Content

Stablecoin capital did not leave the crypto market in the week of March 2–8, 2026. It rotated inside it. Total stablecoin market size remained in expansion mode, with the main public trackers placing it near the $309–313 billion range by the end of the period. The more important signal, however, was not the aggregate number. It was where fresh digital dollar liquidity chose to sit.

Ethereum extended its lead as the main stablecoin balance-sheet layer. Tron kept adding capital as the market’s dominant USDT corridor. Base delivered one of the strongest relative gains among the major chains. Solana was broadly stable. Arbitrum posted the clearest weekly decline. The weekly picture was therefore constructive for liquidity overall, but selective in where that liquidity was willing to concentrate.

Market Structure Snapshot

The stablecoin market remains overwhelmingly controlled by two issuers. CoinGecko’s stablecoin category showed USDT at about $183.9 billion and USDC at about $77.2 billion, equal to roughly 84.5% of the category combined. After them, the market drops sharply into a second tier that includes USDS, USDe, USD1, DAI, PYUSD, RLUSD and others. In practical terms, this is still a two-issuer market with a growing secondary layer, not a fully diversified one.

That concentration matters because stablecoin growth is not only about more on-chain dollars. It is also about reserve trust, redemption confidence, and distribution power. When most of the market sits in USDT and USDC, issuer quality becomes a market-structure question rather than a side note. BitBullNews already highlighted part of that dynamic in its recent coverage of Circle’s latest results, where USDC circulation growth reinforced the view that stablecoins are maturing into core financial infrastructure rather than remaining a niche trading tool.

Weekly Flow by Chain

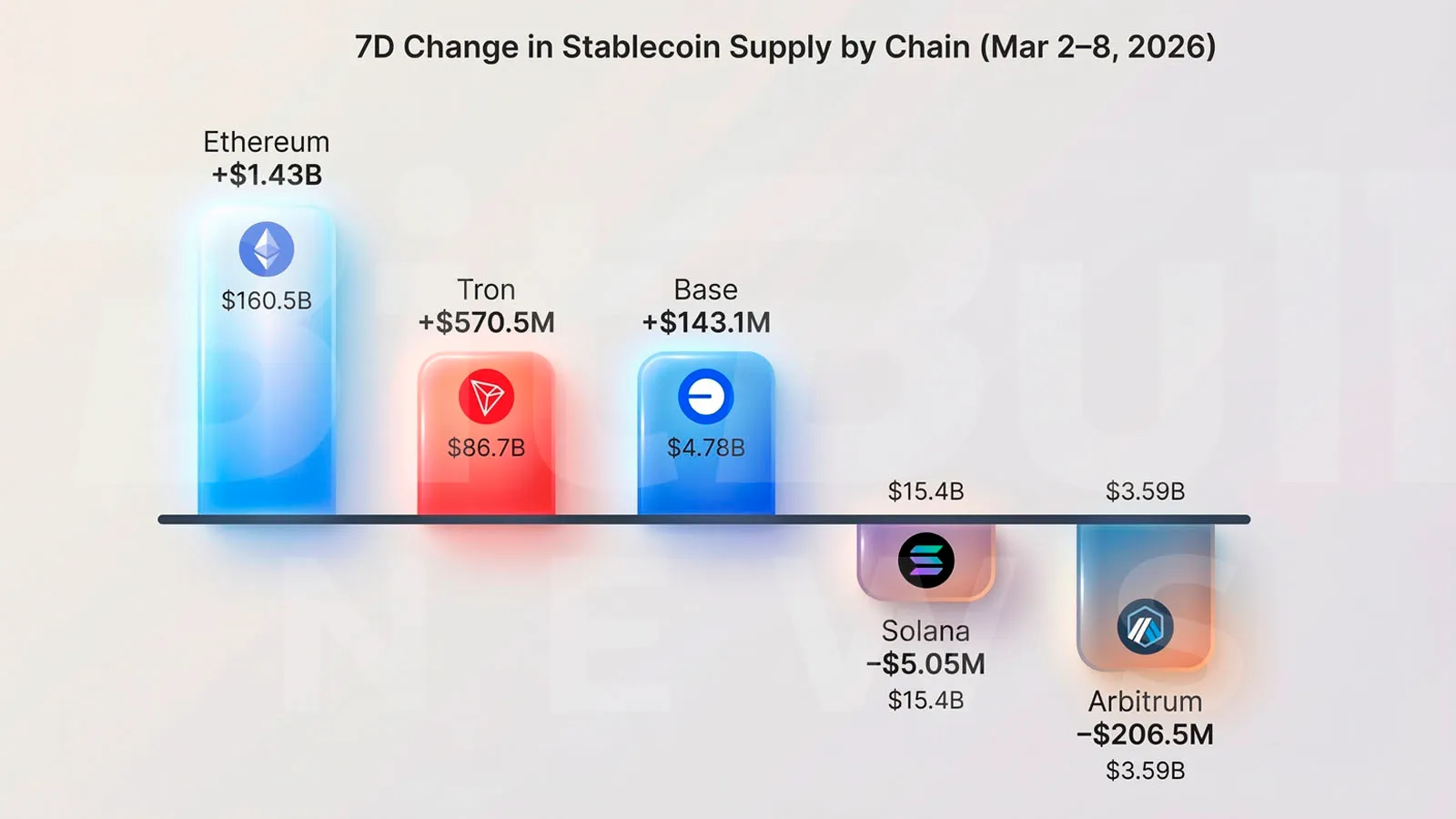

Ethereum remained the dominant stablecoin layer, reaching about $160.5 billion in tracked supply and adding roughly $1.43 billion over seven days. That was the largest absolute weekly increase among the major chains. Tron stayed firmly in second place at about $86.7 billion, with roughly $570.5 million added during the week. Base rose to about $4.78 billion, adding roughly $143.1 million and standing out as one of the strongest relative gainers in the large-chain group.

Solana was close to flat at about $15.4 billion, down only around $5.05 million on the week. Arbitrum moved the other way more clearly, falling to about $3.59 billion after a weekly decline of roughly $206.5 million. That makes this week’s signal fairly clean: stablecoin liquidity did not contract across the system, but it did consolidate more heavily in Ethereum, Tron, and Base while stepping back from Arbitrum.

Chain-by-chain breakdown

- Ethereum: $160.5B, +$1.43B on the week

- Tron: $86.7B, +$570.5M on the week

- Base: $4.78B, +$143.1M on the week

- Solana: $15.4B, -$5.05M on the week

- Arbitrum: $3.59B, -$206.5M on the week

What the Flow Actually Means

Ethereum’s growth confirms that it remains the core place where stablecoins sit at scale. That is consistent with its role as the deepest settlement, collateral, and DeFi layer. Tron’s continued increase points to a different kind of strength: it remains the market’s most important USDT transport rail. DefiLlama shows USDT dominance on Tron at about 98.34%, which underlines that Tron is winning less as a balanced multi-stablecoin ecosystem and more as a highly efficient corridor for Tether liquidity.

Base’s growth is meaningful because it looks increasingly like the clearest USDC expansion zone inside the Ethereum orbit. USDC dominance on Base stood at about 90.34% in the same period. That suggests the chain is attracting fresh digital dollar capacity not through broad issuer competition, but through a very specific pattern of USDC-led on-chain migration. Solana, by contrast, held its position without acceleration. Arbitrum’s decline suggests a real weekly reallocation away from that venue rather than a market-wide exit from stablecoins.

The practical takeaway is simple: stablecoin growth should still be read as available liquidity and settlement capacity, not as automatic proof that capital is already rotating aggressively into higher-risk crypto assets. This week’s data supports a constructive reading for liquidity, but not an indiscriminate risk-on interpretation.

Issuer Quality and Transparency

USDC remains the cleaner transparency case in public disclosures. Circle says it publishes weekly reserve holdings and circulation data, alongside monthly third-party assurance that reserves exceed circulating USDC. That gives USDC a stronger public transparency profile, especially for institutional readers trying to evaluate reserve quality on a recurring basis.

USDT remains the market’s largest stablecoin and its most important pool of dollar liquidity, but the disclosure model is still different. Tether’s own transparency materials emphasize daily circulation visibility and periodic reserve reporting, but the market’s largest issuer still does not present the same disclosure structure that Circle uses for USDC. In a market this concentrated, that difference is not cosmetic. It is systemic.

The second tier also needs to be handled carefully. Fiat-backed, protocol-native, and synthetic dollars may all target the same peg, but they are not interchangeable from a risk perspective. That means future issues of this monitor should continue separating simple supply growth from changes in supply composition.

Structural Risks to Watch

The first structural risk is issuer concentration. A market where two stablecoins dominate is efficient in some ways, but still carries issuer-specific exposure at the system level. The second is chain concentration. Stablecoin liquidity is increasingly clustering around a few preferred rails, which makes distribution strength a strategic advantage but also creates dependency. The third is transparency divergence: public disclosure quality still varies materially between issuers.

The fourth risk is regulatory and policy pressure. BitBullNews has already been covering how stablecoins are being pulled deeper into formal rulemaking, from the UK sandbox process to fresh U.S. debates around issuer rules and global AML treatment. That matters because the next phase of stablecoin growth will be shaped not only by demand, but also by who can keep operating under stricter supervisory expectations.

BitBullNews View

From a BitBullNews perspective, the key question is not whether stablecoins are growing in absolute terms. The key question is where the market is choosing to warehouse digital dollars before they are deployed into trading, DeFi, payments, or treasury activity.

This week’s answer is clear. Liquidity remained constructive, but it did not spread evenly. Ethereum gained the most in absolute terms. Tron kept consolidating its role as the main USDT highway. Base continued to strengthen as a USDC-heavy growth zone. Solana held size without acceleration. Arbitrum was the clearest laggard.

That makes the weekly signal cautiously constructive. The market still has dollar liquidity. It is just becoming more selective about where that liquidity wants to live.

Key Findings

- Total stablecoin market size remained in growth mode during March 2–8.

- USDT and USDC still controlled roughly 84.5% of the stablecoin market.

- Ethereum posted the largest absolute weekly gain in stablecoin supply.

- Tron continued to grow as the market’s dominant USDT corridor, with USDT dominance above 98%.

- Base was one of the strongest relative weekly gainers and remained overwhelmingly USDC-led.

- Solana was broadly flat for the week.

- Arbitrum recorded the clearest weekly decline among the major chains tracked here.

- The broad weekly signal was rotation, not stablecoin exit.

Final Verdict

Weekly verdict: Cautiously constructive

Stablecoin liquidity expanded during the week, but the move was selective rather than broad-based. The market did not signal a clean, all-in risk-on rotation. What it did show is that digital dollar capacity remained inside crypto and continued to concentrate around the chains and issuers with the deepest trust, reach, and utility. For the week of March 2–8, 2026, the most accurate conclusion is this: stablecoins kept growing, but the real story was where they chose to settle.