Content

Institutional crypto adoption did not disappear over the last three months. It changed shape.

From Dec. 10, 2025 to Mar. 10, 2026, the most visible institutional vehicle — U.S. spot crypto ETFs — had a weak quarter on net. Aggregate U.S. spot Bitcoin ETF flows ended the period down about $1.93 billion, while aggregate U.S. spot Ether ETF flows were down about $1.49 billion. January was the main drawdown month, while early March showed a more visible stabilization, especially on the Bitcoin side.

If the quarter is viewed only through ETF flows, the conclusion looks soft. But that would miss the more important development. Corporate treasury accumulation continued. Tokenized fund infrastructure advanced. Broker and bank distribution widened. Institutions kept building market plumbing even while ETF flows were noisy and, on balance, negative.

That makes this quarter less about euphoria and more about infrastructure.

Market Structure Snapshot

The core institutional picture split into two tracks.

The first track was price-access exposure, mainly through ETFs. That layer was volatile, tactical, and net negative over the full quarter. The second track was infrastructure adoption: corporate balance-sheet accumulation, tokenized fund permissions, broker-platform access, custody buildout, and direct crypto product preparation. That layer continued to move forward.

This distinction matters because “institutional adoption” is often discussed as if it were one number. It is not. A fund-flow quarter can look weak while the broader institutional operating stack gets stronger.

This is exactly what happened here. The ETF tape was shaky, but corporate treasuries did not stop. Tokenization did not stop. Distribution did not stop. Banks and brokers did not step back from the category. They kept preparing for larger-scale participation, while USDC circulation growth continued to reinforce the role of stablecoins as institutional financial infrastructure.

BitBullNews has already covered parts of this shift through related stories on stablecoin infrastructure and regulated access, especially where tokenization, custody, and payment rails are starting to overlap with mainstream finance.

ETF and Listed-Product Radar

The ETF story this quarter is best described as drawdown first, stabilization later.

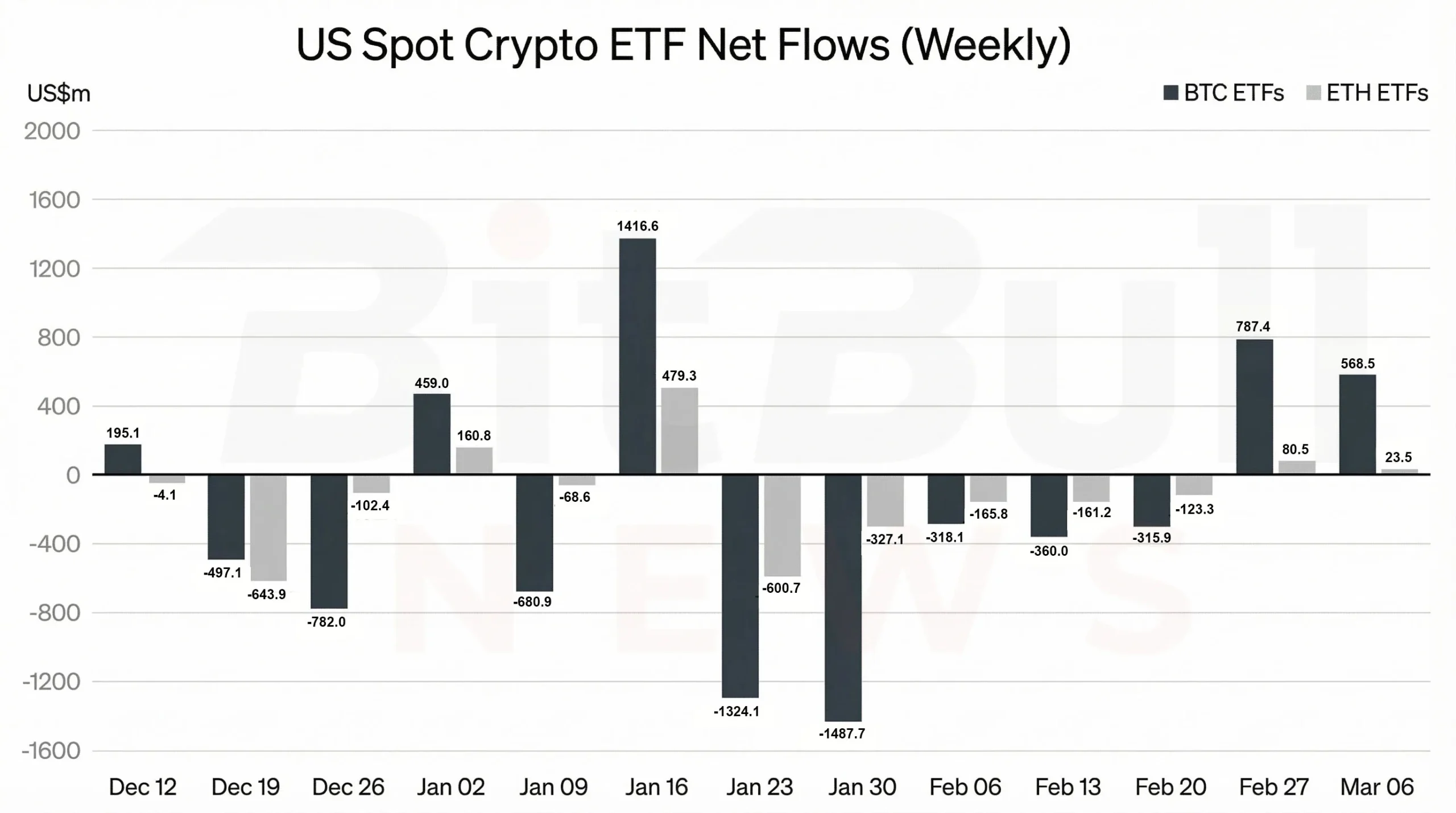

Aggregate U.S. spot Bitcoin ETF flows for the reporting window came in at roughly -$1,925.2 million. December was weak, January was the main washout, February stayed negative, and March 1–10 turned positive at about +$982.5 million. That does not erase the quarter’s net outflow, but it does show that the quarter ended in better shape than it began.

Aggregate U.S. spot Ether ETF flows were softer. They ended the quarter at roughly -$1,491.7 million. December and late January were particularly weak, and while early March improved somewhat, the ETH side never produced the same kind of rebound signal that BTC did by the end of the window.

The weekly pattern matters more than the headline total because it shows how quickly institutional positioning changed during the quarter.

Chart 1. Weekly U.S. spot crypto ETF net flows during the quarter. Bitcoin ETF flows were more volatile but showed a clearer rebound into early March, while Ether ETF flows remained weaker overall.

Two details stand out.

First, this was not a quarter of steady bleeding. It was a quarter of sharp swings. The report identified the largest BTC ETF daily inflow in the window at +$840.6 million on Jan. 14, 2026, and the largest BTC ETF daily outflow at -$817.8 million on Jan. 29, 2026. That is not drift. That is active institutional repositioning.

Second, the latest swing near quarter-end showed that product-level leadership still mattered. On the final trading days covered in the report, flagship products such as BlackRock’s IBIT played a major role in the rebound, even as some competing ETFs continued to post uneven flows. The result was a quarter that looked weak in total but less one-directional than the raw net number suggests.

Snapshot: Which Products Drove the Latest Swing

The underlying report included a useful late-quarter table for selected flagship ETFs. Instead of over-claiming full-quarter issuer totals, it focused on the final trading days from March 3 to March 10, where the stabilization became easier to see.

BTC ETFs (selected) daily flows, US$m

| Date | IBIT | FBTC | GBTC | Total (all BTC ETFs) |

|---|---|---|---|---|

| 03 Mar 2026 | 322.4 | -89.3 | -28.2 | 225.2 |

| 04 Mar 2026 | 306.6 | 48.0 | 21.7 | 461.9 |

| 05 Mar 2026 | -88.7 | -48.0 | -15.0 | -227.9 |

| 06 Mar 2026 | -189.7 | -51.6 | -9.5 | -348.9 |

| 09 Mar 2026 | 47.0 | 28.2 | 57.2 | 167.1 |

| 10 Mar 2026 | 236.2 | -2.4 | -11.9 | 246.9 |

ETH ETFs (selected) daily flows, US$m

| Date | ETHA | FETH | ETHE | Total (all ETH ETFs) |

|---|---|---|---|---|

| 03 Mar 2026 | 41.9 | -66.7 | -4.7 | -10.8 |

| 04 Mar 2026 | 39.3 | 30.3 | 21.9 | 169.4 |

| 05 Mar 2026 | 30.3 | -115.0 | -3.4 | -90.9 |

| 06 Mar 2026 | -4.8 | -67.6 | -1.6 | -82.9 |

| 09 Mar 2026 | -55.1 | 16.2 | -13.4 | -51.3 |

| 10 Mar 2026 | 0.0 | 10.7 | 0.0 | 12.6 |

Balance-Sheet and Treasury Adoption Radar

The strongest counterpoint to ETF weakness was corporate treasury activity.

Several public companies either expanded crypto holdings or disclosed meaningful crypto balances during the quarter. The important thing is not just that they held crypto. It is that many of these positions were disclosed through filings, with enough specificity to move the conversation from narrative to evidence.

Filing-confirmed treasury activity this quarter

| Public company | Asset | What changed in the quarter | Why it matters |

|---|---|---|---|

| Strategy | BTC | Continued disclosing recurring Bitcoin purchases through Form 8-K updates | Shows that the largest corporate BTC strategy remained active despite ETF turbulence |

| DDC Enterprise Limited | BTC | Reported holdings rising from 1,183 BTC at Dec. 31, 2025 to 2,118 BTC at Feb. 28, then disclosed an additional purchase to 2,183 BTC | Demonstrates treasury adoption outside the most obvious names |

| Canaan Inc. | BTC + ETH | Reported 1,793 BTC and 3,952 ETH on balance sheet, alongside mined BTC | Shows mining-linked balance-sheet accumulation remains relevant |

| Sharplink, Inc. | ETH | Disclosed large ETH holdings, liquid staking exposure, and cumulative staking rewards | Suggests ETH treasury strategies are increasingly yield-bearing, not purely passive |

| ProCap Financial, Inc. | BTC | Disclosed 3,000 BTC plus cash held as collateral, with Anchorage and BitGo named in custody structure | Highlights how treasury strategy increasingly overlaps with financing and collateral architecture |

The quarter’s treasury story is important because it weakens the lazy assumption that institutional demand can be measured only by ETF inflows. This quarter suggests the opposite. Institutions can pause or reduce ETF exposure while still expanding treasury, custody, and balance-sheet activity elsewhere.

How Institutions Actually Operationalize a Treasury Entry

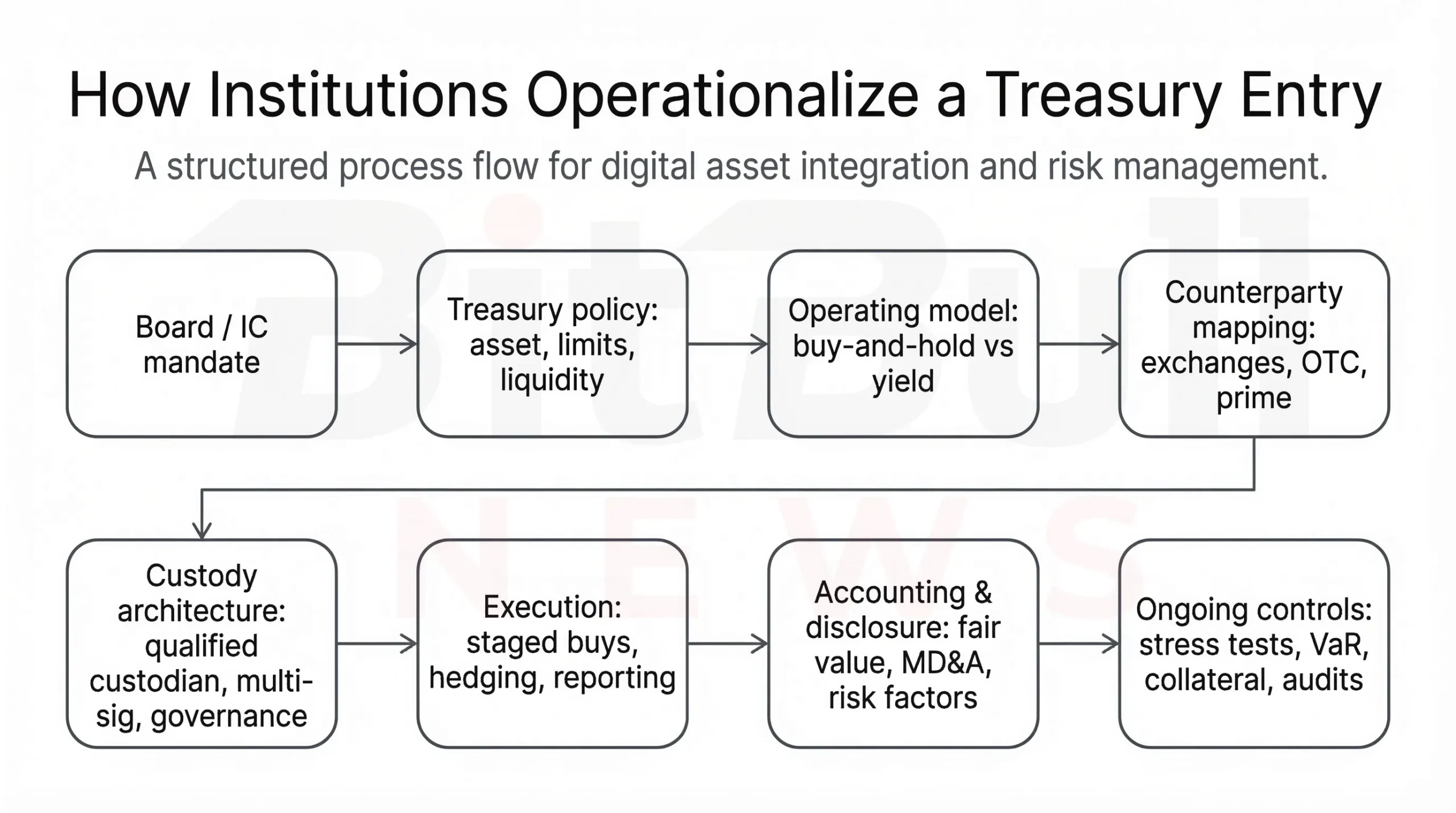

One of the most useful graphics in the report was not a market chart. It was the treasury-entry process map.

That matters because institutional adoption is rarely a single purchase decision. It is an operating model decision. Before a public company adds BTC or ETH to the balance sheet, it has to solve governance, custody, execution, disclosure, and ongoing controls.

Chart 2. Institutional treasury entry is increasingly a full operating framework, not a one-off asset purchase.

The process typically runs like this:

- Board or investment committee mandate

- Treasury policy design covering asset selection, position limits, and liquidity needs

- Operating model choice, including whether the company wants passive exposure or yield-bearing deployment such as staking

- Counterparty mapping, including exchanges, OTC desks, and prime brokers

- Custody architecture, usually involving qualified custodians, governance, and internal controls

- Execution and reporting, often staged rather than one-shot

- Accounting and disclosure, including fair-value treatment, MD&A language, and risk-factor disclosure

- Ongoing controls, such as stress testing, collateral frameworks, and audit readiness

This is why the quarter’s filings matter so much. They show not just asset purchases, but evidence of companies building the operating stack required to hold crypto in a serious way.

Tokenization, Funds, and Market Structure

The most structurally important institutional development of the quarter may not have been ETFs at all. It may have been the steady movement of tokenized funds from concept to regulated operating reality, alongside broader expansion in stablecoin-based global payments infrastructure.

The standout example was WisdomTree, which announced SEC exemptive relief allowing 24/7 trading and instant settlement for tokenized money market fund shares, including settlement against USDC. That is a major signal because it suggests on-chain mechanics are starting to fit inside a regulated fund framework rather than remaining outside it.

That matters for two reasons.

First, it turns tokenization from a “future concept” into a permissions question. Once a regulated asset manager gets formal relief to operate tokenized fund shares with faster settlement, the market starts looking for replication.

Second, it pushes tokenization into an institutional cash-management use case rather than leaving it as a crypto-native experiment. That is a very different adoption profile.

The report also pointed to ongoing movement by major financial players toward tokenized fund infrastructure more broadly. The implication is that institutional adoption is increasingly splitting into two categories: beta exposure through ETFs, and infrastructure adoption through tokenized rails, settlement, and fund mechanics.

This is also where BitBullNews’ stablecoin and tokenization coverage becomes directly relevant. The stablecoin side of institutional adoption increasingly overlaps with tokenized settlement, not just exchange liquidity.

Banks, Brokers, and Distribution

Institutional adoption also broadened through access and distribution.

Vanguard’s reported policy reversal allowing clients to buy crypto ETFs and crypto-linked mutual funds on its platform matters because it expands reach without requiring Vanguard itself to become a crypto issuer. That is a distribution unlock, not just a headline.

The quarter also pointed to a second, more important trend: large brokers and banks are preparing for direct crypto access, not only ETF wrappers, while regulators are also moving toward clearer rules for stablecoin issuers and settlement infrastructure.

Charles Schwab was reported to be preparing a direct crypto offering for launch in Q2 2026. Morgan Stanley was reported to be working toward a proprietary digital wallet initiative later in 2026. Industry reporting also pointed to broader custody, trading, and tokenization efforts among large institutions.

The signal is clear. Traditional finance is no longer treating crypto access as a one-product ETF issue. It is increasingly building a multi-layer stack that includes:

- distribution,

- custody,

- direct trading,

- wallet infrastructure,

- reporting,

- and tokenized settlement compatibility.

That is a much more durable form of institutional adoption than a temporary ETF flow spike.

Real Adoption vs PR

One of the strongest sections of the report was the distinction between real adoption and PR-led intent.

That distinction is essential for BitBullNews because the industry is full of “we plan to” headlines that do not lead to actual balance-sheet exposure, actual product availability, or actual regulatory permissions.

Real adoption vs PR matrix

| Case | Classification | Why |

|---|---|---|

| Strategy BTC purchases | Real adoption | Repeated 8-K disclosures with updated aggregate holdings |

| DDC Bitcoin accumulation | Real adoption | Quantified BTC holdings progression and new purchase disclosure in filed materials |

| Sharplink ETH staking treasury | Real adoption | Quantified ETH holdings, staking deployment, and rewards disclosed in 8-K |

| Canaan BTC + ETH reserves | Real adoption | Specific balance-sheet quantities disclosed in 6-K |

| WisdomTree tokenized MMF shares | Real adoption (regulated) | Regulatory relief plus issuer announcement for 24/7 trading and instant settlement |

| Vanguard platform access to crypto ETFs | Real adoption (distribution) | Policy change that directly expands customer access |

| Charles Schwab direct crypto offering | Execution underway | Timeline disclosed, but quarter lacked operating metrics proving launch |

| Morgan Stanley digital wallet | Execution underway | Signals strategic direction, but not yet shipped-quarter adoption |

This framework helps separate what institutions are already doing from what they are merely signaling.

What the Quarter Actually Means

The most important lesson of the quarter is that ETF flows are no longer a sufficient proxy for institutional adoption.

If ETF flows were the whole story, the quarter would look disappointing. But once treasury accumulation, tokenized fund permissions, direct-access preparation, and broker distribution are included, the quarter looks much stronger.

That does not mean the market saw a clean institutional rush into crypto risk. It did not. What it saw was something more durable: the continued construction of institutional rails.

That is often how real adoption works. Infrastructure appears first. Revenue and balance-sheet behavior follow. Broad sentiment catches up later.

In that sense, the quarter looks more like the early stages of a deeper institutional market structure buildout than a failed adoption cycle.

BitBullNews View

From a BitBullNews perspective, the cleanest way to read this quarter is as a rotation-and-infrastructure quarter.

The visible tape weakened. The underlying buildout continued.

ETF flows were soft, especially through January. But institutions did not step away from crypto. They kept accumulating on corporate balance sheets. They advanced tokenized fund mechanics. They widened brokerage access. They prepared direct offerings and wallet infrastructure.

They kept building the rails through which larger adoption can move later.

That matters more than a single quarter of negative ETF flows.

The institutional question is no longer only “Are they buying the ETFs?” It is increasingly:

- Are they building custody and treasury architecture?

- Are they integrating tokenized settlement?

- Are they making direct access available?

- Are they turning crypto from a product into financial infrastructure?

This quarter’s answer was yes.

Key Findings

- Aggregate U.S. spot Bitcoin ETF flows were about -$1.93B over the quarter.

- Aggregate U.S. spot Ether ETF flows were about -$1.49B over the same period.

- January was the weakest month, while early March showed a visible rebound in BTC ETF flows.

- Corporate treasury accumulation continued despite weak ETF flows.

- Strategy, DDC, Canaan, Sharplink, and ProCap all provided filing-grade evidence of meaningful crypto balance-sheet exposure or growth.

- Sharplink showed that ETH treasury strategies are increasingly tied to staking and yield generation.

- WisdomTree’s tokenized money market fund relief was one of the quarter’s most important infrastructure developments.

- Vanguard broadened platform access, while Schwab and Morgan Stanley signaled deeper direct-access ambitions.

- The strongest institutional signal was not euphoria. It was infrastructure buildout.

Final Verdict

Quarterly verdict: Constructive beneath the surface

This was not a clean “institutions are piling in” quarter if judged only by ETF flows. But it was a meaningful institutional quarter if judged by what serious operators actually built and disclosed.

The most accurate conclusion is this:

institutional crypto adoption kept advancing, but it did so through treasury operations, tokenization permissions, broker access, and infrastructure expansion rather than through a simple flood of ETF inflows.