is a signal that the chain remained active, but without net stablecoin growth reinforcing the move. The system was turning over fast, but not obviously accumulating fresh stable liquidity.

Optimism looked even more mixed. Stablecoins were up only 0.18%, DEX volume rose 11.93%, but perps dropped 53.32%. That is a venue where some activity improved, but leverage clearly did not. In practical terms, it was a milder version of Base’s spot-led profile, with less conviction and much weaker derivatives participation.

Chart 2. Base and BSC showed the strongest positive stablecoin balance growth among the main DeFi-oriented chains, while Ethereum and Solana did not.

Venue Read: Defensive in Aggregate, Risk-On in Pockets

The report’s most useful conclusion is also its simplest one:

Defensive at the supply layer, selectively risk-on at the venue layer.

That summary fits the week well. Aggregate stablecoin growth of +0.15% is too small to describe as a strong fresh-capital impulse. But venue-level activity says capital was still being used aggressively in the right places, especially on Ethereum, and to a lesser degree on Base, BSC, Tron, and Arbitrum.

This is why stablecoin research is more useful when it follows behavior, not just balances. If supply is flat but DEX and perps usage are rising on the right chains, the market is telling you that liquidity is still active — just not everywhere at once.

Infrastructure and Policy Context Still Matter

This week’s issuer-side and infrastructure signals also help explain why stablecoin activity should not be read only as a trading story.

The report notes that Tether’s wallet launch continued to reinforce USDT’s consumer-facing and remittance role, while Circle’s payments and cross-chain infrastructure continued to reinforce USDC’s institutional and programmable-settlement role. That role split remains one of the most important structural truths in the market.

That also makes BitBullNews’ recent Morgan Stanley Launches Stablecoin Reserve Fund For Issuers especially relevant here. The deeper stablecoin story is increasingly about reserve management, operational infrastructure, and regulated financial plumbing — not just exchange balances.

Chart 3. Venue deployment remained strongest on Ethereum and Tron, while Base, BSC, Optimism, and the nearest Arbitrum read also stayed positive.

What This Week Means for the Next One

The market is now at a useful decision point.

If stablecoin growth re-accelerates from here and Ethereum, Base, BSC, and Arbitrum keep showing positive venue activity, the market would have a much stronger case for calling the move a broader risk-on reacceleration. But if supply growth stays soft while only a few venues remain active, then the more likely interpretation will remain reallocation and efficient deployment, not a fresh market-wide liquidity wave.

That is the people-first value of this report. It does not just say whether stablecoins were “up” or “down.” It shows where those balances were likely being used, which is usually the more useful signal for traders, investors, and analysts.

BitBullNews View

From a BitBullNews perspective, the week of April 22–27 was not weak. It was narrower.

Ethereum still showed the strongest conversion of stable balances into risk activity. Base and BSC still looked constructive, but in a more spot-led way. Tron stayed dominant as a USDT utility rail. Solana and Optimism stayed active without showing the same balance-sheet support. And aggregate supply growth slowed enough to remind everyone that the market is still being selective with new capital.

That makes the cleanest conclusion this: the market still had liquidity, but it was choosing its venues more carefully than a broad bullish narrative would suggest.

Key Findings

- Total stablecoin market cap rose only modestly, to about $320.433B, up roughly $467.35M (+0.15%) over seven days.

- Ethereum stablecoin balances were slightly lower, but Ethereum DEX and perps activity rose sharply.

- Base and BSC both added stablecoin balances and also posted stronger DEX activity.

- Tron remained overwhelmingly USDT-led and still functioned primarily as a settlement and transfer rail.

- Solana remained active but without supply growth, while Optimism looked more mixed and much less leverage-led.

- The best overall classification was defensive at the supply layer, selectively risk-on at the venue layer.

Final Verdict

Weekly verdict: Growth softened, deployment sharpened

The week of April 22–27 did not bring a broad stablecoin breakout. It brought something subtler and more useful: a market that was still moving liquidity around intelligently even as fresh aggregate growth slowed.

The clearest conclusion is this:

Stablecoin supply barely moved, but where the market chose to spend stablecoin liquidity still mattered — and Ethereum, Base, BSC, and Tron remained the key venues to watch.